Which Credit Cards Are Best for Low-Cost Airlines?

While low-cost carriers have earned a bad rap in Canada, they are a way of life in many parts of the world, especially in countries where they’re integral to connecting cities, islands, and communities.

However, despite these carriers being an important part of the aviation industry, flying with low-cost airlines does come with accepting certain realities – like the lack of free food and drinks, no rewarding loyalty programs, and strict baggage rules that feel more like traps than policies.

There are also somewhat unique risks to flying with low-cost carriers, especially with regards to delays and cancellations.

Fortunately, as we’ll discuss below, there are great credit cards in the Canadian market that you can leverage to mitigate the realities of flying with low-cost airlines.

The Realities of Flying with Low-Cost Airlines

To understand the realities of low-cost airlines, you need to know that the low-cost model hinges on selling unbundled fares at low sticker prices in hopes that you’ll eventually pay more through ancillary fees like baggage, seat selection, and food.

However, it’s also perfectly fine if you’d prefer to go for the absolute bare minimum fare – as long as you set your expectations accordingly, and more importantly, follow the airline’s rules to the letter, especially when it comes to bag sizes.

We in Canada aren’t as used to low-cost carriers as the rest of the world. We’re used to having meals, snacks, or at least beverages when flying, and we’re used to having a carry-on included with our fare. That said, Canadian airlines have clearly been taking notes, quietly rolling out “ultra-low-cost” fares that somehow don’t include the one thing you need most: your bag.

So when a carrier like Flair Airlines strictly enforces its personal item size and charges for water, people naturally feel indignant, and many reminisce about the days when “flying was glamorous” and “people dressed up for flights.”

But elsewhere? Flying on low cost carrier is very common.

In Peru, people use low-cost flying to access highland cities like Cusco and Cajamarca, since a trip by land would take too long and would be perilous.

Meanwhile, in archipelagos like the Philippines, low-cost carriers connect its main islands, eliminating the need for multi-day journeys by ship.

