Koho Extra Account: Prepaid Going Premium?

Canada’s prepaid credit card scene never fails to be interesting.

Whereas this segment of the market was in its infancy a mere five years ago, there’s now an endless roster of competitors: from the PC Financial Money Account, to EQ Bank’s no-FX fee offering, to the once-great Mogo Prepaid Visa, and others, we have more options than ever before.

I was therefore interested to learn about the Koho Extra Account, and ponder about whether its “premium prepaid” nature will capture the imagination of younger consumers.

Let’s dive in.

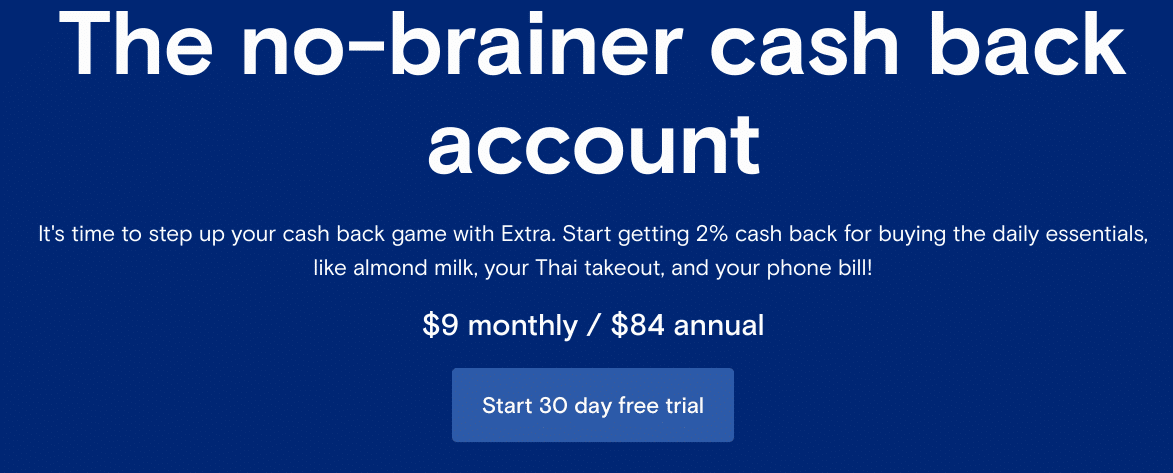

Koho Extra Account Features

Just by looking at Koho’s promotional materials, it’s pretty clear which demographic they’re targeting.

The Koho Extra Account is available to all Koho cardholders who already possess the base-level (free) version of the product. That same product already earns 0.5% cash back on all transactions, and is accepted wherever Mastercard is.

The Koho Extra Account is also aimed at millenial and Gen-Z customers who are familiar with the omnipresent subscription-based service model, hence the $9 monthly fee instead of the one-off annual fee that older-school products possess.

This upgraded version of the Koho Card provides the following features:

- 2% cash back on restaurants, cafés, bars, groceries, and pre-authorized payments such as phone bills

- 2% interest on the sum of the entire balance loaded onto your card

- No foreign transaction fees

- One free international ATM withdrawal per month

- $3 off Koho’s Credit Building Coach ($7 per month instead of $10 per month)

The name of this upgraded account has also been changed from Koho Premium to Koho Extra, and it comes with the now-ubiquitous vertical card design so common in the age of the cell phone cardholder case.

Where’s the Value?

Frankly, I don’t understand the unique value proposition that this product is supposed to bring. A flat rate of 2% cash back on three categories, plus 0.5% cash back on every other purchase, is already matched by the Tangerine Money-Back Credit Card.

In fact, the Tangerine card even lets you select the three categories you want to earn 2% cash back on, so you aren’t shackled to the restaurant, grocery, and pre-authorized payment categories.

Moreover, cash back is deposited directly into your Tangerine account rather than being provided as a statement credit, so you can use it for cash- or cash-like transactions.

