How to Get Business Credit Cards

As you look to earn rewards faster, you may find yourself working your way through various credit cards until you find one that fits best. Programs like Aeroplan have many cards and partners, and you can accelerate your progress from a variety of sources.

Eventually, though, you might run out of personal credit cards to apply for, and at that point, it’s time to turn to business credit cards. Often overlooked, they can fit very well with your strategy as a valuable source of points. In fact, many of the welcome bonuses are highly competitive with premium personal cards.

But what if you don’t own a business? Fear not, as these cards aren’t as hard to get as you may think.

Who Can Get a Business Credit Card?

There are two types of business credit cards: small business cards, and commercial (or corporate) cards.

Commercial cards are issued by a company to its employees, and the company is directly responsible for expenses. The issuing bank provides the cards in accordance with its commercial lending standards.

For smaller companies, there’s a separate class of cards available to business owners, but issued by personal lending standards. You can qualify based on personal income, instead of business income.

Any debts on the card are the personal responsibility of the cardholder. Also, in Canada, the bank runs a personal credit check before approving the card, and the card reports to your personal credit file.

As far as banks are concerned, business cards are just another tier of qualification requirements, like Visa Platinum, Visa Infinite, or Visa Infinite Privilege, and the cards don’t work any differently from personal credit cards. But instead of asking for a high personal income, they ask for various documents depending on the structure of your business.

These cards are available to any type of business, including sole proprietorships, partnerships, corporations, and non-profits. Sole proprietorships are by far the easiest and cheapest type to register, and the easiest for credit card approvals.

Often, you’ll only be asked to prove your business registration. For example, here’s CIBC’s list of required documents for sole proprietors:

On the other hand, corporations need to show their finances and articles of incorporation. You might expect that it’s easier for larger, established businesses to obtain credit – in fact it’s quite the opposite.

