Which Credit Cards Have Annual Credits?

Whether you’re chasing massive welcome bonuses, maximizing everyday earn rates, or soaking up exclusive perks, the best credit cards usually come with hefty annual fees.

Sure, premium cards can be worth it when the value outweighs the cost, but let’s be honest, who wouldn’t want to save a few bucks?

After all, a free first year is nice, but it’s not forever. Signup incentives are easy to justify for new cards, but what about the ones that stick around in your wallet year after year?

Thankfully, the banks know they need to sweeten the deal to keep fee-paying cardholders loyal. That’s where annual credits come in.

American Express Platinum Cards

The heavyweight champ of Canadian credit cards, the American Express Platinum Card, is a perks powerhouse. It’s got some of the best benefits around, making it a must-have for those who want to travel in style.

You get 2 Membership Rewards points per dollar spent on eligible dining and travel purchases, a complimentary Priority Pass membership with unlimited visits to airport lounges for you and one guest, and automatic hotel status including Marriott Bonvoy Gold Elite and Hilton Honors Gold. Throw in a robust travel insurance, and you’ve got yourself one flash piece of plastic, or should I say, metal.

Let’s be honest: beyond the perks, the Amex Platinum is a bit of a status symbol. It’s the credit card equivalent of pulling up in a luxury car. Whether that matters to you or not, there’s no denying the allure of its exclusivity and sleek branding.

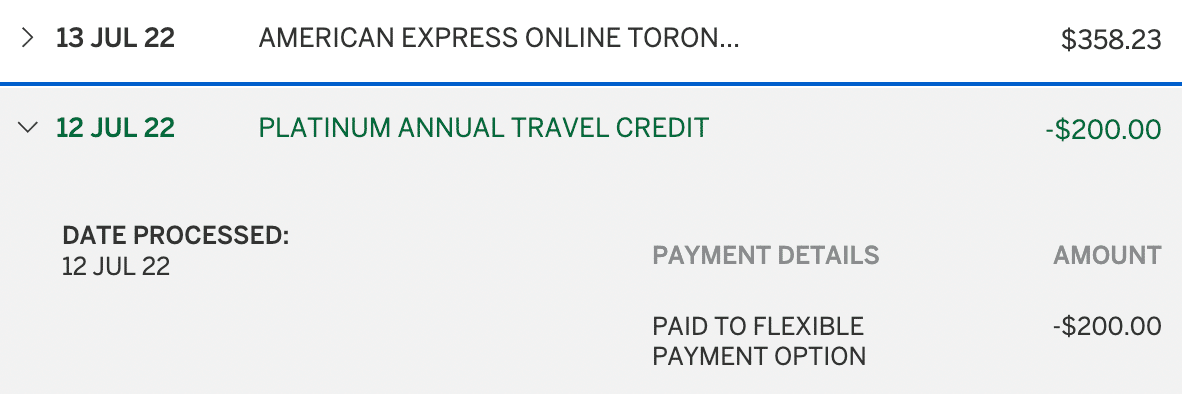

Of course, all that prestige and privilege doesn’t come cheap. The card now commands an eye-popping annual fee of $799 (all figures in CAD). But before you hit the back button, consider this: it comes with a $200 annual travel credit and a $200 annual dining credit, making that fee a little easier to stomach.

Its business variant, the Business Platinum Card from American Express, now also comes with a $200 annual travel credit; however, it didn’t get the $200 annual dining credit added to its list of perks during the most recent revamp.

The travel credit on both cards is extremely flexible and easy to use. You can apply it to any flight, hotel, car rental, or vacation package booked through American Express Travel Online or the Platinum Card Travel Service over the phone. It’s basically a $200 head start on your next adventure.

You have to use the credit when you make the booking; it can’t be applied later. Thanks to its versatility, I’d consider this credit as good as cash.

The $200 annual dining credit on the personal Platinum Card on the other hand, isn’t quite as flexible. It’s limited to a curated list of “top restaurants” handpicked by Amex, most of which are high-end spots.

