The Best Credit Cards for Rebuilding Your Credit

Finances aren’t easy, and it can be difficult to find balance with busy modern lifestyles. Currently, many of us feel strain on our pocketbooks, and when combined with financial instruments such as unsecured credit cards, this can lead to a spiral of debt and even worse.

If you’ve made mistakes in the past and are trying to repair your credit history, then you’ve come to the right place. In this article, I’d like to offer folks who might be getting back into using credit responsibly some excellent credit card options.

Even if you have a less-than-stellar credit report from TransUnion or Equifax, there are still some tools available to you to help rebuild your credit score.

Why Get a Credit Rebuilding Card?

Everyone is on a financial journey. If you stumbled enough to affect your negatively, don’t fret. You can better this situation, and the good news is that second-chance lenders in Canada are often the furthest thing from second-rate.

If you find yourself in need of a lending product from a more forgiving creditor, do yourself a favour and know the types of products you’re looking at to begin with.

There are two options for you to consider: secured credit cards and unsecured credit cards. The former requires you to put up a security deposit, while the latter are products from lenders such as Capital One who are known to specialize in looking past financial mistakes, but don’t require a security deposit.

This first type of product, secured credit cards, will require a security deposit beginning from as low as $50, but usually starting around the $200–500 range. This is done to make sure you don’t abscond with the bank’s money.

Secured Credit Cards: What You Need to Know

Read moreThe second category, unsecured credit cards, usually requires you to have a slightly higher credit score. This creates a longer distance between you and any bankruptcies, consumer proposals, or missed or late payments.

In either case, the act of having a credit card should report your responsible spending to the credit bureaus, TransUnion and Equifax. When you pay your balance down on time and in full, and refrain from overleveraging your available credit, then you’ll see your credit score, and thus your access to credit, increase over time.

Just remember you can’t get a credit card if you’re in the midst of a bankruptcy or consumer proposal – only afterwards, and only with a lender who will accept you.

Also note that throughout this article, I’ll be referring to the best version of a credit card that it’s possible for a customer to get. If your income or personal credit history don’t qualify for the the more premium iteration of one of these products, don’t worry.

The less prestigious versions of these cards still offer excellent value, and will help you on your path to a fresh credit restart. Once you build up your credit score, you can always revisit the more premium versions of the cards.

Are Rewards Programs Worth It While Fixing Your Credit?

The next thing you should consider before getting a secured or unsecured product is any potential rewards program it may offer. Not every credit card in this financial recovery category offers consumer rewards, and those that do will often be hesitant to offer their most optimal products to consumers with a few hiccups in their past.

Ask yourself a few honest questions before applying for a rewards card:

- Do you need a rewards program to make it worth your time?

- If you’re eligible for a product with some consumer kickbacks, do you think you can trust yourself to not overspend in hopes of earning more rewards?

- Most importantly, will you avoid paying interest, because interest will often offset the benefits of rewards points?

If you can answer each of these questions in a positive fashion, then go for it. If you still think you have a little work to do, there’s no shame in taking a temporary break from the Miles & Points game as you get your credit report in order.

There will always be more opportunities to come, and we’ll be here to share them with you when you’re ready.

Also remember that sometimes your home bank, or a bank that wishes to build a relationship with you, may offer you a secured version of one of their premium cards even if you normally wouldn’t qualify.

This is very much subjective to your personal situation, so don’t rely on it. It might be a good idea to check with your banker before applying for something on this list.

Tried & True: Capital One Guaranteed Mastercard

The first card on our roundup is a no-frills option that comes with zero bells and/or whistles: the Capital One Guaranteed Mastercard. The reason that this card is attractive is right in the name: for an annual fee of $59, you’re guaranteed to get a Mastercard credit product.

The credit limit will be contingent on your payment history. If you’ve had recent or significant credit problems, such as a bankruptcy or multiple missed payments, you can expect this limit to be low. You may also be required to provide security funds for the secured version of this card.

Still, this card offers you a guaranteed second chance to start rebuilding credit now rather than later, and at a simple, low annual fee.

The card’s annual percentage rate (APR) weighs in slightly below the industry standard at 19.8% APR on purchases, a hair beneath the normal 19.99% of other credit cards. Interestingly, balance transfers also incur a fee of 19.8% instead of the 21.9% for cash advances.

The purchase and balance transfer interest rates can be reduced to 14.8% if you increase your annual fee to $79 annually – but I think it’s better to save $20 and avoid racking up any interest at all.

