I wrote Getting US Credit Cards for Canadians exactly one year ago, and since then it’s become one of the most popular articles on Prince of Travel. I figured we’re due for an update, so in this post I’ll round up all the latest developments in terms of the optimal strategies for getting, managing, and maximizing US credit cards.

I’ve also kicked off our new Knowledge Base feature with a dedicated US Credit Cards section for those of you looking to get into the game stateside, and I’ll be keeping an eye out for the most pressing questions that people have about the topic as I expand Knowledge Base.

Is It Worth Getting US Credit Cards?

People often ask me whether US credit cards are worth their time. As many of you know, it takes quite a bit of effort to get everything going at the beginning – there are mail forwarding services to book, bank accounts to set up, ITINs to procure, etc.

The way I see it, getting into US credit cards is a long-term investment in your future points earnings. Indeed, while Amex US can be quite easy to get approved for at the beginning, other issuers may require at least a year of credit history to approve you, so this isn’t a quick process by any means.

Instead, one must recognize that the credit card market in Canada will always be rather limited when compared to our neighbours down south, so setting up a US credit file is a way to access both a much larger volume of signup bonuses and a much wider range of points currencies and frequent flyer programs.

Once you’ve completed the initial few steps and you’ve started to build a credit history, there’s really not much more work involved – it’s simply a matter of banging out a few credit card applications every now and then, similar to what you’d do domestically in Canada.

The New US Credit Cards of 2018

In the Managing US Credit Cards for Canadians article, I highlighted a few US credit cards that I thought were particularly worthy of your attention. 2018 has seen plenty of shifts in the credit card landscape, so what’s changed since then?

The American Express Premier Rewards Gold Card has since rebranded as the American Express Gold Card. The Premier Rewards Gold used to be a great first card to choose thanks to its first-year fee waiver, but nowadays the Gold Card’s US$250 annual fee is levied on the first statement, making it less suitable as an intro card – it’s now essentially a mid-tier premium card, offering solid earning rates and perks such as 4x MR points on US supermarkets and dining.

On the plus side, there’s a limited-edition Rose Gold colour available until early 2019 – how cool is that?!

Meanwhile, we’ve seen Amex make changes to their SPG credit card offerings in light of the Marriott–SPG merger that took place this year. You’ll now earn 75,000 Marriott points on the personal and business SPG cards when you spend US$3,000 in the first three months. The annual fee of US$95 is also waived for the first year.

In my view, the first-year fee waiver and the strong signup bonus make these very good choices for your first Amex US credit card (you can get them through a Global Transfer – see below). Moreover, since Amex signup bonuses in the US have strict once-in-a-lifetime policies, you don’t have to ever cancel these cards – the annual free night certificates can easily outweigh the US$95 annual fee, so you can keep these cards around to build credit history.

There’s a new SPG Luxury Card as well, but given the hefty US$450 annual fee, I don’t see this card as being worthwhile unless you actually have a lot of paid stays at Marriott hotels and can take advantage of the 6x earnings, the US$300 hotel credit, etc.

Lastly, Amex US has also elevated their Hilton co-branded products. There are three cards you can choose from: the Hilton Honors Card, the Hilton Ascend, and the Hilton Aspire. Out of these three, the Hilton Honors Card might be a great choice as an introductory US credit card as well, given the lack of an annual fee and the signup offer of 75,000 Hilton Honors points upon spending US$1,000 in the first three months.

Mail Forwarding: Shipito OUT, MyMallBox IN

Unless you’re one of the lucky few to maintain a US address or can rely on family and friends to forward your US mail, you’ll need a mail forwarding service to use as your US residential address. Shipito had been the fashionable choice until early this year, when data points began filtering in that they were refusing to forward credit cards in the mail.

It’s unclear how they knew whether each package was a credit card or not – some people reported Shipito asking them about the contents of their mail, while others claimed that Shipito just knew on their own. In any case, Shipito’s policy seems to have changed sometime in 2018 that credit cards need to be picked-up in person and could not be forwarded.