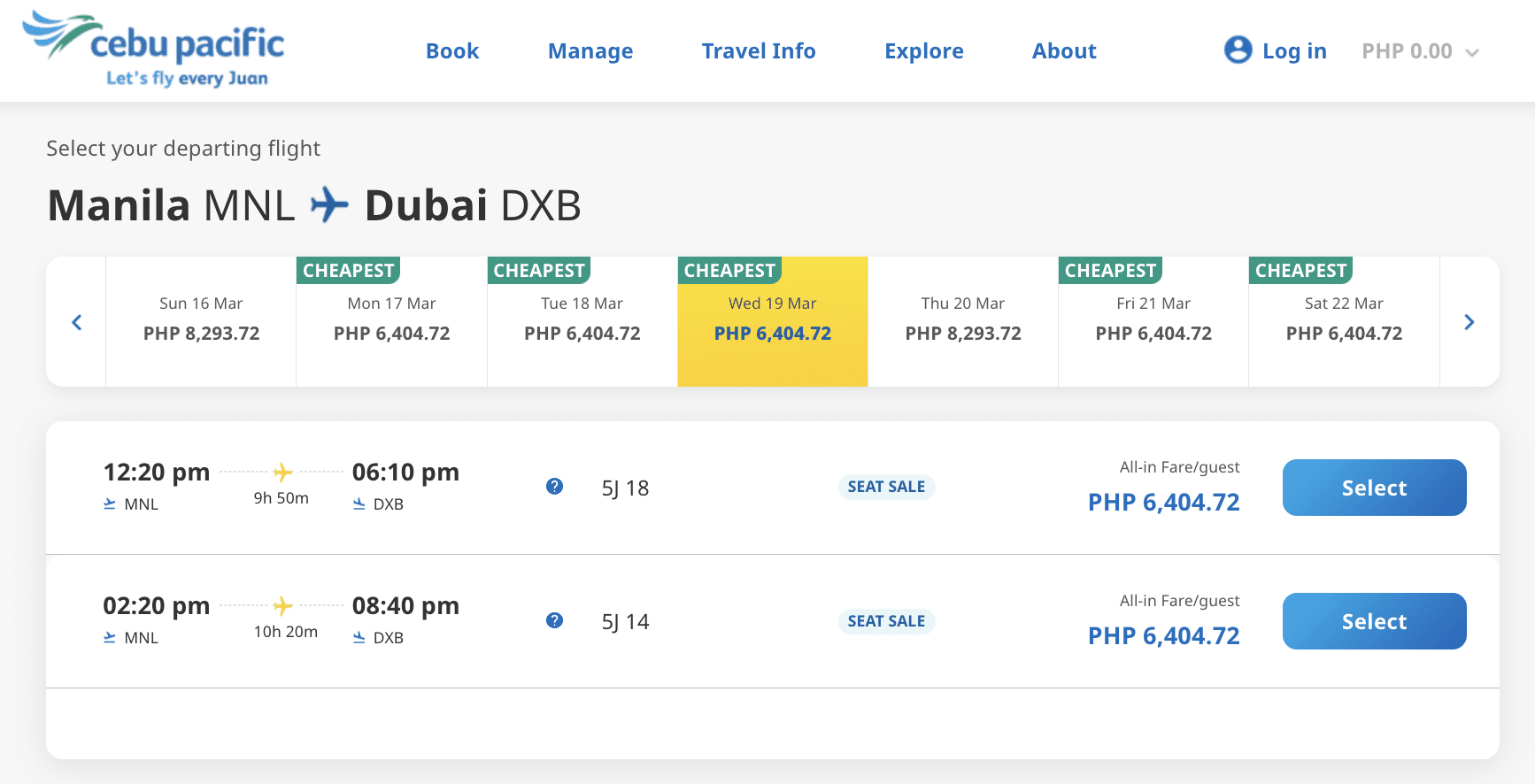

Plus, in the the same country, a low-cost carrier, Cebu Pacific, actually flies long-haul from Manila to Sydney (almost nine hours) and Dubai (almost 10 hours) – and you can fly these routes for less than $200 (all figures in CAD) per way. But no, you won’t get meals or even drinks during these long flights unless you purchase them in addition to your fare.

The people that regularly rely on these low-cost carriers have long ago accepted the realities of low-cost flying – that it’s essentially like taking a bus, but you get there faster.

Travellers who use low-cost carriers quickly learn that food and drinks cost extra and their bag must be the right weight and size. Additional amenities and comfort would certainly make the fares cost more, and many price-sensitive consumers are unwilling or unable to pay anything above the absolute lowest available price.

We in Canada are still relatively far from embracing low-cost flying, but we’re getting there thanks to Flair Airlines surviving despite the odds, and WestJet rising to Flair’s pricing challenge and introducing their own low-cost UltraBasic fares.

Comparing WestJet's UltraBasic vs. Flair's Ultra-Low Fares

Read moreStill, despite our reluctance to embrace low-cost airline travel with open arms, we actually have credit cards at our disposal that can help us adapt to the realities of low-cost travel, whether in Canada or abroad, as we’ll discuss below.

Choose a Credit Card with Lounge Access

When you’ve paid $10 for a fare on AirAsia, it feels unconscionable to pay an additional $10 for a meal and a drink during the flight.

Fortunately, a few Canadian credit cards offer complimentary airport lounge access, which gives you a place to have a meal or snack and take a bottle of water for your flight. You’ll also have a more pleasant waiting environment that surely beats waiting at the departure gate.

Most Canadian credit cards that offer lounge access provide free membership and passes through lounge networks like Priority Pass and Visa Airport Companion Program, which are mostly airline-agnostic.

Canada's Best Credit Cards for Lounge Access

Read moreThat means that even if you’re flying a low-cost flight out of Bogotá (BOG) on an airline such as Wingo or Spirit Airlines, you can still use the LATAM Lounge, one of the best lounges in the region, since it’s part of the Priority Pass network.

And if you’re flying out of New York (JFK) on Flair Airlines, you can pop into the Air France Lounge in Terminal 1 and take a sip of Champagne before your flight using the lounge passes available on your credit card.

In terms of which credit card you should choose to enjoy complimentary airport lounge access, the best card for this purpose is clearly the American Express Platinum Card which offers unlimited lounge access at airports worldwide as its flagship perk. However, if you’re only travelling a few times a year, you might find its $799 annual fee difficult to rationalize.

Conveniently, there are a few other cheaper alternative credit cards to choose from, but understandably, their free lounge access is more limited.

First, there’s the Scotiabank Passport® Visa Infinite* Card, which grants six lounge passes per membership year through Visa Airport Companion Program, and its annual fee is only $150.