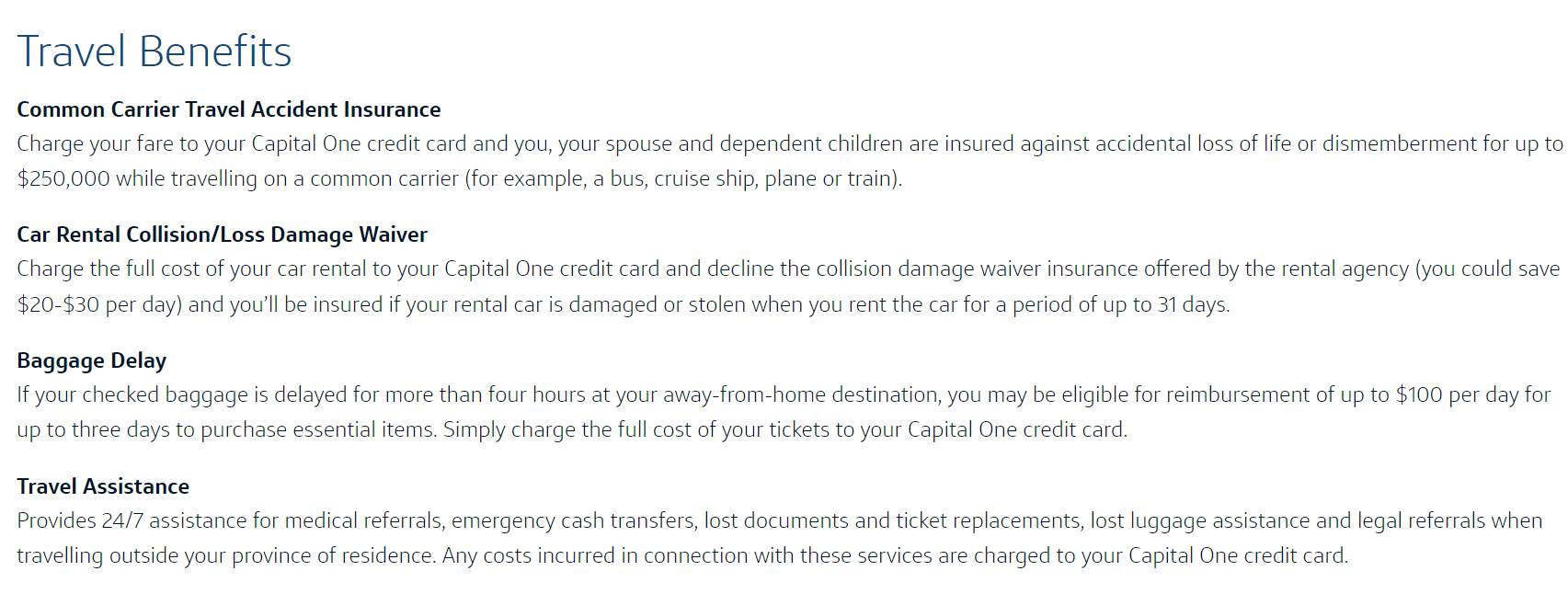

Interestingly, even the guaranteed version of this product comes with a suite of travel insurance, including baggage delay insurance, and rental car loss-damage collision waiver. Not bad for a credit card of last resort!