Fear not, because MyMallBox has emerged as a new contender for all your mail-forwarding needs. The Delaware-based service is NOT listed as a “Commercial Mail Receiving Agency” on the USPS website, which is what we want, since credit card issuers might otherwise refuse to accept its address.

Moreover, there’s an easy online portal for you to track which items have arrived and which you want sent to you, and you can even consolidate multiple items into one in order to save on shipping fees. There’s also no ongoing fee to use the service – only a small fee per package forwarded.

I’ve signed up for a MyMallBox account, but so far I haven’t switched over my US address to it yet. I’m still using 24/7 Parcel based in Niagara Falls, NY, which has been very good to me so far. However, they do charge an annual fee of US$95, so I really should switch over when I get the chance.

ITIN: Smashwords OUT, Amazon IN

The best practices for obtaining ITINs has undergone a similar change (consult the original US Credit Cards article if you need a refresher on what an ITIN is and why it’s important).

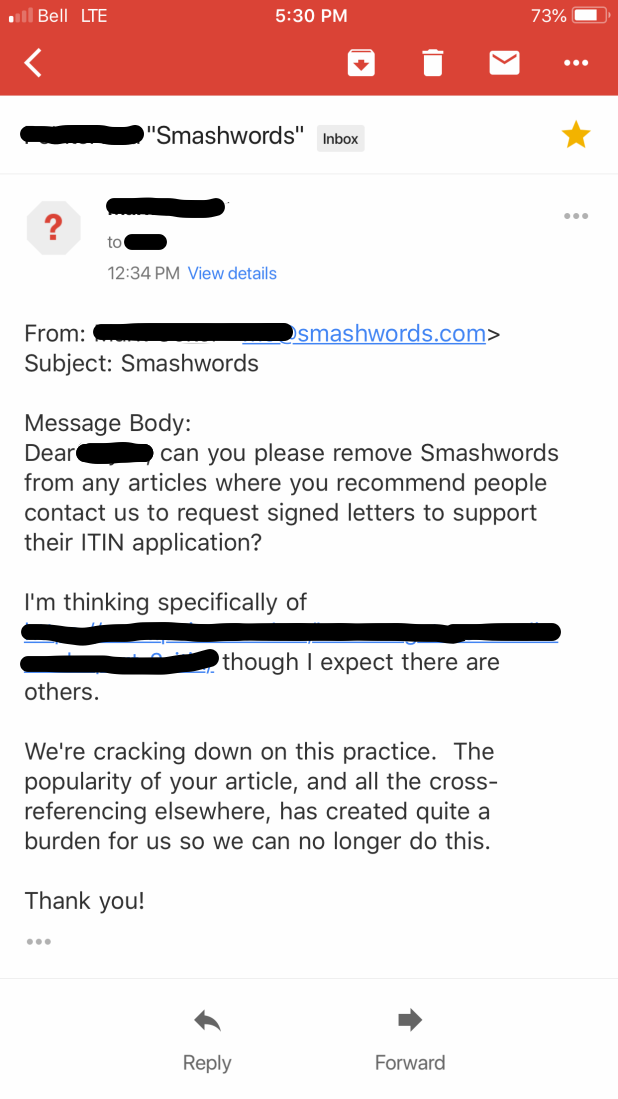

The prevailing method back in 2017 was to ask Smashwords, an eBook publishing company, for a signed letter to the IRS certifying that you were a foreign national using a US-based service and therefore required an ITIN to avoid withholding taxes. Nevertheless, Smashwords soon buckled under the pressure of so many Canadians asking them for ITIN letters:

Nowadays, the best method to obtain an ITIN support letter is through Amazon, who’ve made it super easy – almost too easy. They’ve made the ITIN document available as as download, so you just download the form and fill it in with your name and date. Once that’s done, you file it along with your completed W-7 form and your passport certified copy, toss it in the mail, and wait for the IRS’s response in 6-8 weeks.

As a reminder, you can either wait for your ITIN to arrive before you begin the entire US credit cards process, or you can get a head start through Amex Global Transfer (see below) and then “attach” your ITIN to your US credit file after you obtain it by including it on your next credit card application.