For a dinner for two, you’ll likely end up spending more than the credit covers. Still, it’s a nice way to justify the Platinum Card’s annual fee, and when you stack it with the travel credit, you’re looking at an effective net cost of $399.

On the Business Platinum, the $200 annual travel credit makes the annual fee $599 instead of $799.

Now, $399 or $599 may still sound steep for a keeper card, but it’s actually on par with or lower than other top-tier cards. The TD Aeroplan® Visa Infinite* Card, the CIBC Aeroplan Visa Infinite Privilege, and the American Express Aeroplan Reserve Card all have $599 annual fees.

If you value the broad travel perks of the Amex Platinum cards over benefits specifically tailored to Air Canada flights, these cards are clear winners. It’s all about choosing what fits your travel style, whether that’s global flexibility or airline-specific advantages.

Read More

First-year value

$1,581

Annual fee: $799

• Earn 80,000 points upon spending $10,000 in the first 3 months

• Plus, earn 30,000 points Upon making a purchase between months 15 and 17 of Cardmembership

Earning rates

Key perks

- $200 annual travel credit

- $200 annual dining credit

- $100 NEXUS credit

- Unlimited Priority Pass lounge access

- Marriott Bonvoy Gold Elite status

- Platinum Concierge

Annual fee: $799

• Earn 80,000 points upon spending $10,000 in the first 3 months

• Plus, earn 30,000 points Upon making a purchase between months 15 and 17 of Cardmembership

Earning rates

Key perks

- $200 annual travel credit

- $200 annual dining credit

- $100 NEXUS credit

- Unlimited Priority Pass lounge access

- Marriott Bonvoy Gold Elite status

- Platinum Concierge

First-year value

$1,914

Annual fee: $799

• Earn 90,000 points upon spending $15,000 in the first 3 months

• Plus, earn 40,000 points upon making a purchase between months 15 and 17

Earning rates

Key perks

- $200 annual travel credit

- $100 NEXUS credit

- Up to $200 annual Dell statement credit

- Up to $300 annual Indeed statement credit

- Up to $120 annual wireless services statement credit

- Unlimited Priority Pass lounge access

Annual fee: $799

• Earn 90,000 points upon spending $15,000 in the first 3 months

• Plus, earn 40,000 points upon making a purchase between months 15 and 17

Earning rates

Key perks

- $200 annual travel credit

- $100 NEXUS credit

- Up to $200 annual Dell statement credit

- Up to $300 annual Indeed statement credit

- Up to $120 annual wireless services statement credit

- Unlimited Priority Pass lounge access

American Express Gold Rewards Card

Think of the American Express Gold Rewards Card as slimmed down version of the Platinum Card.

With an annual fee of $250, the Gold Rewards Card is easier on the wallet compared to the Platinum’s $799 annual fee. Add in a $100 annual travel credit, and you’re effectively looking at a $150 cost, a sweet spot that feels reasonable for most.

The annual travel credit can be used in essentially the same way as the Platinum’s. You have to apply it during the booking process on American Express Travel Online.

When you consider the card’s other perks, including four complimentary visits to Plaza Premium Lounges per year and a $50 NEXUS rebate every four years, there’s a decent amount of value to be found at a lower cost than the Platinum Card.

Pay attention to your spending habits, though. If dining out and grocery runs make up a big chunk of your budget, the American Express Cobalt Card might offer better value with five points per dollar spent on food and drinks, compared to the Gold Rewards Card’s two points.

First-year value

$2,094

Annual fee: $250

• Earn 30,000 points upon spending $4,000 in the first 3 months

• Earn 5,000 points per month upon spending $1,000 per month for 12 months

Earning rates

Key perks

- $100 annual travel credit

- $50 NEXUS credit

- 4 Plaza Premium lounge passes annually

- The Hotel Collection

- Front Of The Line access

- Transfer to airline and hotel partners

Annual fee: $250

• Earn 30,000 points upon spending $4,000 in the first 3 months

• Earn 5,000 points per month upon spending $1,000 per month for 12 months

Earning rates

Key perks

- $100 annual travel credit

- $50 NEXUS credit

- 4 Plaza Premium lounge passes annually

- The Hotel Collection

- Front Of The Line access

- Transfer to airline and hotel partners

Big 5 Banks: Travel & Lifestyle Credits

Let’s take a look at the travel credits, or lack thereof, offered by Canada’s Big 5.

