EQ Bank Launches New Prepaid Mastercard

The past 18 months have been rough for the prepaid credit card industry. Mogo abolished its rewards program, while Stack self-destructed by charging users foreign exchange fees.

I’m happy to report that there’s some good news in this section of the personal financial services market: the online-only institution EQ Bank has quietly launched their pilot prepaid card, and its features are pretty strong.

Let’s get into the details, and hope that this becomes the standard for new products in Canada.

EQ Bank Card: A New Prepaid Contender

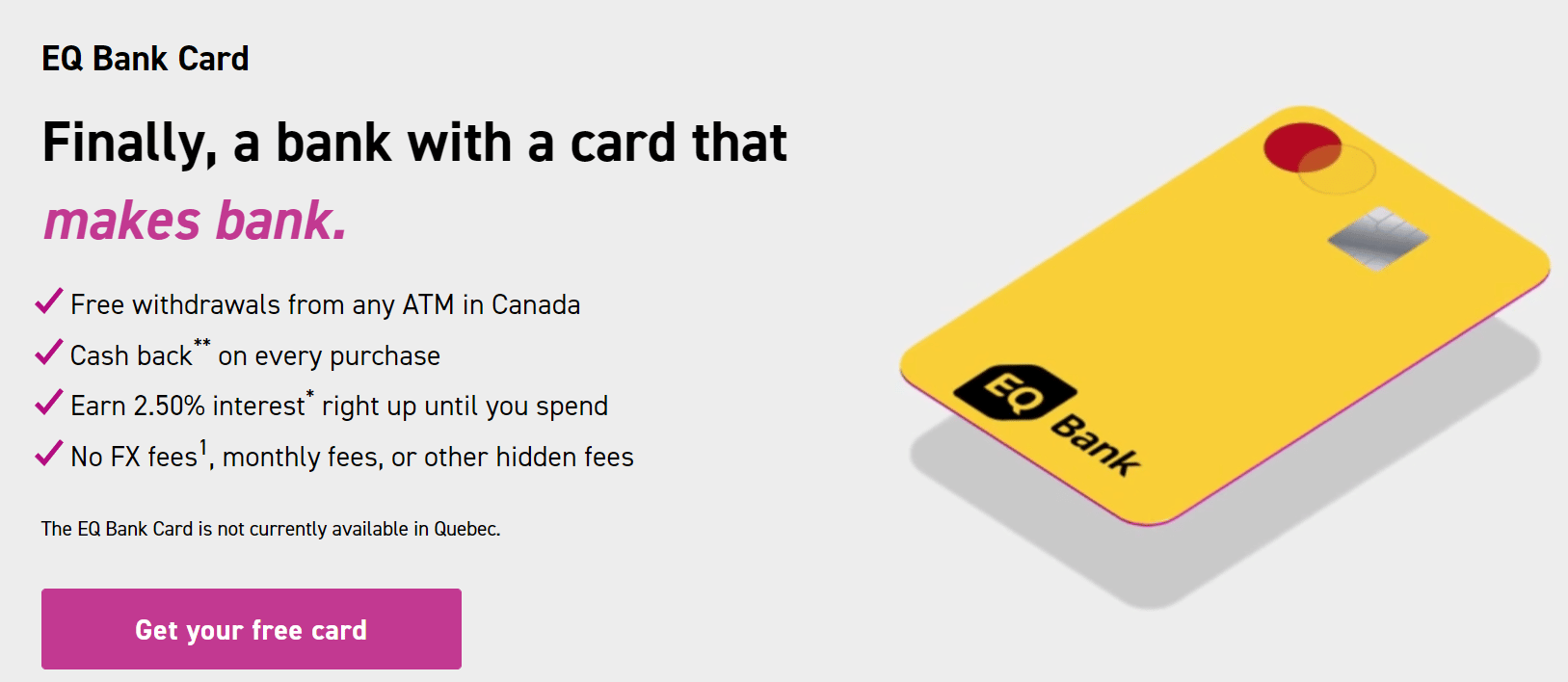

From EQ Bank’s own marketing materials, their new card is blasting out its proverbial gate at a gallop. Just take a look at the features:

To summarize the highlights, here’s what the card offers:

- No monthly or annual fees

- Free withdrawals from any ATM in Canada

- 0.5% cash back on every purchase

- No foreign transaction fees

Cash back equal to 0.5% certainly isn’t enough to turn this card into your daily driver – for that, you’d be much better off using a card with a higher rate of return, and with rewards denominated in a more valuable program. Also be advised the 0.5% cash back is paid out monthly to your EQ Bank Savings Account, which you’ll need to have in order to obtain and load the card.