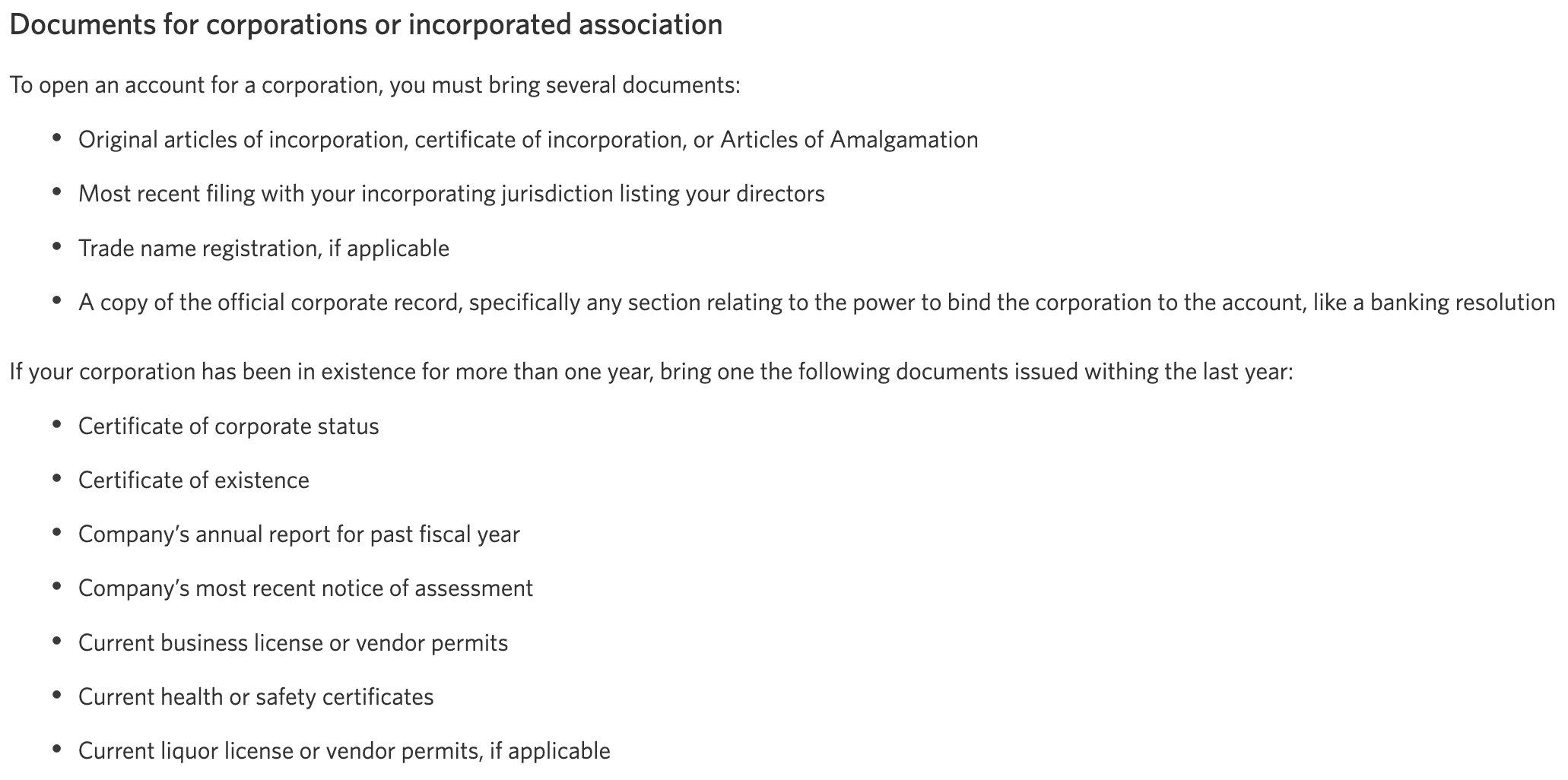

Here’s CIBC’s list of required documents for corporations:

Sole proprietorships are without a doubt the way to go if you’re just here for the travel rewards.

Any individual can start a business, and just about every business has expenses. You’ve got materials, phone and internet bills, marketing, gas, you name it. After all, you gotta spend money to make money.

So what does your small business do? Do you enjoy crafting or retail flipping? Congratulations, you now run an Etsy store.

Busy setting up mom’s new phone? Welcome to your new side hustle as a technology consultant.

Video game streamer? Gotta pay for a new webcam somehow.

Get creative – pick an activity close to your real life, even if you don’t intend to make this into a successful enterprise.

Where does your business operate? Not a problem for your little cottage industry to be at your home address. Keep it simple. No office, no employees, just a one-person travel award factory.

How to Register a Small Business

Most banks will ask for documentation when you apply for a business credit card. American Express is the exception in that they typically do not ask, but it never hurts to have just in case. Besides, it’s worth it for access to the business cards offered by other banks.

As a sole proprietor, you technically don’t need to register your business if you are doing business under your own name. However, I think it’s useful to register a trade name for your enterprise, because most banks will want to see this document anyway.

Each province has their own system for registering trade names, but they’re all basically the same. You’ll pay for the registration and to conduct a name search, which checks that your desired business name isn’t already taken, or confusingly similar to a competitor in the same industry.

There are slight variations on the terminology. In Ontario you’ll get a Master Business License, in British Columbia you’ll get a Statement of Registration, and so on. These all refer to the name registration document.

If a bank’s requirements use one province’s particular terminology, any of the equivalent variants would work.

Your provincial business name is different from a national business number. You may also hear the latter referred to as a CRA number.

You likely only need it if you’ll be collecting taxes on sales exceeding $30,000 annually (and you don’t need sales to have business expenses), or if you withhold payroll deductions (for your zero employees).

In most provinces, you’ll get a national number when you register provincially. In Quebec, you can register for a Quebec enterprise number instead. In Newfoundland and Labrador, there is no trade name registration – a national business number should suffice at the bank.

There are various fees and forms required to register a business. In particular, some jurisdictions require you to pay for a separate name search prior to registering.