CIBC

In a similar vein to the Amex Platinum Card, the CIBC Aventura® Visa Infinite Privilege* Card also has a $200 annual travel credit, bringing the card’s annual fee down from $499 to a net cost of $299. However, it’s not quite as flexible as the Amex Platinum or Gold credits.

You can only use this credit by booking through the CIBC Rewards Centre. While you can book flights, hotels, car rentals, vacation packages, and cruises, everything is done using CIBC’s agency rates and booking portals.

That means it’s not always easy to attach your loyalty number to a flight or hotel booking. Unless you can find an agent who’s willing to book a different way, you won’t be able to enjoy your hard earned elite benefits, and you can’t enjoy lower members-only rates that you may find.

While this credit isn’t as versatile as Amex’s, it’s still a reliable annual fee reducer.

First-year value

$276

Annual fee: $499

• Earn 25,000 points upon spending $3,000 in the first 4 months

• Earn 25,000 points upon spending $6,000 in the first 4 months

• Earn 30,000 points on card anniversary upon spending $25,000 in the first 12 months

Earning rates

Key perks

- 6 Visa Airport Companion lounge visits per year

- Priority security at Toronto Billy Bishop, Montreal, Ottawa

- Visa RSVP Diamond at 60+ Sandman/Sutton hotels

- Troon Rewards Platinum (20% off at 150+ golf courses)

- $200 annual CIBC by Expedia travel credit

- 2 NEXUS application fee rebates every 4 years

Annual fee: $499

• Earn 25,000 points upon spending $3,000 in the first 4 months

• Earn 25,000 points upon spending $6,000 in the first 4 months

• Earn 30,000 points on card anniversary upon spending $25,000 in the first 12 months

Earning rates

Key perks

- 6 Visa Airport Companion lounge visits per year

- Priority security at Toronto Billy Bishop, Montreal, Ottawa

- Visa RSVP Diamond at 60+ Sandman/Sutton hotels

- Troon Rewards Platinum (20% off at 150+ golf courses)

- $200 annual CIBC by Expedia travel credit

- 2 NEXUS application fee rebates every 4 years

50,000+ travellers get this email

Weekly deals, credit card insights, and points strategies – free forever.

BMO

BMO takes a slightly different approach with its BMO eclipse Visa Infinite* and BMO eclipse Visa Infinite Privilege* cards. Instead of a travel credit, they offer a “lifestyle credit”, which can be redeemed against literally any purchase.

- The BMO eclipse Visa Infinite* comes with a $50 lifestyle credit, lowering the net annual fee from $120 to $70.

- The BMO eclipse Visa Infinite Privilege* comes with a $200 lifestyle credit, lowering the net annual fee from $599 to $399.

While the flexibility of the lifestyle credit is appealing, the bigger question is whether these cards are worth keeping long-term.

Let’s break it down. The BMO eclipse Visa Infinite Privilege* does offer a few travel perks, such as six complimentary lounge visits per year through DragonPass.

The eclipse Visa Infinite*, meanwhile, is light on travel perks. Its current welcome offer does sweeten the deal with up to $20 per month in streaming credits (covering eligible services such as Netflix, Disney+, Crave, and Spotify, with a $500 minimum in monthly card spend), for up to $240 over the first 12 months. That perk is part of the welcome offer, though, so it remains to be seen whether it’ll carry on as an ongoing benefit beyond the first year.

As for the eclipse Visa Infinite Privilege*, the value is a little harder to place. At a net cost of $399, you’re largely paying for six lounge visits and the flexibility of the lifestyle credit, so it’s worth weighing carefully against the alternatives.

