The Best Ways to Convert Canadian Dollars into US Dollars

It’s awesome to be Canadian. We are a country that gets to enjoy skiing, maple syrup, politeness, and excellent credit card rewards programs.

In fact, I’d argue that the Canadian Miles & Points scene is one of the best in the world, especially given how easy it can be for us to sign up for our American cousins’ cards.

This brings up another quandary, though: how can we best pay off our USD-denominated cards in their native currency, and perhaps optimize our USD spending money for any trips to the US while we’re at it?

Today, let’s take a look at five methods to get American dollars at a great exchange rate.

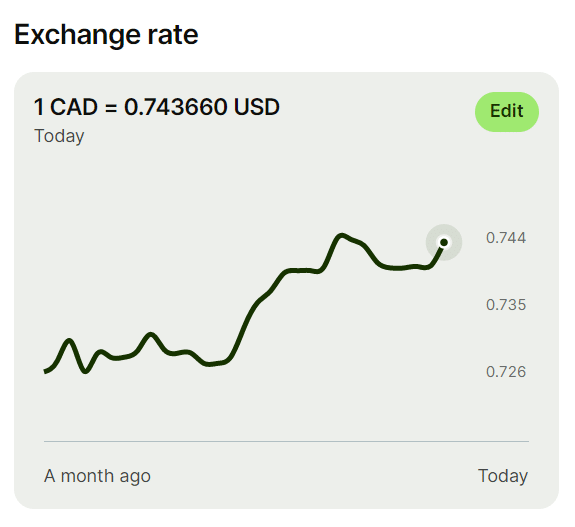

Wise

I’ve written about Wise before because their prepaid Visa card has been a great addition to the Canadian foreign exchange retail space. However, it’s not the prepaid Visa I’m super interested in today; it’s Wise’s international transfer services.

Wise openly publishes its exchange rates, which are some of the most competitive on the market, as well as an historical log of the Canadian dollar’s performance versus its American counterpart. This makes it one of the easiest ways to see what a good USD exchange rate ought to look like.

When you’ve made up your mind that it’s time to transfer, simply log in to the app or online. You can add your USD bank account down south as a recipient, and send cash to it easily and directly.

Just select how much money you wish to transfer, either directly from your bank or from funds which you’ve loaded onto your Wise Prepaid Visa.

Be aware that as per the chart above, you’ll be subjected to certain fees on Wise’s end.

Those fees are how they make their money, and the cheapest option will always be transferring from your bank account through Interac or direct debit versus using a Visa debit or – heaven forbid – credit card for the transaction. And because Wise codes as cash advance on all major issuers, it’s never recommended you use a credit card.

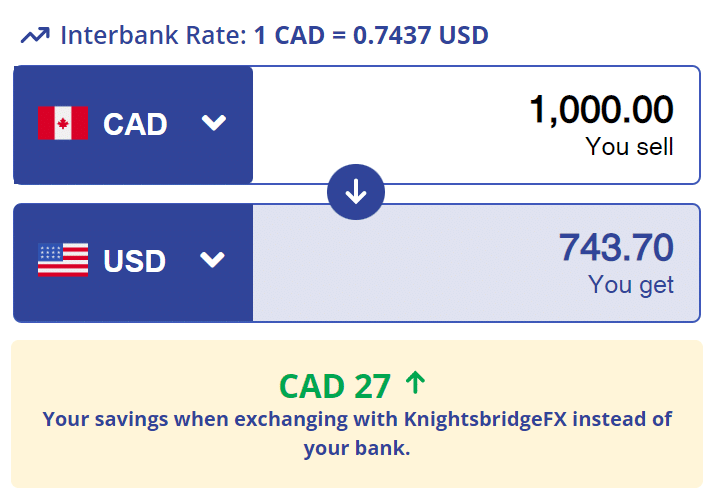

Still, at $1,000 (CAD) for $738 (USD), Wise is perhaps the most competitive USD exchange rates that’s widely available in the Canadian market.