This card is a great travel companion, since first and foremost, it doesn’t tack foreign transaction fees on purchases made abroad. This feature alone saves you 2.5% on all foreign currency purchases, a fee which most other Canadian cards charge.

Moreover, the card earns up to 3 Scene+ points per dollar spent, which you can use to offset any travel purchase at a rate of 1 cent per point.

First-year value

$850

Annual fee: $150

• Earn 40,000 points upon spending $2,000 in the first 3 months

• Earn 10,000 points upon spending $10,000 in the first 6 months

• Earn 10,000 points upon spending $40,000 in the first 12 months

Earning rates

Key perks

- No foreign transaction fees

- 6 Visa Airport Companion lounge visits per year

- Avis Preferred Plus (1 car-class upgrade)

Annual fee: $150

• Earn 40,000 points upon spending $2,000 in the first 3 months

• Earn 10,000 points upon spending $10,000 in the first 6 months

• Earn 10,000 points upon spending $40,000 in the first 12 months

Earning rates

Key perks

- No foreign transaction fees

- 6 Visa Airport Companion lounge visits per year

- Avis Preferred Plus (1 car-class upgrade)

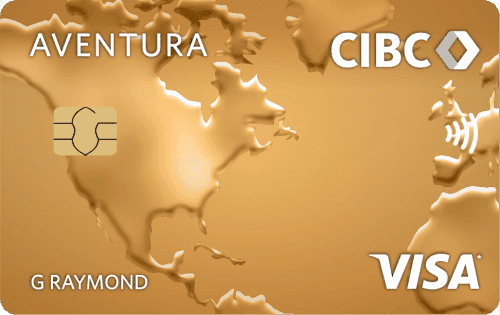

Next up is the CIBC Aventura® Gold Visa* Card, which comes with four free lounge passes per membership year through DragonPass.

In terms of other features, this card isn’t a heavyweight; however, with a low annual household income requirement of $15,000 and a modest $139 annual fee, it’s arguably the easiest to obtain among cards with free lounge access.

Plus, the CIBC Aventura Points that the card earns can be used for flights through the CIBC Aventura Airline Rewards Chart, or simply redeemed to offset just about any travel purchase through the “Shop with Points” feature at 1 cent per point.

50,000+ travellers get this email

Weekly deals, credit card insights, and points strategies – free forever.

First-year value

$480

Annual fee: $139First Year Rebate

• Earn 15,000 points on first purchase

• Earn 30,000 points upon spending $3,000 in the first 4 months

Earning rates

Key perks

- 4 Visa Airport Companion lounge visits per year

- NEXUS application fee rebate every 4 years

- Mobile device insurance

Annual fee: $139First Year Rebate

• Earn 15,000 points on first purchase

• Earn 30,000 points upon spending $3,000 in the first 4 months

Earning rates

Key perks

- 4 Visa Airport Companion lounge visits per year

- NEXUS application fee rebate every 4 years

- Mobile device insurance

Choose a Credit Card with Good Travel Insurance

In more ways than one, travel insurance is a must when flying with low-cost carriers, whether you have it as a standalone policy or as part of your credit card perks.

While flying can be unreliable at times regardless of airline, flying with low-cost carriers has risks that are somehow unique to it.

First, there’s the way in which low-cost carriers handle cancellations.

Since many low-cost carriers fly to destinations only once a day or a few times a week, when cancellations occur, the airline is constrained when it comes to rebooking passengers onto their own flights, which can leave travellers stranded for days.

Additionally, most low-cost carriers operate on a “point-to-point” model, which means that they don’t offer connecting flights.

While you can always separately book two flights that connect with the same airline, this opens you up to an additional potential issue. If a delay or cancellation occurs on one of your flights, there’s a chance the low-cost carrier won’t rebook you for free – otherwise known as “reprotection” – since they’re separate tickets and the airline is technically not required to rebook in this circumstance.

Thus, in cases such as these, you’ll have to rely on your trip interruption insurance to help you get you to your destination as quickly and efficiently as possible.

With trip interruption coverage, in the situations we’ve outlined above, you may be able to book the next cost-effective economy flight on any available airline and then claim the fare as expenses through the insurance coverage.

In these cases, by having solid trip interruption coverage, you could save yourself waiting for days to be rebooked by the low-cost carrier or possibly not being rebooked at all in situations where the carrier isn’t required to assist you.

Meanwhile, when it comes to flight delays, low-cost carriers also tend to cut costs on their provisions to passengers.