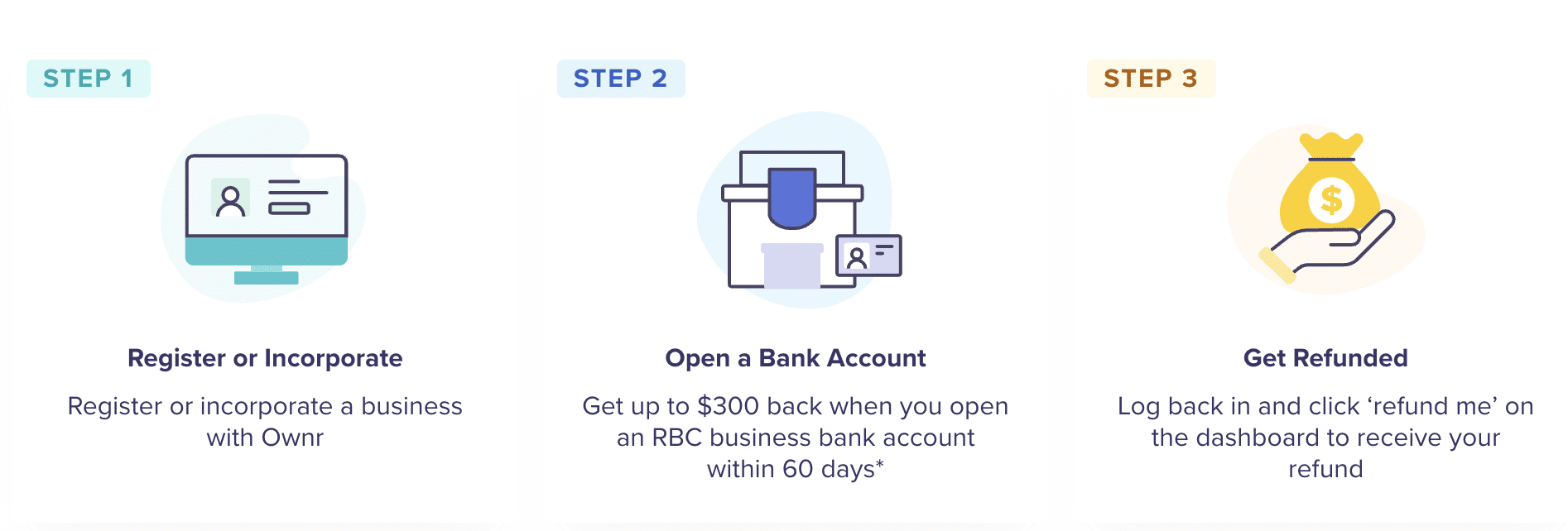

To simplify the process, Ownr offers a comprehensive service to register sole proprietorships and corporations. They also provide branding services, as well as perks such as up $300 cash back for opening an RBC Business Bank Account.

Ownr is currently available online for residents of Alberta, British Columbia, Ontario, and Quebec, with plans to expand to the rest of the country. A sole proprietorship registration costs $49 plus tax, depending on your province, and you can get a 15% discount by signing up for Ownr via Prince of Travel’s link.

For Canadians elsewhere, or if you’d prefer to tackle the forms yourself, here are the resources and estimated fees. Unless otherwise stated, you can apply online.