If you meet the minimum income threshold requirements, you can even qualify for the Tangerine World Mastercard, which comes with a complimentary suite of insurance coverage as well.

Of course, the Tangerine products don’t feature no foreign transaction fees, so you’ll get dinged 2.5% on foreign currency transactions. However, if you must remain in the prepaid credit card space, why not then just use the EQ Bank Card, which is free and comes with no FX fees.

Why pay $84 to combine the features of two free products when you can easily just get both of those other products instead?

Personally, I think it’s a question of marketing, since every single millenial/Gen Z-oriented product is built as a subscription so the service provider can rely on constant revenue. Start-up issuers, such as Koho, therefore use a subscription model with which these younger consumers are familiar in order to monetize their product.

However, what’s the unique value proposition to the consumer? $84 a year could buy a cardholder a much better credit card, and in fact most mid-tier Visa or Mastercard products come with no annual fee for the first year anyway.

Anyone willing to spend money on a monthly basis could instead get the American Express Cobalt Card, which earns 5 points per dollar spent on groceries and dining at a cost of $12.99 a month – a 150% increase on earning in these categories for only a ~40% increase in fees.

Then there’s the question of interest – paying $9 a month to earn 2% interest seems pretty lame when some free savings accounts will often provide you with 5% interest, at least for a promotional period.

A Theorem on Prepaid Credit Cards

In my estimation, prepaid cards are almost only ever good for the issuer, because said issuer can collect the higher swipe fees associated with credit networks like Visa and Mastercard.

On the other hand, prepaid credit cards can’t be used at businesses that only take debit, which is an inconvenience for the customer. They also can’t be used to pay for services such as taxes, which also only usually accept debit.

Next, because prepaid cards are funded in advance with the customer’s real money, the cardholder therefore also can’t initiate chargebacks as easily as if they were using credit cards.

This is because credit card issuers tend to side with customers because transactions are initially made with the issuer’s funds, which the cardholder then promises to pay back. With prepaid products, this distinction is eliminated.

Moreover, prepaid credit cards don’t give you the ability to either hold onto debt (albeit at a hefty interest charge), or even to free up your personal cash flow. As much as we all hate paying interest, the 21-day interest-free grace period after a credit card statement closes can work wonders for cash flow management.

Oh, and if push comes to shove and you find yourself bereft of cash and hard-up on accessing your Canadian accounts in a foreign country, you can just stick your credit card into an ATM and take money out. You’ll pay hefty fees and interest, but sometimes $500 in dinosaur bills can be the difference between getting home or not.

A counter-argument could be made that debt is bad and it’s good to teach customers financially savvy habits. But then I have to ask: why pay Koho (or any similar issuer) $9+ a month for features that can be (mostly) attained for free by combining other prepaid products such as the EQ Bank Card and the PC Financial Money Account?

I can’t help but feel the entire business model of attempting to push prepaid products toward “premiumization” is doomed to fail, simply because it just doesn’t offer any kind of value that a financially-savvy Canadian can attain for free with limited effort.

Then again, perhaps people who value 2% cash back on almond milk via their favourite app-based payment solution aren’t a segment of the market that overlaps too much with those who compare every financial product in circulation.

Conclusion

Koho has launched Koho Extra Account. For $9 a month, cardholders gain access to 2% cash back on groceries, eats & drinks, and pre-authorized payments, as well as no FX fees and one free international ATM withdrawal per month.

This product might have some value to certain consumers, but for the moment I can’t help but feel that the entire prepaid card hype might just be a fad. This is the inevitable result of marketing that plasters “disruption” and “technology” on top of financial products that are inferior on every fundamental level to traditional credit and debit cards.

We will see as time goes on if Koho’s bet pays off. For now I remain skeptical.

Until next time, use payment methods that work for you.

Kirin explores the world through the lens of miles and points, sharing insights on premium travel experiences.

First-year value

$336

Monthly fee: $15.99

• Earn 1,250 points per month upon spending $750 per month for 12 months

Member Discussion