In many jurisdictions, when your flight is delayed for reasons within the airline’s control, the airline is required to provide meals or refreshments in a reasonable quantity.

In these instances, low-cost carriers may just hand out cookies and juice packs. WestJet, for example, typically only provides a $15 voucher to delayed passengers – an amount that will barely buy a meal at the airport, where prices are inflated.

When the delay isn’t attributable to the airline (e.g., weather disruptions), low-cost carriers usually wouldn’t even bother to provide anything at all.

In such cases, your credit card’s trip delay insurance could buy you a nice meal or even provide a hotel if your delay involves waiting overnight. With some credit cards, the coverage gives you up to $1,000 per person in these situations.

These are just some of the travel insurance benefits your credit card could provide for you, but to ascertain your coverage, be sure to read your credit card’s welcome kit and/or certificate of insurance.

Be it travel-focused cards or cash back cards, travel insurance coverage is among the selling points of many credit cards. However, since the amount and extent of coverage varies, it’s worthwhile for you to consider what coverage you’d like to have and how a card would cover for your trip in case of unexpected events.

To give you an idea of what’s available, below are a couple of cards noted for their strong insurance coverage.

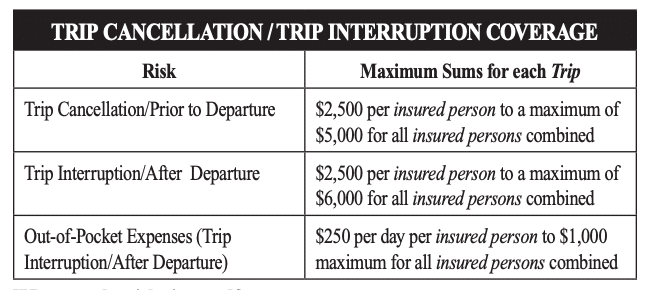

The first one is the TD First Class Travel® Visa Infinite* Card, which provides the following travel insurance benefits per covered person†:

- Travel medical insurance: up to $2 million†

- Trip cancellation: up to $1,500†

- Trip interruption: up to $5,000†

- Common carrier travel insurance: up to $500,000†

- Delayed and lost baggage: up to $1,000†

- Flight/trip delay: up to $500†

In addition to extensive travel insurance benefits, the TD First Class Travel® Visa Infinite* Card earns TD Rewards points that can be redeemed for travel products (e.g., flights, hotels, activities, etc.) through Expedia for TD at 0.5 cents per point, or they can be redeemed to offset any travel purchase made to your account at 0.4 cents per point.

First-year value

$900

Annual fee: $139First Year Rebate

• Earn 20,000 points on first purchase

• Earn 145,000 points upon spending $7,500 in the first 6 months

Earning rates

Key perks

- 4 Visa Airport Companion lounge visits per year

- $100 annual Expedia for TD travel credit

- Annual birthday bonus up to 10,000 TD Rewards points

Annual fee: $139First Year Rebate

• Earn 20,000 points on first purchase

• Earn 145,000 points upon spending $7,500 in the first 6 months

Earning rates

Key perks

- 4 Visa Airport Companion lounge visits per year

- $100 annual Expedia for TD travel credit

- Annual birthday bonus up to 10,000 TD Rewards points

Another card worth considering is the National Bank® World Elite® Mastercard®, which lists the following insurance benefits (per covered person)†:

- Travel medical insurance: up to $5 million†

- Trip cancellation: up to $2,500†

- Trip interruption: up to $5,000†

- Delayed baggage: up to $500 (for delays over six hours)†

- Lost or stolen baggage: up to $1,000†

- Departing flight delay: up to $500 (for delays over four hours)†

This card has always been at the top of our choices for insurance coverage since its travel medical insurance lasts up to 60 days for those 54 and under and 31 days for those aged 55 to 64.† Even seniors aged 65 to 75 receive up to 15 days of coverage,† which is a rarity for credit card insurance.

Additionally, the À la Carte Rewards points the card earns can either be redeemed for travel products through the program’s in-house online booking website at 1 cent per point or used to offset any travel expense at a lower rate of 0.83 cent per point.

Annual fee: $150

Earning rates

Key perks

- Airport lounge access

Annual fee: $150

Earning rates

Key perks

- Airport lounge access

Choose a Card with Points to Cover Low-Cost Flights

Most low-cost carriers don’t participate in loyalty programs since these programs would cost them money to operate.

