Low-Hanging Fruit: Easy Credit Card Bonuses for Everyone

Note: AIR MILES rebranded to BMO Blue Rewards in summer 2026. Existing balances were converted at 95 Air Miles = 1,500 Blue Rewards points. Read the announcement.

A little while back, I wrote about three different ways I measure my Miles & Points earnings. Some credit card bonuses are easier to earn than others, and no matter what my current credit card strategy looks like, I’m always looking for ways to be efficient with my efforts.

Today, I want to take a closer look at how you can use certain credit card offers that are highly efficient, some infinitely so, to earn rewards easily by eliminating (or at least greatly reducing) fees or spending requirements.

I’ll cover my outlook on different ways to play the game. I’ll also provide some specific suggestions for those of you who may be more hesitant to get started, and I hope that my outlook shows you that your fears may be overblown.

Rewards Credit Cards: Top-Down or Bottom-Up?

Ricky talks a big game when it comes to premium credit cards, and rightfully so. It’s often worth it to pay big annual fees, and you’ll earn points fastest if you’re willing to pay to play.

But let’s be realistic: Miles & Points can be an intimidating pursuit, and not every newcomer is ready to dive right in.

All of the points collectors I’ve encountered fall into one of two camps: travel-seekers who appreciate value, and value-seekers who appreciate travel.

If you’re the former, it’s a lot easier to bite the bullet and go straight for premium credit cards. If you have very specific travel goals, the value you’re getting by booking award flights instead of cash flights is impossible to ignore, and it’s worth the effort to bend over backwards and hammer some ultra-high spending requirements.

I’d call that a top-down approach – come out guns blazing, learn about complex flight redemptions at the outset, and aggressively rack up rewards as fast as you can with the biggest welcome bonuses and best perks.

On the other hand, my own origin story falls more into the latter camp.

I began by optimizing category earn rates and intentionally prioritizing the simplicity of cash back over arcane loyalty programs (two strategies which I no longer place at the forefront). I’ve developed my rewards game incrementally, motivated from the value side.

As a lover of travel, I’m confident that I’ll get good value for my efforts whenever I do eventually redeem. However, without a laser-focus on a particular aspirational booking, I’ve been careful not to put in more than I need to (whether it’s more fees or more spend), instead accumulating points slowly but deliberately. Let’s call that the bottom-up approach.

We tend to focus a lot on the top-down strategy around here, but I suspect that there are far more bottom-up points collectors than it seems.

Achieving Infinite Returns

With that being said, there are some concrete ways to get your feet wet with credit card rewards, all while still racking up meaningful balances of points.

Circling back to how I measure the efficiency of my points earnings, it’s easy to see how by maximizing metrics like Return on Fees or Return on Spend, you can still earn points very quickly without having to splurge on the credit cards with the biggest absolute bonuses.

These are what we call low-hanging fruit offers, where the bonus is too easily achievable, and the value is too obvious, to ignore.

These offers are a great first step for beginners who may be intimidated by other ways to play the game. They also continue to play a key role in my advanced strategy even as I’ve gradually grown bolder over time; the value and convenience here is still unmistakable.

Infinite Return on Fees: First Year Free

If you’re unable or unwilling to invest a lot into big annual fees, you’ll definitely want to focus on cards with a first-year annual fee waiver.

In particular, this is a great way to earn points for free before you’ve determined your own personal valuations based on your own redemption patterns. It’s all too easy to get trapped in analysis paralysis trying to figure out if this game is “worth it,” but with lucrative First Year Free offers, there’s literally nothing to lose.

For beginners, I highly recommend leaning heavily on these offers. They don’t take any brainpower or math to understand, and if you get started on earning pronto, you’ll have accumulated a nice balance of points by the time you’ve figured out how you want to redeem them.

I’d avoid cards with no annual fee, and instead prioritize cards with First Year Free offers. Cards with no fee on a recurring basis tend to target the entry-level segment of the market, and provide paltry signup incentives accordingly.

Instead, temporary annual fee waivers can be found on better cards, the sort of card that has a better welcome bonus. Sure, you’re on the hook when the second year comes around, but that’s a problem you can address when the time comes.

Here are the cards I’d watch for First Year Free offers:

- Among the Big 5, TD, CIBC, and BMO rotate their points promotions, but they generally all consistently offer a first-year annual fee waiver on their Visa Infinite, World Elite, and Business cards.

- Similarly, HSBC’s welcome bonus comes and goes, and it’s a bit different every time, but most of its rotating special offers tend to include First Year Free (or with an equivalent points boost in Quebec).

- The MBNA Alaska Airlines Mastercards have started offering a $100 statement credit periodically (including the current offer until June 30, 2021), enough to fully offset the annual fee on either the World Elite or Platinum Plus variant. Failing that, you can get the fee significantly rebated by applying through a cash back portal.

- The Brim World Elite Mastercard has also begun offering a first-year annual fee waiver. The offer has an end date of May 31, 2021, but like BMO it seems they’ve been extending it every time it expires.