Can You Do Multiple Amex Global Transfers?

American Express prides themselves on being a global company, and one of the key perks they offer is the Global Transfer program, a seamless process that’s designed for individuals who are existing customers in one country maintain their Amex relationship when they relocate to a different country.

For Canadians looking to get in on the credit card action south of the border, Global Transfer represents a “shortcut” in the process. You don’t need an SSN or ITIN to initiate a Global Transfer; you just need a US address, a US bank account (to verify your US address), and a Canadian credit card account that’s been open and in good standing for three months.

In the past the strategy has always been to initiate a Global Transfer while you wait for your ITIN to arrive – this way you get a head start on the process of building your credit history. However, recent data points indicate that you can take this even further by initiating multiple Global Transfers from different Canadian Amex cards.

So for example, if you held a Platinum Card and an SPG Card here in Canada (both in good standing for at least three months), you could do one Global Transfer from each, thus obtaining, say, the Hilton Honors Card and the US-issued SPG Card. This way you’re now obtaining two (or more) juicy signup bonuses and building credit history with two (or more) accounts!

Note, however, that obtaining multiple Global Transfers isn’t completely necessary if you don’t want to go through the whole process another time. That’s because once you’ve gotten your first Global Transfer done and established a relationship with Amex US, you should be getting approved for more Amex US cards within a few months if you simply apply directly as a US resident using the online application.

Can You Get Approved by Chase?

Chase is the juggernaut of credit card bonuses in the US, so getting approved by them represents the ultimate goal. Unfortunately, they’re rather strict about how much credit history they require, so the road towards getting their approval is a bit of a slog.

I myself applied for the Chase Sapphire Preferred a few times before getting approved in November of last year, and even then it required multiple reconsiderations to get through. And now that I’ve been a Chase customer for a year (and my overall credit file is over two years old), I still can’t get approved for the Chase Ink Preferred or any of their business cards – I’ve applied and been denied thrice already, and I’ll be trying again soon and hoping for better luck.

I will say that having regular utilization on your credit cards is pretty important for building up credit history. Whereas in Canada you might apply for a credit card, meet the minimum spend, and then put it away in your drawer, it’s probably best to put a bit of spending on your US credit cards every month in order to demonstrate that you’re using your credit responsibly (instead of having no usage at all).

That’s been pointed out to me by the Chase reps as a reason why they don’t view my credit history favourably enough, so I’ll be looking to rectify that and hopefully get approved for more Chase cards in the near future.

Having an existing banking relationship with Chase also helps. If you ever find yourself down in the US, it may be worthwhile to visit a Chase branch and open a checking account – you can use your foreign passport and your US residential address. Word on the street is that Chase plays much more nicely with those who apply for their credit cards while also having other banking products with them, since it paints an overall picture of someone who’s recently “moved” to the US and looking to establish a long-term relationship with Chase.

Conclusion

The strategies for collecting points via credit cards changes rapidly here in Canada, and that’s even more the case if you’re looking to expand your operations down into the US as well. This stuff isn’t an exact science, so we rely on data points throughout the community in order to put together the latest picture.

I’ve brought you up to speed on the many changes we’ve witnessed in 2018 to mail forwarding, ITINs, Global Transfers, and which US credit cards to get, so now all that’s left to do is to go out and get them 😉

Great work, Ricky! Some applicants on Flyertalk reported that applying for US Amex cards via Global Transfer means giving up the signup offer of the card. Do your data points confirm this? If this is not the case, how should applicants proceed to request a ‘specific’ signup offer on the Global Transfer-dedicated website or one the phone? By ‘specific’, I mean even at a given point in time, Amex potentially offers 2 or more signup offers for the same card. On its website, I was once offered 50000 points and a couple of hours later, 35000 points for the Amex Gold…

Banks require a proof of a physical address to issue a credit card. In the case of BofA, the requirement was a physical address either in Canada or the US and a mailing address in the US. I’m getting conflicting information about the requirement from Chase: can the physical address be in Canada or does it have to be in the US? I think the physical address is a government regulation and therefore should not be different between each bank. Anyone has any more information on this? I have a mailbox in the US, but I don’t have a physical address and I’m not sure why it should be required. I think the Chase credit cards are very attractive to Canadians and I would like to know how we can meet the physical address requirement?