There are only a few exceptions, such as Scoot, which is under Singapore Airlines KrisFlyer loyalty program, and JetSMART, which participates in the American Airlines AAdvantage program.

However, for most low-cost airlines, you can’t redeem miles or points through an in-house loyalty program.

That said, if you wish to save money and use points to book on a low-cost carrier, you can consider a credit card that yields fixed-value rewards. With flexible fixed-value rewards points, you can offset any travel purchase, which of course includes low-cost flights.

A good example of a card worth considering is the Scotiabank Gold American Express® Card, which earns up to 6 Scene+ points per dollar spent.

As mentioned above with the Scotiabank Passport® Visa Infinite* Card, Scene+ points can be used to offset any travel purchase at a rate of 1 cent per point; thus, earning 6 Scene+ points per dollar means up to a 6% return on your purchases.

Additionally, the Scotiabank Gold American Express® Card doesn’t tack on foreign transaction fees to purchases made in foreign currencies, such as low-cost flight tickets bought from Ryanair and paid for in euros.

First-year value

$525

Annual fee: $120First Year Free

• Earn 25,000 points upon spending $2,000 in the first 3 months

• Earn 20,000 points upon spending $7,500 in the first 12 months

Earning rates

Key perks

- No foreign transaction fees

- Amex Offers & Front of the Line access

Annual fee: $120First Year Free

• Earn 25,000 points upon spending $2,000 in the first 3 months

• Earn 20,000 points upon spending $7,500 in the first 12 months

Earning rates

Key perks

- No foreign transaction fees

- Amex Offers & Front of the Line access

Lastly, the RBC® Avion Visa Infinite† notably earns up to 1.25 Avion points per dollar spent on travel purchases.

When it comes to RBC Avion points, our usual advice is to transfer the points that the card earns to airline loyalty partners, including The British Airways Club, to gain access to outsized value, but your Avion points can also very well be used to offset travel purchases at a rate of 1 cent per point.

This redemption rate is in line with other programs, including Scene+ and CIBC Aventura, so it’s still a decent way to use Avion points.

First-year value

$1,080

Annual fee: $120

• Earn 35,000 points on approval

• Earn 20,000 points upon spending $5,000 in the first 6 months

Earning rates

Key perks

- Transfer to British Airways Avios, Cathay Asia Miles, WestJet, American Airlines

- DoorDash DashPass for 12 months

- Petro-Canada 3c/L savings + 20% bonus Petro-Points

Annual fee: $120

• Earn 35,000 points on approval

• Earn 20,000 points upon spending $5,000 in the first 6 months

Earning rates

Key perks

- Transfer to British Airways Avios, Cathay Asia Miles, WestJet, American Airlines

- DoorDash DashPass for 12 months

- Petro-Canada 3c/L savings + 20% bonus Petro-Points

Conclusion

With low-cost flights, there are realities we must accept, but fortunately, there are credit cards that allow us to adapt to these realities.

First off, practically nothing is included with low-cost flights, but with credit cards that come with free lounge access, you can save money on food and drinks.

Second, there are somewhat unique risks associated with flying low-cost carriers, especially with regards to delays and cancellations, and to mitigate these risks, you can charge your fare to a credit card with excellent travel insurance.

Lastly, low-cost carriers rarely participate in a loyalty program, so if you want to save money by using points, you can consider a card with flexible rewards that you can then use to offset your airfare.

In all, if you leverage the right credit cards, low-cost carriers become a great deal more appealing and not nearly as bad as some people make them out to be.

† Terms and conditions apply. Please refer to the card issuer’s website for up-to-date information. Reasonable efforts are made to maintain accuracy of information.

Jason thrives on connecting with the heart of a destination, seeking out experiences that go beyond the guidebooks.

First-year value

$480

Annual fee: $139First Year Rebate

• Earn 15,000 points on first purchase

• Earn 30,000 points upon spending $3,000 in the first 4 months

Earning rates

Key perks

- 4 Visa Airport Companion lounge visits per year

- NEXUS application fee rebate every 4 years

- Mobile device insurance

Annual fee: $139First Year Rebate

• Earn 15,000 points on first purchase

• Earn 30,000 points upon spending $3,000 in the first 4 months

Earning rates

Key perks

- 4 Visa Airport Companion lounge visits per year

- NEXUS application fee rebate every 4 years

- Mobile device insurance