Overall, First Year Free offers on mid-tier cards are pretty much the industry standard at this point, with no shortage of ways to earn credit card rewards at no cost to you.

Recommended Credit Cards with No First Year Annual Fee

Welcome bonus: 75,000 Aeroplan points

Annual fee: $180

First-year value

$2,415

Welcome bonus: 40,000 Aeroplan points

Annual fee: $139

First-year value

$588

Welcome bonus: 45,000 Aeroplan points

Annual fee: $139

First-year value

$546

Welcome bonus: 20,000 Aeroplan points

Annual fee: $89

First-year value

$441

Infinite Return on Spend: First Purchase

For every dollar you charge to a credit card, that’s a dollar that you can’t charge to another card. Whether you’re earning everyday rates or chipping away towards a welcome bonus threshold, it’s good to make every dollar count for as much value back as you can.

If you’re unable to spend a lot of money in time to meet the requirements to earn the bonus, you’ll definitely want to focus on cards which award the bonus upon approval, activation, or first purchase.

For limited spenders, you can accelerate your rewards with these offers. There’s no opportunity cost because you don’t actually have to put any of your spending capacity towards earning the bonus. You can instead devote your scarce spending efforts towards other valuable cards that demand it.

Notably, Quebec residents will be quite well-versed with this concept. Due to some peculiar provincial legislation, credit card issuers can’t offer spend-based incentives to new applicants. Instead, many banks run alternate promotions for Quebec, doing away with the spend requirement entirely and just giving you the same number of points for keeping your account open and in good standing for a few months.

They’ll even do this for premium credit cards, like the TD Aeroplan Visa Infinite Privilege:

That’s certainly awesome for Quebecers operating on a low spending capacity. Even for those with higher cashflow, it eliminates the chore of switching up which credit cards you’re using. As long as you’re willing to pay the annual fees, there’s no reason why you can’t apply for as many good offers as possible.

For Canadians elsewhere, we don’t have as many options, short of moving to La Belle Province.

All of RBC’s credit cards award the bonus without any spending requirement, including their recent promotions for 35,000 Avion points across the Avion family. Roughly speaking, these are the highest-value first-purchase cards out there, and you’ll usually have to spend for the bonus for any other card worth applying for.

Instead, if you’re struggling to spend, look for offers with welcome bonuses awarded in multiple parts. Often, you’ll see promotions with some points awarded upon first purchase, and more points awarded upon meeting some other requirement.

If you deem that the first purchase bonus alone is enough to justify the credit inquiry and any annual fee, feel free to skip the spending requirement and forgo that portion of the bonus if you feel your spending will have a bigger impact on a different card.

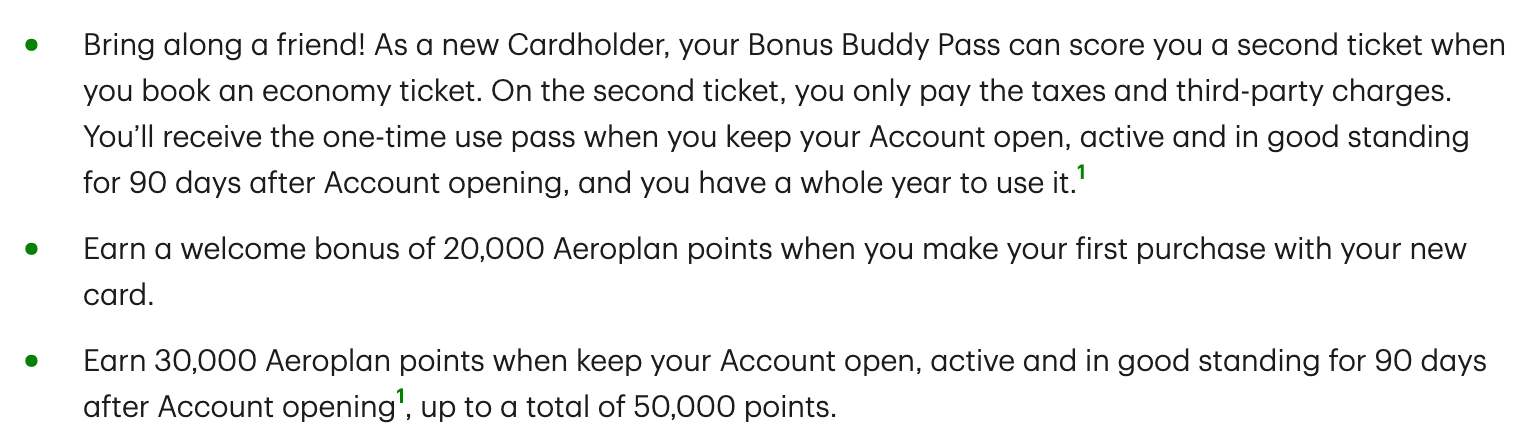

For example, the CIBC Aeroplan Visa Infinite currently offers 10,000 Aeroplan points upon first purchase, plus 10,000 Aeroplan points and a Buddy Pass worth 30,000 points upon spending $1,000 within four months, for a total up to 50,000 Aeroplan points.