Compare that to the Scotiabank Passport® Visa Infinite*, which costs just $150, also includes six lounge passes, and throws in no foreign transaction fees, which can save you hundreds when travelling abroad.

First-year value

$606

Annual fee: $599

• Earn 80,000 points upon spending $6,000 in the first 3 months

• Earn 40,000 points upon spending $30,000 in the first 6 months

• Earn 80,000 points upon spending $75,000 in the first 12 months

Earning rates

Key perks

- 6 Visa Airport Companion lounge visits per year

- Priority security at Toronto Billy Bishop, Montreal, Ottawa

- Visa RSVP Diamond at 60+ Sandman/Sutton hotels

- Troon Rewards Platinum (20% off at 150+ golf courses)

- $200 annual lifestyle credit

- $200 NEXUS application fee rebate (first year)

Annual fee: $599

• Earn 80,000 points upon spending $6,000 in the first 3 months

• Earn 40,000 points upon spending $30,000 in the first 6 months

• Earn 80,000 points upon spending $75,000 in the first 12 months

Earning rates

Key perks

- 6 Visa Airport Companion lounge visits per year

- Priority security at Toronto Billy Bishop, Montreal, Ottawa

- Visa RSVP Diamond at 60+ Sandman/Sutton hotels

- Troon Rewards Platinum (20% off at 150+ golf courses)

- $200 annual lifestyle credit

- $200 NEXUS application fee rebate (first year)

TD

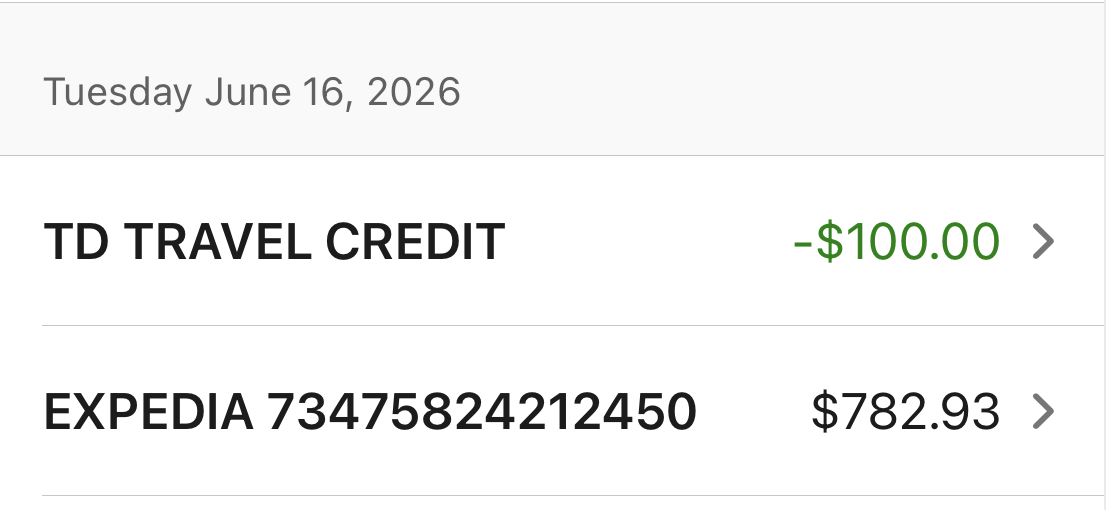

The TD First Class Travel® Visa Infinite* Card had a makeover in the fall of 2022, with changes to its earning structure, design, and annual fee, as well as the introduction of a travel credit of sorts.

It works like this: the $100 TD Travel Credit is tied to accommodation bookings through Expedia for TD. After spending at least $500 on eligible lodging, you’ll receive a $100 statement credit.

While it’s a step forward for TD in the travel credit arena, the restrictions take away some of the shine. Unlike the straightforward, “use it how you want” credits on other cards, this one is a bit more rigid, making it less appealing for those who value flexibility.