Similarly, the 2.5% interest is also paid out to your EQ Bank Savings Account, and is calculated to the moment you spent whatever was loaded. That means you can allocate a slice of your savings balance to your spending card, without missing the opportunity to earn interest on that chunk of change before it is spent. (Note that this rate will fluctuate when EQ Bank adjusts their interest rate on savings accounts.)

While the cash back and interest features are handy, they hardly set the card apart. Instead, the card’s generosity on ATM withdrawals and foreign transactions are by far its most powerful elements.

Not only does the EQ Bank Card not charge ATM fees itself, but it will also reimburse you any fees charged by the machine. You’ll get reimbursed within 10 business days of making a withdrawal.

This “truly ding-free” perk also exists on the Charles Schwab debit card available in the US. It’s great to see this benefit coming to Canada for the first time.

Alas, the ATM reimbursement is only available on withdrawals within Canada, but I hope it comes to extend to the rest of the world – then this card would be a true must-have in any savvy traveller’s wallet!

For use out of the country, you’ll still reap the benefits of no foreign currency conversion fees. Transactions denominated in anything other than Canadian dollars are simply converted at the Mastercard rate, with no additional spread or surcharge. As per my reading of the cardholder agreement, this includes purchases as well as ATM withdrawals in a foreign currency.

Considering this card’s ATM advantages both at home and abroad, the EQ Bank Card gives the Wise Card, about which I’ve previously raved, a serious run for its money.

Despite my enthusiasm, it’s very important to remember that this card remains a prepaid option. You’re spending your own money via this platform, so you can’t use it for an interest-free grace period with a statement cycle, or as a credit-builder.

Moreover, as a Mastercard, even though it’s prepaid, you can’t use it entirely like a Canadian debit card. It won’t be accepted by merchants that only take Interac card payments, for example, as it will be processed as a Mastercard at the point of sale.

EQ Bank Quietly Making Waves

Even before announcing this card and all its myriad features, EQ Bank was already a favourite of many fiscally-minded consumers because of the high interest rates (often above 2%) that it freely offered to account holders, even providing high returns in the era of record-low interest rates during the pandemic.

What EQ Bank often received some critique for was that their accounts functioned as savings-only despite being billed as dual-purpose chequing and savings. There was no way to physically withdraw cash, and the company lacked a debit card or similar method for spending. For that, you’d have to transfer your money to another financial institution.

This makes me wish I’d been a fly on the wall during the conception of the EQ Bank Card. Did the company initially want a traditional debit card? Or perhaps a Visa/Mastercard-branded debit card? Or were they always going to go the prepaid route, but wanted the perfect moment to strike?

Whatever EQ Bank’s decision-making process, it’s good to see an actual competitive product launch on the market in the wake of so many devaluations. Many other prepaid products make you wonder what the unique value proposition of their card might be because they often seem rather identical, and rather watered down lately.

On the other hand, the EQ Bank Card’s obvious utility lies in its no foreign exchange fees, ATM fee reimbursements, high interest rates working in your favour, and seamless integration with your EQ Bank Savings Account.

Conclusion

EQ Bank has stealthily launched a new product – and what a product it is!

Between ATM fee reimbursements in Canada, the lack of foreign transaction fees, and cash back and interest at a competitive rate, the EQ Bank Card is one of the more interesting prepaid payment solutions I’ve seen. Here’s to hoping it holds up through 2023 and beyond.

There are no fees to get or keep the card. Existing EQ Bank customers can already order the new EQ Bank Card through the mobile app.

Until next time, don’t pay foreign transaction fees.

Kirin explores the world through the lens of miles and points, sharing insights on premium travel experiences.

First-year value

$336

Monthly fee: $15.99

• Earn 1,250 points per month upon spending $750 per month for 12 months

Member Discussion