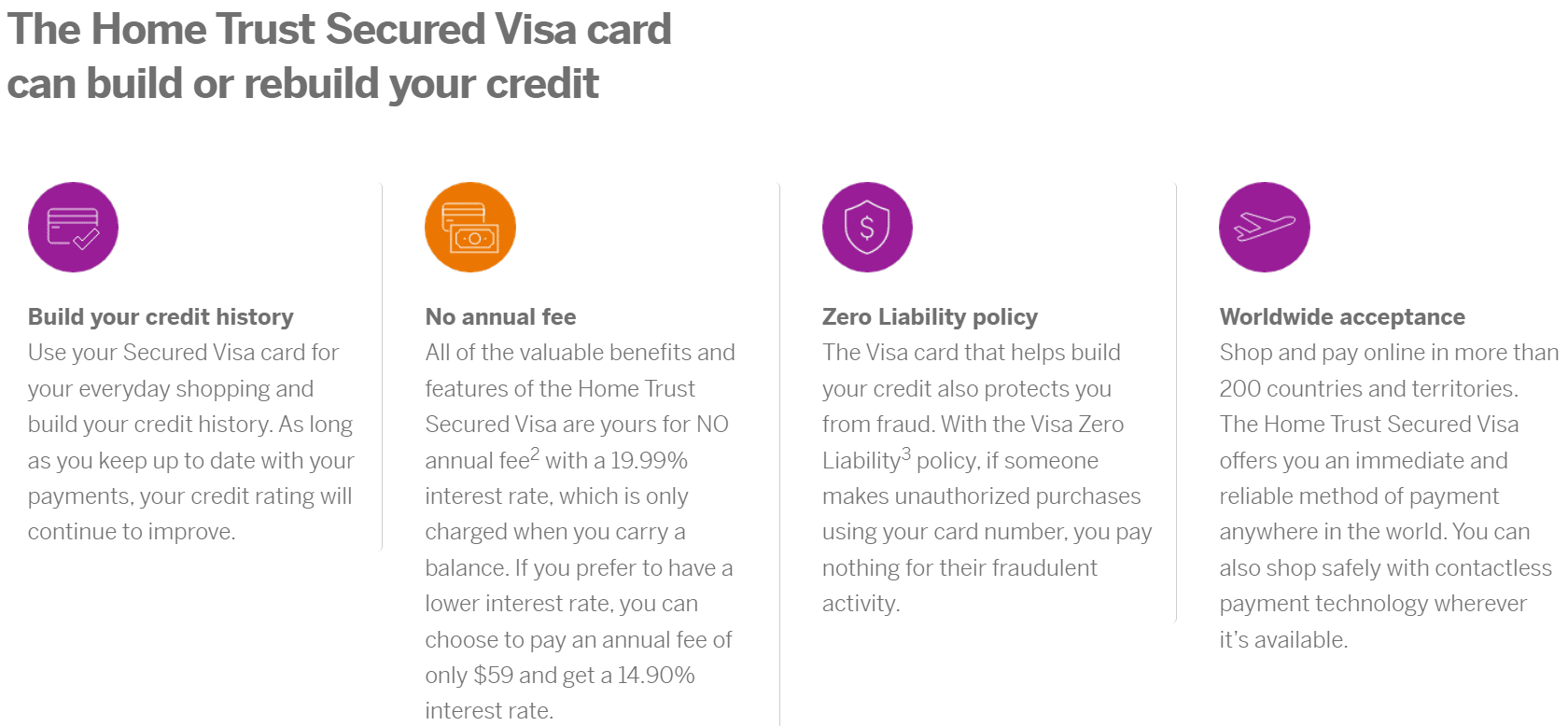

The Best No-Fee Secured Credit Card: Home Trust Secured Visa

Next up is the Home Trust Secured Visa. This has even fewer bells and whistles than the Capital One Guaranteed Mastercard: there’s no insurance to speak of, the card isn’t available in Quebec, and you must make a minimum annual income of $15,000 in order to qualify.

Even with this in mind, I think this is the best no-fee secured credit card on the Canadian market.

This is because it’s from a lender, Home Trust, that has been known to double-check things like paystubs religiously, but still offers decent products to customers who pass their vetting process. This particular credit card requires a security deposit starting at $500, which might be hefty for someone getting on their financial legs again.

Once approved, you can expect a standard purchase APR of 19.99%, but you can also opt to pay a $59 annual fee to reduce the APR to 14.9%. Once again, I’d skip out on this option.

This card carries mobile wallet support, so you can add it to Apple Pay or Google Pay.

Assuming you want to dodge the annual fees and your home bank isn’t offering a no-fee secured version of one of their cards, I’d pick up the Home Trust Secured Visa in a heartbeat.

Close to Greatness: Neo Financial Secured Credit Card

The Neo Secured Credit card is, at least to my eye, identical to its non-secured cousin. While there are no insurance coverage or perks to speak of, there is a partner-based cash back rewards system, and the minimum rate of cash back you can earn on any transaction is 0.5%.

Neo boasts that the “average” cash back with their partners is 5%, though if you don’t want to buy goods or services at their specific partners, this does you little good. Still, it’s at least a straightforward rewards program.

Better yet, approval is guaranteed according to Neo, with security fees starting at only $50. However, your credit limit is equal to the funds you’ve laid aside, so don’t expect Neo to provide you anything above your collateral.

On the plus side, there are no annual fees to speak of, and the APR ranges from 19.99–24.99%, depending on your personal situation.

You also have the opportunity to upgrade to the full version of the Neo card, should you be a client in good standing for an undisclosed period of time. This could be months or years since your last derogatory credit report, but in such a situation, your security funds will be returned to you in full.

Proceed with caution, should you choose to apply.