However, the card’s annual fee is a modest $139 and is often waived in the first year. As long as you can take advantage of the travel credit each calendar year, your net fee effectively drops to just $39.

At that price point, it’s hard to argue against the value, especially if you’re already booking accommodations through Expedia for TD.

First-year value

$805

Annual fee: $139First Year Rebate

• Earn 20,000 points on first purchase

• Earn 126,000 points upon spending $7,500 in the first 6 months

Earning rates

Key perks

- 4 Visa Airport Companion lounge visits per year

- $100 annual Expedia for TD travel credit

- Annual birthday bonus up to 10,000 TD Rewards points

Annual fee: $139First Year Rebate

• Earn 20,000 points on first purchase

• Earn 126,000 points upon spending $7,500 in the first 6 months

Earning rates

Key perks

- 4 Visa Airport Companion lounge visits per year

- $100 annual Expedia for TD travel credit

- Annual birthday bonus up to 10,000 TD Rewards points

Scotiabank

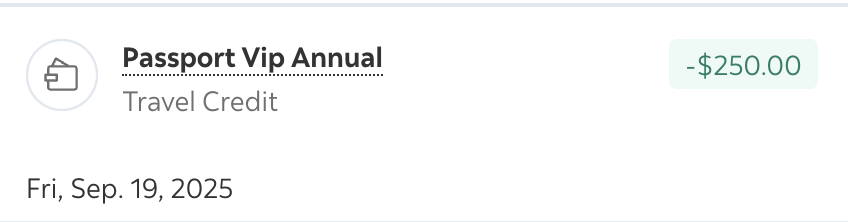

Scotiabank used to be a no-show in the annual credit department, but that’s changed. The Scotiabank Passport® Visa Infinite Privilege* Card now comes with a $250 annual travel credit, bringing its $599 annual fee down to a net cost of $349.

The credit is applied automatically after your first eligible travel purchase of $250 or more, booked through Scene+ Travel, and it renews every year on your account anniversary. As long as you put a single trip through the portal, you’ll claw back $250 annually.

Like the CIBC credit, it’s tied to the bank’s own booking portal rather than being a “use it anywhere” rebate, so it’s a touch less flexible than the Amex credits. Still, on a card that already includes 10 airport lounge visits and strong everyday earn rates, it’s a meaningful offset.

Beyond that one credit, the rest of Scotiabank’s lineup leans on the flexibility of Scene+ points rather than annual credits. I can book travel any way I like and redeem points against the purchase, which means I can book directly with hotels and fully enjoy the elite status I’ve worked so hard to earn.

First-year value

$451

Annual fee: $599

• Earn 30,000 points upon spending $3,000 in the first 3 months

• Earn 30,000 points upon spending $20,000 in the first 6 months

• Plus, earn 20,000 points upon spending in month 13

Earning rates

Key perks

- No foreign transaction fees

- 10 Visa Airport Companion lounge visits per year

- Priority security at Toronto Billy Bishop, Montreal, Ottawa

- Visa RSVP Diamond at 60+ Sandman/Sutton hotels

- Troon Rewards Platinum (20% off at 150+ golf courses)

- $250 annual travel credit via Scene+ Travel

Annual fee: $599

• Earn 30,000 points upon spending $3,000 in the first 3 months

• Earn 30,000 points upon spending $20,000 in the first 6 months

• Plus, earn 20,000 points upon spending in month 13

Earning rates

Key perks

- No foreign transaction fees

- 10 Visa Airport Companion lounge visits per year

- Priority security at Toronto Billy Bishop, Montreal, Ottawa

- Visa RSVP Diamond at 60+ Sandman/Sutton hotels

- Troon Rewards Platinum (20% off at 150+ golf courses)

- $250 annual travel credit via Scene+ Travel

RBC

RBC is the one Big 5 bank that still doesn’t offer an annual credit on any of its credit cards. But here’s the twist: I still consider its cards keepers, thanks to the transferability of RBC Avion points.