What happens if you dont meet the minimum spending requirement for the sign up bonus. Since most/all of the US credit cards are once-in-a-lifetime signup bonus if you dont meet the minimum spending requirement can you cancel the card and then a few months later sign up again and if you hit the minimum spend do you get the sign up bonus then? Or is it more along the lines you get 1 chance to hit the minimum spend to get the sign up bonus and if you dont make it you are out of luck forever?

What US Banks are available for us? BMO/Harris Bank, TD/USD Accounts, Hubert Financial US dollar accounts (Online only)

US Credit History, this isn’t pulled by Canadian Banks when you apply for Canadian Financial Credit products correct?

RBC and CIBC have USA accounts that you can get as well. And correct.

I live in Canada and since 2011 I have a Royal bank of Canada US$ account in Canada and a RBC Bank (Georgia) US$ Visa card and US$ account with that US bank. When I first obtained the RBC (Georgia) US account – they did not ask for an ITIN number – and now when I use Credit Karma I see Trans Union has my CDN SIN number associated with my US mail forwarding address – and my RBC Bank (Georgia) Visa card. I obtained an ITIN number a few years ago – and last week I tried to get a Chase Freedom credit card – using the ITIN number and my US mailing address. I could see on Credit Karma the Chase ‘individual’ credit inquiry on me – yet Chase denied my credit card application saying they ‘could not access my credit history’. I kind of think the issue could be the credit bureau has my Cdn SIN number on file – and not my ITIN number. Do you know of a way to get the credit bureau to update my file – and either add in my ITIN number alongside my CDN SIN number -or- replace my CDN SIN number with the ITIN number?

So I’ve been declined twice now by using these guides to fill out the form/ with the documentation. Everything i’ve submitted is exactly correct and not sure what to do. When I call the IRS they tell me i was declined because of "Exception document". Any advice? Im using the letter Amazon gives us to download!

Does anyone have updated instructions on filling Form W-7? Seems that people are getting denied more often using Pointsnerd’s.

Unfortunately, my first application of Hilton Honors was pending for income verificaitons despite having US address and SSN. Will give it a try with SPG personal and call the GT line tomorrow and see if they can approve both of them at one shot using my canadian history (i have AMEX Platinum, Gold active in good standing though)

MyMallBox is a no go. Just signed up for an American Bank Account and MyMallBox has confirmed they will not accept credit cards. From MyMallBox:

“Due to an overwhelming influx of credit cards being sent to MMB, we feel we must address this issue with our customers.

Currency is one of the Prohibited Items that we can not ship under any circumstances and credit cards and bank cards fall under this category.

Please contact your credit card company to send your credit cards directly to your home.

We are sorry for the inconvenience this has caused you.”

Hi Ricky

I applied for Chase card, they ask for proof of physical address like a utility bill or Govt ID, I have already sent bank statement and Amex statements but I don’t have utility bill or ID with U.S address. Any ideas? Thanks

Hi! Did you eventually get your Chase card?

Will a lease agreement work?

My wife and I successfully got our ITINs and then got our first US amex cards using global transfer. I don’t remember amex asking us for our ITINs when we applied though. How can we be sure that our credit file is linked to our ITIN to build credit outside of just amex?

Hi James,

Did you use the Amazon method? Does it still work?

You’ll have to include your ITIN on your next credit card application.

Hi Ricky,

There’s been recent Data Points saying that MyMallBox does not forward credit cards anymore to Canada. Is there any other options?

Also looking for other options! I’m in Montreal so 24/7 parcel is not practical.

I’ve been using 24/7 Parcel and have no issues so far, although they do charge an annual fee.

Hi Ricky,

Thanks so much for sharing all of this information. I’m just going through the process now and just wanted to clarify if we needed to fill in the area in Form W7 where it asks: "additional info for a & f – enter treaty country and article number. I did check off A & H and wrote that it was an amazon requirement for income generation. But I’m a bit lost on that bit of the application.