- National business number: free

- Alberta: $60, register in person

- British Columbia: $70

- Manitoba: $105

- New Brunswick: $112

- Newfoundland and Labrador: no provincial registration

- Northwest Territories: $20

- Nova Scotia: $130

- Nunavut: $50, register by email

- Ontario: $60 online, $80 by mail or in-person

- Prince Edward Island: $130

- Quebec: $38

- Saskatchewan: $50

- Yukon: $40

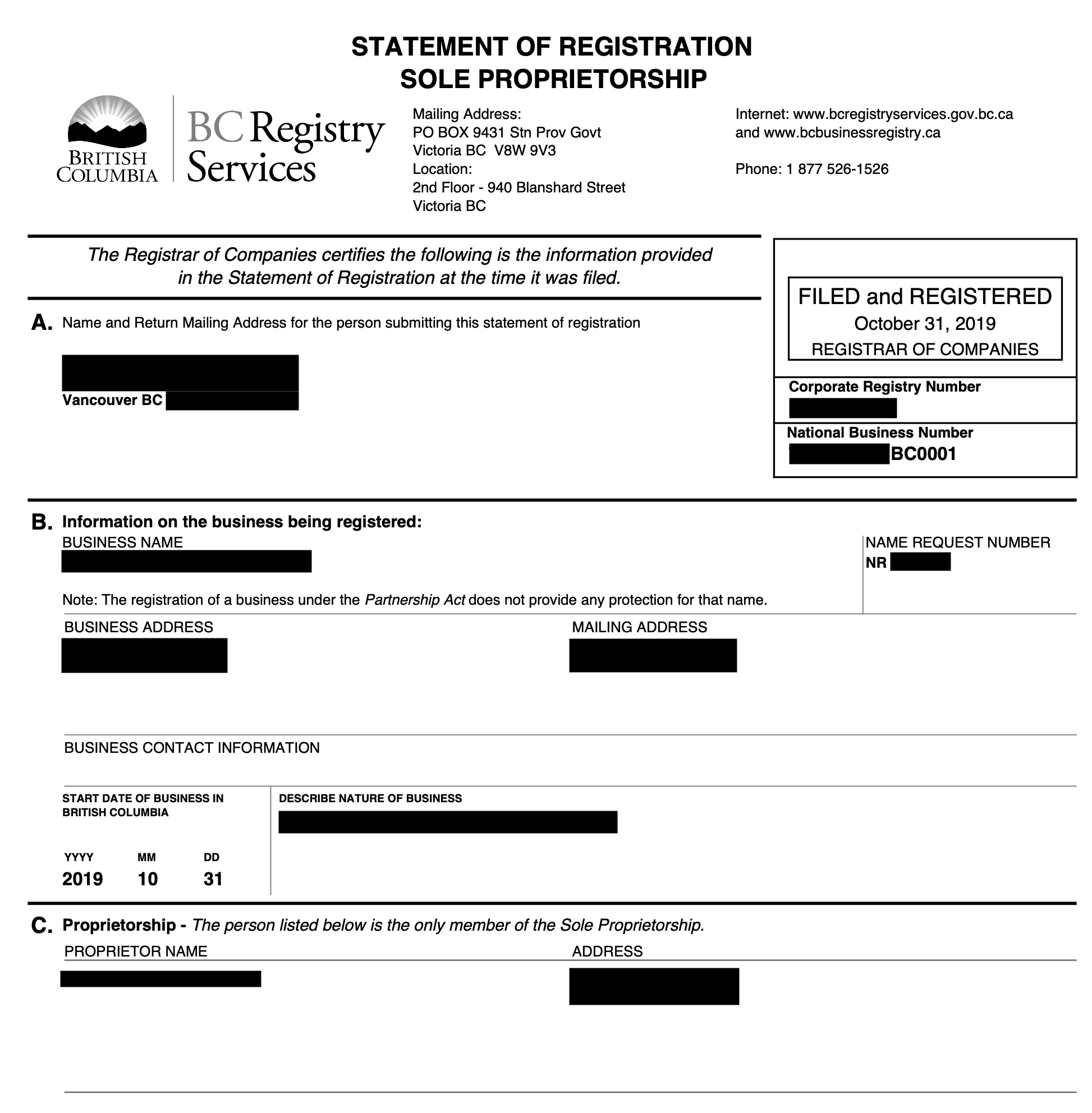

Personally, I obtained a BC Statement of Registration via Ownr, which I received about a week after applying. I’ve had no problems getting approved for business products from RBC, CIBC, and TD, as a brand new business, with no invasive questions asked.

- At RBC, I applied in person for a business bank account, and was also approved for any small business credit card of my choice. I provided my trade name registration document. At the time, the only other RBC products I held were personal credit cards.

- At CIBC, I applied online for the CIBC Aerogold Visa Business Card as my first CIBC product of any kind. I was asked to bring my trade name registration to a branch. The entire process took about a month, from application to receiving the card.