Great for Groceries: PC Financial World Elite Mastercard

Next up is an unsecured credit product close to my own heart, because I do a lot of shopping at Superstore: the PC Financial World Elite Mastercard. Forget about the 20.97% purchase interest and the 22.97% cash advance APR (21.97% in Quebec) charges, and focus on the rewards.

In partnership with the PC Optimum program, which can be redeemed for cash at the same partners at which you earn the points, this products garners the following rewards at the low rate of $0 per year in annual fees:

- 45 PC Optimum points per dollar spent at Shoppers Drug Mart (an effective 4.5% return, the highest pharmacy earn rate in Canada)

- 30 PC Optimum points per dollar spent at Loblaws-banner grocery stores (3%)

- 30 PC Optimum points per dollar spent at Esso and Mobil gas stations (3%)

- 30 PC Optimum points per dollar spent at PC Travel (3%)

- 10 PC optimum points per dollar spent everywhere else (1%)

If you apply between now and September 11, 2022, there’s also a promotion for 75,000 PC Optimum points, worth $75, after completing your first purchase.

On top of this, the card has a bevy of basic but serviceable insurance, such as emergency medical treatment, extended warranty, and purchase protection. These last inclusions can be quite worthwhile, especially considering that Shoppers Drug Mart sells various mid-range electronics, such as the Nintendo Switch.

PC Financial has a track record of being charitable to folks who’ve had less than stellar credit history, including with late payments. Once again, a second-chance financial institution proves it has products that can compete with Big Five products any day of the week.

And if you don’t qualify for the World Elite Mastercard, there are always its little cousins to tide you over until you do.

Loaded with Perks: Triangle World Elite Mastercard

Last, but certainly not least, on our list is the Triangle World Elite Mastercard. Canadian Tire Financial Services (CTFS) is known to be a generous lender, though it can be stingy with initial credit limits.

Once again, ignore the 19.99% APR, and focus on all the bonuses this card can offer.

You may have been annoyed in the past by random salespeople at Canadian Tire trying to get you to sign up for a credit card while you’re just trying to buy a leaf blower. Next time, it might be in your best interest to slow down and listen to their spiel: this is one of the most feature-laden credit cards on the entire Canadian market.

Let’s take a look at the earning rates:

- 4% back in Canadian Tire Money (CTM) at Canadian Tire stores (including Sport Chek, Atmosphere, Pro Hockey Life, and Mark’s Work Wearhouse)

- 3% back in CTM on groceries (excluding Walmart and Costco)

- 1% back in CTM on all other purchases

- 5 cents in CTM per litre of gas (7 cents in CTM for premium) purchased at Canadian Tire gas stations

Aside from earning stacks of Canadian Tire Money, this card also comes with other interesting features:

- Free Canadian Tire Gold Roadside Assistance (A value of over $100, which includes multiple tows/battery boosts each year)

- Priority concierge line as a World Elite Cardholder (the CTFS customer service is the second best in Canada after American Express)

- A bill pay feature to pay select taxes or bills via with your Triangle World Elite Mastercard for no additional fee (0.4–1% back in CTM)

- Optional 24-month no-interest payment plans on all purchases over $150 at any of Canadian Tire’s stores

- Car rental loss/damage waiver, purchase protection, and extended warranty insurance

This is an overwhelming slew of amazing functionality in one card. Even the basic version of the Triangle Mastercard accesses most of these features, which is great if you don’t qualify for the World Elite.

This is a great way to rebuild your credit, and I’d argue that the host of perks puts most of its competition to shame.

Conclusion

This wraps up our round-up of credit rebuilding cards, and while it’s a decisive win for Mastercard, keep your eyes out for any Visa products that might come to market in this category. Hopefully, you’ve found some superior solutions to some of the frankly inferior secured or “second chance” products available today.

While I encourage financial prudence in all matters, it’s also true that once-in-a-while mistakes or the unfortunate side effects of this thing called “life”, happen. There’s no reason in such situations that you should feel down on yourself, or that you as a consumer need to be shackled to second-rate or shady lenders.

Always do your research and take your hard-earned dollars to the best issuer for your needs, who can also come to terms with any past issues you’ve had as you rebuild.

Until next time, keep those credit card statements paid in full and on time.

Kirin explores the world through the lens of miles and points, sharing insights on premium travel experiences.

First-year value

$336

Monthly fee: $15.99

• Earn 1,250 points per month upon spending $750 per month for 12 months

Earning rates

Key perks

- Transfer to airline and hotel partners

Monthly fee: $15.99

• Earn 1,250 points per month upon spending $750 per month for 12 months

Earning rates

Key perks

- Transfer to airline and hotel partners