Hanna,

Did you receive the ITIN?

Hey Ricky, thanks for the update, always enjoy reading your blog.

Just wondering, have you had any difficulties getting credit cards using "PMB" or "#" in your address? I noticed that you use 24/7 parcel which uses this format of address and wasn’t sure if the banks use this as a method of screening addresses as well.

Thanks!

I usually go for "Unit" instead of "PMB". Works just fine and 24/7 processes it without issues.

Just a question for those who have successfully leveraged Global Transfer more than once – I successfully did my first Global Transfer almost a year ago with a no fee Amex and got the SPG business card a few months after that. I did try applying for the SPG Personal card (but they asked me to fill out a 4506T which I understand you can decline and reapply later without them asking for it again) and then the Amex Gold Card which was declined.

So I tried calling Global transfer number again a couple of days ago and the first question they asked me was whether I had an Amex card before (I presume they meant a US Amex card). I didn’t want to lie so I said yes, but asked if I could still do a Global transfer. They said they would submit the application as a "regular" application and if it went to "pending status" then they would look into my Canadian credit history. That didn’t really make sense to me so I just thanked them for their time and hung up.

What have other people’s experience been on this?

Thanks!

Hey Ricky! The post is very helpful and it helped me get Amex SPG card approved without ITIN but just with Passport no. But i would like to get ITIN to apply for other credit cards. I have some questions regarding the ITIN application (Maybe you should write an article on getting ITIN). In ITIN Application what do you select from a-h check mark the first section. Another clarification ..what address to use in the ITIN application US address/ Canadian or both.

If I remember you should check a and h, and write the exception alongside h.

Meanwhile use your Canadian address since the point of an ITIN is to show you’re a foreign resident who needs to be exempt from withholding taxes.

Hi Ricky,

My ITIN application got rejected. What do you fill in the Exception alongside h. I will have to correct it and resubmit it again.

Hey Ricky! First off, thanks for all the amazing work you have put together. I just went through multiple articles on your blog this morning and made quite a difference in our travel hacking adventure.

For someone who lives between Vancouver and Toronto for a majority of the year, and just getting started on this process, would you recommend going with 24/7 Parcel? OR just start with an account on MyMallBox.

My girlfriend will be doing this with me. So will we have to get 2 separate accounts in either case?

Appreciate you and your willingness to share with us 🙂

Jay

Great series, thanks! I run a business that mostly operates in USD, and I’d like to get an Ink Preferred for my business spending.

I already have an ITIN, and an RBC USA credit card that I’ve had for 5 years. In your experience, will this help a lot with chase, or are they looking for multiple cards in the credit file?

Also:

Thanks again!

Multiple cards would certainly help but with a five-year history I think you have good odds of getting approved.

Yes, the 5/24 rule only applies to US cards – the US credit bureaus can’t see your Canadian activity. And Chase does accept ITIN, except many Chase employees have never heard of an ITIN and will say that they don’t. In reality you just enter the ITIN in the SSN field and it serves as the identifier.

One thing I’d love someone to address is the legality or morality of applying for US credit cards as someone who is not American and does not reside in the US. Are there things we need to lie about in order to go through with this process? Or are we doing something that’s completely above-board?

Hi Tim, I respect people who think about legality and morality because there are some who are so obsessed with points, they abuse the system. I obtained a US AMEX card, and now have two, because I have a seasonal residence in the US. I had a Canadian issued US $MC that didn’t provide any benefits. I called US AMEX and asked for a card. I was forwarded to a more senior department and they checked out my Canadian AMEX history which dates back to ’09. They saw that I was a good member, I supplied my US address, answered a few questions, and was completely above board in providing information. It amazes me though, that with all the US AMEX offers, I benefit a lot more from 4-5 months of using US AMEX than I benefit from 7-8 months of using my Canadian AMEX card. I am really disappointed in how little CND AMEX does for its members compared to US AMEX.

That’s a good point Tim.

I can see how there’s an element of misrepresentation here. The credit card issuers require you to be a US resident in order to get the cards, but their only way of verifying US residency is by checking for a valid mailing address, so you’re basically holding your hands up and saying "I’m a US resident!" despite not being one.