- At TD, I booked an appointment to open the TD Aeroplan Visa Business Card, but I was able to complete the entire process remotely with an advisor during the peak of COVID-19 closures. I wasn’t explicitly asked for my name registration or business number, but I offered those documents anyway. I’m a lifelong client at TD with plenty of personal banking products.

Altogether, there are three ways you can approach the bank as a sole proprietor:

- Unregistered, doing business as yourself: no fee; no paperwork

- National business number: no fee; complex government form

- Trade name registration: fees vary by province; multiple complex government forms yourself, or a simple web application via Ownr

Officially, most banks ask for the trade name registration. While it’s tempting to skimp on fees if you can, having a trade name registration will give you confidence for applying at any institution.

Without a name registration, you might be able to find a flexible banking advisor at some institutions, but I’d hate to waste a trip to the branch in case that fails. It’s always possible that they were misinformed, the credit department will delay (or deny) your card approval, or you may have to return with additional paperwork.

Even if you apply for a credit card online, you’ll likely have to visit a branch anyway to provide supporting documents and to create a business profile in the bank’s system. I see no reason not to just do the whole process in a single visit. I’d recommend booking an appointment and clarifying which documents are required beforehand.

Separating Your Affairs

If you have no aspirations of actually running a small business, you can easily use business credit cards to boost your rewards earnings.

For sole proprietors, there’s no need to separate personal and business income. If you register a trade name just to be approved for credit cards, and your business has no income, you won’t have any additional tax filing obligations whatsoever.

You also don’t need to distinguish between personal and business expenses. You can use your business credit card for personal expenses to your heart’s content, whether or not your business actually does anything.

That said, if you run an actual business, I’d advise not mixing business with pleasure, especially if your business is structured in any way other than a sole proprietorship.

Even as a sole proprietor, it can be an accounting nightmare to work your way through several business cards just for the rewards. Many business operators prefer to keep business expenses on a designated card, and meet minimum spend requirements on other cards (either personal or business) as usual with unrelated purchases.

Another advantage of keeping purchases separate: you can also deduct the credit card annual fee on your tax return as a business expense, if you use the card exclusively for business purposes. (Not recommended for CF Frost Consulting, pro bono credit card manager, and award travel booking agent for family and friends.)

Finally, it’s important to be aware of how the CRA treats credit card rewards on business cards. While in most cases points are not taxable, they technically do become taxable if they are earned by a business and given to an employee for personal use.

Unless your business is a sole proprietorship, it’s legally a separate entity from you. Points earned on a business card could be considered property of the business, even on a card that you’re personally liable for.

If you have any concerns about how points fit into your real business operations, be sure to clarify your situation with a tax professional.

Business Credit Cards to Consider

Just like personal credit cards, business card offers change from time to time. Here are a few worth keeping your eye on at Canada’s major banks:

Business Credit Cards

Welcome bonus: 75,000 Aeroplan points

Annual fee: $180

First-year value

$2,415

Welcome bonus: 70,000 Membership Rewards points

Annual fee: $199

First-year value

$2,001

Welcome bonus: 130,000 Membership Rewards points

Annual fee: $799

First-year value

$1,914

Welcome bonus: 40,000 Scene+ points

Annual fee: $199

First-year value

$1,300

Welcome bonus: 95,000 Aeroplan points

Annual fee: $599

First-year value

$1,147

Welcome bonus: 70,000 Aventura Points

Annual fee: $120

First-year value

$1,050

Welcome bonus: 100,000 BMO Rewards points

Annual fee: $149

First-year value

$972

Welcome bonus: 45,000 Avion points

Annual fee: $175

First-year value

$725

Welcome bonus: 110,000 Bonvoy points

Annual fee: $150

First-year value

$650

Conclusion

With so many good business credit cards available on the market, they shouldn’t be ignored any longer just because there may be a few more documents required along the way.

American Express typically doesn’t ask for documents on business credit card applications. However, to apply for business cards at Canada’s other banks, it’s very helpful to register your sole proprietorship first.

For an easy process, consider using Ownr to complete your trade name registration.

First-year value

$1,147

Annual fee: $599

Member Discussion