If I’m going to use a card regularly, it needs to earn rewards that I find value in. RBC lets me transfer Avion points to British Airways Avios, American Airlines AAdvantage, and Cathay Pacific Asia Miles, opening up opportunities to fly in business or even first class.

For me, that flexibility matters more than chasing partial rebates on products that don’t offer long-term value. Rewards that fit my travel style will always take priority over perks that feel like half-hearted attempts at value.

First-year value

$826

Annual fee: $399

• Earn 35,000 points on approval

• Earn 20,000 points upon spending $5,000 in the first 6 months

• Earn 15,000 points on card anniversary in the first 12 months

Earning rates

Key perks

- 6 Visa Airport Companion lounge visits per year

- Priority security at Toronto Billy Bishop, Montreal, Ottawa

- Visa RSVP Diamond at 60+ Sandman/Sutton hotels

- Troon Rewards Platinum (20% off at 150+ golf courses)

- Transfer to British Airways Avios, Cathay Asia Miles, WestJet, American Airlines

- DoorDash DashPass for 12 months

Annual fee: $399

• Earn 35,000 points on approval

• Earn 20,000 points upon spending $5,000 in the first 6 months

• Earn 15,000 points on card anniversary in the first 12 months

Earning rates

Key perks

- 6 Visa Airport Companion lounge visits per year

- Priority security at Toronto Billy Bishop, Montreal, Ottawa

- Visa RSVP Diamond at 60+ Sandman/Sutton hotels

- Troon Rewards Platinum (20% off at 150+ golf courses)

- Transfer to British Airways Avios, Cathay Asia Miles, WestJet, American Airlines

- DoorDash DashPass for 12 months

National Bank: Travel Enhancement Credits

Apart from the Big 5, National Bank World Elite® Mastercard® also offers an annual credit, but it’s a bit of a puzzle to make sense of them.

Rather than a blanket travel credit that can be used for any booking, it offers a travel “enhancement” credit. They can’t be used for flights and hotels in the traditional sense. Instead, they’re intended to be used to upgrade your travel experience.

Unfortunately, many of these upgrades are already covered by flying business class or having elite status, so let’s see if we can get value for them anyway.

You get a travel enhancement credit worth up to $150 per year, but it’s restricted to very specific types of expenses:

- Airport parking fees

- Baggage fees

- Seat selection fees

- Airport lounge access fees

- Ticket upgrade fees

Against an annual fee of $150, if you’re able to use all of the credits, you can essentially keep the card year-over-year without an annual fee. For a card that’s already worth keeping for award ticket insurance and emergency medical assistance on trips up to 60 days, eliminating the annual fee makes it a no-brainer.

However, National’s redemption process is fairly involved. You need to submit an itemized invoice to the rewards department, showing a travel upgrade that was used (not purchased) on a past date.

At a certain point, it comes down to how much effort you’re willing to put in. If the redemption process feels like too much hassle, or the eligible expenses don’t line up with how you travel, the credit may not be worth pursuing on its own.

That said, as mentioned earlier, the award ticket insurance alone makes this card worth keeping. Sometimes, a single standout feature can tip the scales, saving you both money and peace of mind when things don’t go as planned.

First-year value

$400

Annual fee: $150

• Earn 5,000 points upon spending $5,000 in the first 3 months

• Earn 10,000 points upon spending $20,000 in the first 12 months

• Earn 10,000 points

• Earn 10,000 points

Earning rates

Key perks

- Airport lounge access

Annual fee: $150

• Earn 5,000 points upon spending $5,000 in the first 3 months

• Earn 10,000 points upon spending $20,000 in the first 12 months

• Earn 10,000 points

• Earn 10,000 points

Earning rates

Key perks

- Airport lounge access

Calendar Year vs. Cardmember Year Credits

Not all annual credits run on the same clock, and the difference matters more than you might think. Some credits reset on the calendar year (January 1 to December 31), while others reset on your cardmember year, the 12-month period that begins on your account anniversary.