It all depends on what you’re comfortable with doing at the end of the day. Perhaps a post on "The Ethics of Miles & Points" would be fun to write.

That would be fascinating. I think there would be two reasons to consider an article like that. The first would be to avoid potential legal issues. It sounds to me like, in theory, there could be something fraudulent in applying for a card in a country for which you’re not a resident. If it’s fraudulent, there’s a chance of legal ramifications. It would be good to assess risk. The second reason would be to help people consider moral issues. I think some people would like to know what’s fully moral and what’s crossing lines into grey areas (and maybe into full-out wrong). Of course I’m not sure our society has a common basis of morality for us to build upon anymore, so it seems like each person kind of needs to construct their own…

Either way, I’d love to read an assessment of what’s legal and not and what’s moral and not. That would be really helpful for people just getting into this!

Hi Ricky:

Very helpful!

Hopefully you can do an article on the US cards you carry and how you decide on which card (US vs. CAD) to use for spending.

I was just approved through the Global transfer for the Hilton Honor s Amex, and US SPG Amex. I have followed your road map, and done everything except send the forms for the ITIN. My question is can I build credit history with these cards without applying for the ITIN, or will I ultimately need an ITIN for additional cards/applications?

You can build credit history without an ITIN using only Amex cards, but the problem is that other issuers won’t be able to find your credit file properly without an ITIN as an identifier. So if you’re content with the US Amex cards for now then an ITIN isn’t a priority, but if you do want to expand into Chase/Citi/BoA cards then you’ll want to get one.

Yo Ricky –

I approached a couple of Chase bank locations while visiting in Scottsdale and Sedona this past spring, and the Brick-&-Mortar guys use the same online apln that is used on the web. After giving a relative’s US-based address, I get stumped at the SSN which is a mandatory input field; the ITIN doesn’t cut it. Is there a work-around method so I can get the generous Marriott sign-up points ? Thx !

Hey James, have you had any luck with using entering the ITIN in the SSN field as Ricky suggested? I don’t want to accidentally enter some poor bloke’s SSN because it shares the same numbers as my ITIN.

I don’t believe this will be a problem since ITINs begin with a 9 and SSNs never do.

Just enter the ITIN in the SSN field. They’re both 9-digit identifiers with the same format and they serve the same purpose – as an identifier for the credit bureaus.

Hey Ricky,

You mention that GT can be done twice. Wondering if it’s advised to wait a certain period of time prior to doing your 2nd GT? Wife and I have a large purchase coming up and I’m hoping we can each to the US SPG personal and SPG US Business at the same time.

I don’t think a certain waiting period is necessary – as long as you’re initiating the GT from two separate Canadian Amex cards it seems to work.

Can you combine points balances with existing accounts from Canada? (MR, Mariott, etc.)

For MR, you’re allowed to transfer between US MR and Canadian MR at the prevailing exchange rate. This doesn’t seem to be a well-documented process, so I might give it a try soon to write about how it works.

For other loyalty programs (Marriott, Aeroplan, etc.), yes you can transfer MR points from both countries to a single account.

Did Chase keep asking you for a copy of a utility bill as a proof of the US address ?

Yes – first they wanted a US driver’s license (which I don’t have), then they asked for some kind of bill for address verification. I used my TD Bank statement.

Curious your thoughts on the US TD Aeroplan Visa Signature card that Canadians can apply for via fax or mail? 25,000 AP, FYF, $1000 MSR, and no SSN/ITIN needed. It’s never mentioned by any of the Canadian bloggers when referencing US cards so figure there must be a good reason.

It’s a good offer – I mentioned it in my original Getting US Credit Cards for Canadians article as a good way to get started. You’re right that it does deserve more attention though!

Perhaps a dumb question, but I assume for US cards you also need a US bank account in order to pay off the card?

You can actually pay off US cards from certain USD accounts of Canadian banks. I know BMO does this with their USD accounts. However, a US bank account is useful to have for address verification purposes.

Thanks!

Thank you!