If you can’t meet the spending requirement, you could choose to treat the card like a 10,000-point offer with with no strings attached (although you’d definitely be leaving some serious value on the table).

50,000+ travellers get this email

Weekly deals, credit card insights, and points strategies – free forever.

Recommended Credit Cards with No Spending Requirement

Welcome bonus: 70,000 Avion points

Annual fee: $399

First-year value

$826

Welcome bonus: 70,000 WestJet points

Annual fee: $139

First-year value

$536

The Best of Both Worlds

Finally, this one speaks for itself. Once in a while, you’ll come across an offer that dispenses the bonus upon signup without any required spending and without an annual fee for the first year.

The only thing limiting you from applying for as many of these credit cards as possible is the number of credit inquiries you can spare. For these offers, I’d recommend ranking them by Net Gain, and only going for the ones that are worth a hard pull – $300 first-year value or more is commonly accepted as a reasonable benchmark.

Fortunately, from time to time, there are some mid-tier credit card offers that hit this sweet spot, offering bonuses that are worth more than what you’d get from an entry-level card:

- In the past we’ve seen the RBC Avion Visa Infinite and WestJet RBC World Elite Mastercard run a First Year Free promotion on top of their typical first-purchase bonuses.

- The size and format of CIBC’s welcome bonuses have fluctuated over the years, but I recall the CIBC Aeroplan Visa Infinite and CIBC Aventura Visa Infinite cards having this type of bonus at one point.

Otherwise, it’s slim pickings, unless you’re keen on the PC Financial World Elite Mastercard (when it runs a signup promotion) or the MBNA Best Western Rewards Mastercard.

How I Started with Low-Hanging Fruit

I’ll wrap up by sharing my personal strategy when I was starting out with a bottom-up approach.

I began by filtering out the credit cards that didn’t interest me. I looked at my big-picture goals, and decided to focus on programs that offer outsized value rather than fixed value. That meant collecting airline and hotel loyalty programs, both directly and via transferable points, while skipping bank and shopping points programs.

I actually covered quite a broad spectrum with my early rewards cards. I didn’t concentrate excessively on a specific program, like by funnelling Aeroplan relentlessly from every available source. Instead, I focused more on avoiding distractions, such as Air Miles and Scotiabank.

Then, I ruled out any offers if I wouldn’t be able to meet the minimum spend requirement. Amex Platinum cards were off the table, and instead I lined up a steady stream of low spend requirements which I knew I could meet with confidence.

I also made sure to avoid spending money just to earn rewards. To me, that meant minimizing annual fees, transaction fees, and lifestyle creep.

All said and done, here’s a snapshot of the low-hanging fruit cards I opened as I was getting started, and what made them appealing at the time (aside from their value, of course):

- TD Aeroplan Visa Infinite: First Year Free, $1,000 minimum spend

- TD First Class Travel: First Year Free, $1,000 minimum spend

- WestJet RBC World Elite: first purchase

- Amex Gold: First Year Free, $1,500 minimum spend

- MBNA Alaska World Elite: partial cash back rebate, $1,000 minimum spend

- RBC Avion Visa Infinite: First Year Free, first purchase

- CIBC Aeroplan Visa Business: First Year Free

- CIBC Aeroplan Visa Infinite: First Year Free, first purchase

- Amex Bonvoy: partial cash back rebate, $1,500 minimum spend

- TD Aeroplan Visa Business: First Year Free

At a glance, these offers should be totally achievable for any new Miles & Points enthusiast. You could pick and choose among any offers like these, as an alternative to the imposing spectre of the Amex Business Platinum’s $499 annual fee and $10,000 minimum spend.

I amassed over 200,000 Aeroplan points in my first year just from First Year Free offers alone, with only two cards having a spending requirement above $1,500. Although it may not be the fastest route, I absolutely believe that it’s possible to achieve meaningful gains in spite of any limitations you may face with fees or spend.

Conclusion

Credit card offers with a First Year Free promotion or a first purchase bonus are an easy shortcut to racking up rewards when you’d normally be limited by fees or spend. Whether you’re a fresh-faced beginner or a grizzled veteran, whether your timelines for earning and redeeming are long or short, these offers have a place in anyone’s strategy.

Specifically, these offers can be an accessible starting point for beginners who are looking for value, but aren’t prepared to pay big annual fees yet. If you’re struggling with the psychology of pay-to-play tactics, there’s no reason not to get started immediately with a slow and steady approach.

If you want to find some low-hanging fruit for yourself, check out our tools for sorting and filtering credit cards. You can adjust the value, fees, and spend sliders to set the bar as high or low as you want. You can also select rewards programs to rule out distractions, and you can set banks, payment networks, or income if you face any other constraints in those areas.

First-year value

$2,415

Annual fee: $180First Year Rebate

Member Discussion