Why does it matter? A calendar-year credit can effectively be used twice in a short window: once in December, and again in January once the new year’s credit becomes available. A cardmember-year credit doesn’t offer that flexibility, since it resets on the anniversary of when you opened the card.

The American Express Platinum Card is the perfect example, as it carries one of each: its $200 dining credit resets every calendar year, while its $200 travel credit resets every cardmember year.

The annual credits on some of Canada’s most popular keeper cards break down as follows:

| Card | Annual Credit | Calendar Year | Cardmember Year |

|---|---|---|---|

| American Express Platinum Card | $200 dining credit | ✓ | |

| American Express Platinum Card | $200 travel credit | ✓ | |

| Business Platinum Card from American Express | $200 travel credit | ✓ | |

| American Express Gold Rewards Card | $100 travel credit | ✓ | |

| CIBC Aventura Visa Infinite Privilege | $200 travel credit | ✓ | |

| BMO eclipse Visa Infinite Privilege | $200 lifestyle credit | ✓ | |

| BMO eclipse Visa Infinite | $50 lifestyle credit | ✓ | |

| TD First Class Travel Visa Infinite | $100 travel credit | ✓ | |

| National Bank World Elite Mastercard | $150 travel credit | ✓ | |

| Scotiabank Passport Visa Infinite Privilege | $250 travel credit | ✓ |

If you’re applying for a card largely for its annual credit, a calendar-year credit is the more valuable of the two: apply late in the year, and you may be able to claim the credit twice within a few weeks before your first renewal even comes due.

US Credit Cards

This is where it gets fun. Annual credits are much, much more abundant on US cards than they are in Canada, with many cards providing more credits to cardholders than the cost of the annual fees.

Below is a small sample of cards whose annual net costs are lower than they appear (all numbers in US dollars, with some credits distributed in chunks throughout the year):

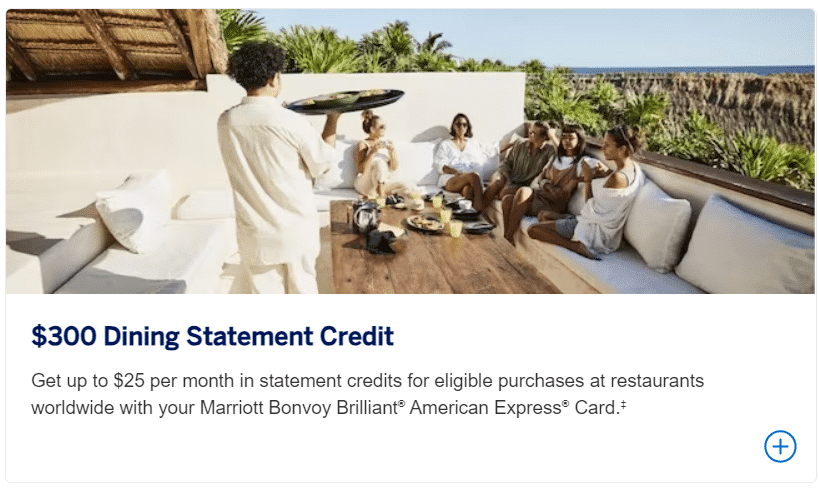

- American Express US Marriott Bonvoy Brilliant Card: $650 annual fee, offset by 12 × $25 monthly dining credits, $100 property credit at The Ritz-Carlton or St. Regis with two night minimum stay, and an anniversary Free Night Award worth up to 85,000 Bonvoy points (worth $595 as per our Points Valuations)

- American Express US Business Platinum Card: $895 annual fee, offset by up to $600 in annual hotel credits (2 × $300 semi-annual on prepaid Fine Hotels + Resorts and The Hotel Collection bookings), a $200 annual airline credit, up to $200 in annual Hilton Honors credits, and Dell credits (up to $150, plus up to $1,000 more after $5,000 in annual Dell spending)

- American Express US Hilton Honors Aspire Card: $550 annual fee, offset by up to $400 in annual Hilton resort credits (2 × $200 semi-annual), up to $200 in annual flight credits (4 × $50 quarterly), an annual Free Night Reward, and a CLEAR Plus credit (around $189)

- American Express US Hilton Honors Surpass Card: $150 annual fee, offset by 4 × $50 quarterly Hilton property credits

- American Express US Platinum Card: $895 annual fee, offset by up to $600 in annual hotel credits (2 × $300 semi-annual on prepaid Fine Hotels + Resorts and The Hotel Collection), up to $400 in annual Resy dining credits (4 × $100 quarterly), up to $300 in annual digital entertainment credits ($25 monthly), a $200 airline fee credit, and up to $200 in annual Uber Cash

- American Express US Gold Card: $325 annual fee, offset by a $120 annual dining credit ($10 monthly), $120 in annual Uber Cash ($10 monthly), a $100 annual Resy credit, and an $84 annual Dunkin’ credit ($7 monthly)

- Capital One Venture X Rewards: $395, offset by up to $300 in in statement credits for flights, hotels, or rental cars booked through the Capital One Travel portal

- Citi Strata Premier Card (formerly the Citi Premier Card): $95 annual fee, offset by a $100 annual hotel credit on a single Citi Travel hotel stay of $500 or more

- Chase Sapphire Reserve: $795 annual fee, offset by a $300 annual travel credit, up to $500 in annual hotel credits through The Edit (2 × $250 semi-annual), up to $300 in annual dining credits, and up to $300 in annual StubHub/viagogo credits

Of course, many of these rebates are only valuable if they suit your lifestyle. There’s no point having the Hilton Aspire card if you don’t have cash expenses at their resorts and with eligible US airlines. But for those who’d benefit, it’s wild to see cards at the most premium tier practically paying you to be a cardholder.

Also, aside from hotels, many of the credits are difficult to use outside of the US. While the Amex US Gold Card offers an excellent 4x earning rate on restaurants around the world, you’d likely have to live in or frequently travel to the US to properly offset the annual fee with cash credits.

Additionally, the airline credits are only for incidental fees.

Keeper cards are a much bigger part of the Miles & Points strategy for Americans. In the US, repeat welcome bonuses are harder to come by, and it’s more important to maintain good relationships with credit card issuers by putting regular spend on your cards.

I think it’s worthwhile for Canadians to take note, as keeper cards and relationship-building are taking on a higher importance here as well. Hopefully we’ll see our banks follow suit and offer more credits as they try not only to gain our business, but also to retain it in a competitive marketplace.

American Express Offers

Beyond annual credits, Amex Offers give cardholders (including Scotiabank Amex cardholders) the chance to snag extra rewards points or cash rebates. These ongoing perks make a strong case for keeping Amex cards in your wallet year after year.

I don’t like to bank on guarantees, but some offers are like clockwork. Take the Marriott Offer, for example: it reliably pops up at least once a year and typically delivers a solid $50 to $60 rebate per card.

Other offers are less predictable, but usually quite valuable.

More and more, we’re seeing that some banks are less likely to give repeat welcome bonuses, and that they’re more likely to approve you for new cards if you keep your cards long term.

If you can anticipate enough useful offers to offset your annual fee, it might be worth hanging onto a premium card beyond the first year to create a win-win situation for you and the issuer.

Conclusion

The more credit cards I add to my collection, the more I appreciate the value of keeping certain cards long-term. When it’s time to renew and face another annual fee, I always ask myself: Am I getting enough value to make it worth it?

Often, the earn rates and perks justify the cost, but it’s not always an easy comparison against other cards. That’s where annual credits come in. They provide peace of mind and cost certainty, acting as a reliable offset to those fees.

While there are countless other ways to offset costs, like hotel vouchers, companion fares, referral bonuses, bank account rebates, or even just negotiating with the issuer, they can be inconsistent and laborious.

For me, annual credits stand out because of their simplicity and predictability. I know I can count on their value, which makes them a cornerstone of my long-term credit card strategy.

Member Discussion