Once you’ve hit send on your transfer, you’re all done. Wait a few business days for the funds to show up in your American cash account, but be advised that historically Wise has been slower for me than other forms of online transfer.

What you sacrifice in expedience, though, you certainly make up for with a good deal.

KnightsbridgeFX

The next method might stink a bit of the stone age due to the fact that it will require you to (gasp!) pick up the phone and call a trader.

But I can promise you that the person on the other end isn’t trying to sell you penny stocks from within a sweltering boiler room – they’re just trying to help you offload your CAD for foreign currencies.

The company I’m referring to which uses these ancient-seeming practices is KnightsbridgeFX, who can be reached via their call centre at 1 (877) 355 5239. Before thinking about completing a trade, let’s take a look at their stated exchange rate for our example value of $1,000 (CAD).

At a net of $744 (USD) for $1,000 (CAD), perhaps the inconvenience of calling is not a bad idea. Just remember that KnightsbridgeFX does not post its rates for every currency it trades in online, and those rates you do see in promotional materials can be subject to change. The only sure way to get a set quote is by calling in.

This being said, opening a KnightsbridgeFX account does require some effort. As a federally-regulated financial institution, you’ll have to pass fairly thorough Know Your Customer (KYC) verification before being granted an account capable of trading.

This will require you to upload your driver’s license or passport in order to open your account, as well as verify your source of funds. Every single new customer is scrutinized by real human beings to protect against fiscal impropriety.

When your account has been opened, you’ll be given a number and permitted to begin purchasing USD. Have your American banking information ready, as they’ll need it to complete those transfers down south.

Norbert’s Gambit

Do you like stocks that take rocket emojis to the moon? Well, that means you’ve probably heard of trading accounts.

Any Canadian citizen or permanent resident with an established credit history should be able to open a personal trading account. Several types of accounts, such as cash accounts whose profits are taxable, or Tax-Free Savings Accounts to make those stock-pick chicken tendies you always craved, are available.

As always, opening such an account is a very personal decision. This article is not meant to be financial advice, but it is posted here for informational purposes. Consult an accountant prior to opening or contributing to a trading account should you have any doubts about its effects on your personal financial situation.

That being said, if you have a trading account, then it is possible to engage in a classic Canadian trick: Norbert’s Gambit. This trick is named after its inventor, Norbert Schenkler, who discovered it in the early days of online stock picking.

Let’s use Questrade, for example. There may be other platforms you can use for this transaction, but this is the one that’s most famous for making the procedure simple.

- First, deposit some Canadian dollars into your account.

- Once the funds have cleared, go and purchase the exchange-traded fund (ETF) DLR.TO. Divide the number of Canadian dollars you wish to convert by the price of the ETF, which is sold in CAD, and ensure you purchase in a whole number (this is so you avoid any nasty fees incurred by buying fractional shares).

- Once you’ve purchased the DLR.TO, go to Questrade’s customer service chat.

- After passing customer verification with the chat agent, request that they journal your shares as DLR.U.TO. This is the same ETF as the previous one, except denominated in USD instead of CAD.

- Then just wait about 2–5 business days, and you’ll see the new shares in your account.

- Sell the shares, and voilà, you’ve turned your CAD to USD.

You could also choose to call or email Questrade to complete this process, but I find these to be too slow for my impatient taste. However you choose to complete the procedure, add your USD bank account to your Questrade and withdraw funds whenever ready.

Due to the time involved in this process, my preference for doing it would only be when transferring large sums of money across the border.

Your Bank’s USD Exchange Account

Sometimes, simplicity is the spice of life. Before we even get into the nitty-gritty of using your bank’s in-house exchange system, I want to warn you: this will not be as good a value as the other methods I’ve mentioned.

However, there won’t be Norbert Gambit’s complexity, KnightsbridgeFX’s phone conversations, or Wise’s at-times tedious delays. Everything will be quite simple, and what you sacrifice in cash value, you’ll get back in rapidity.

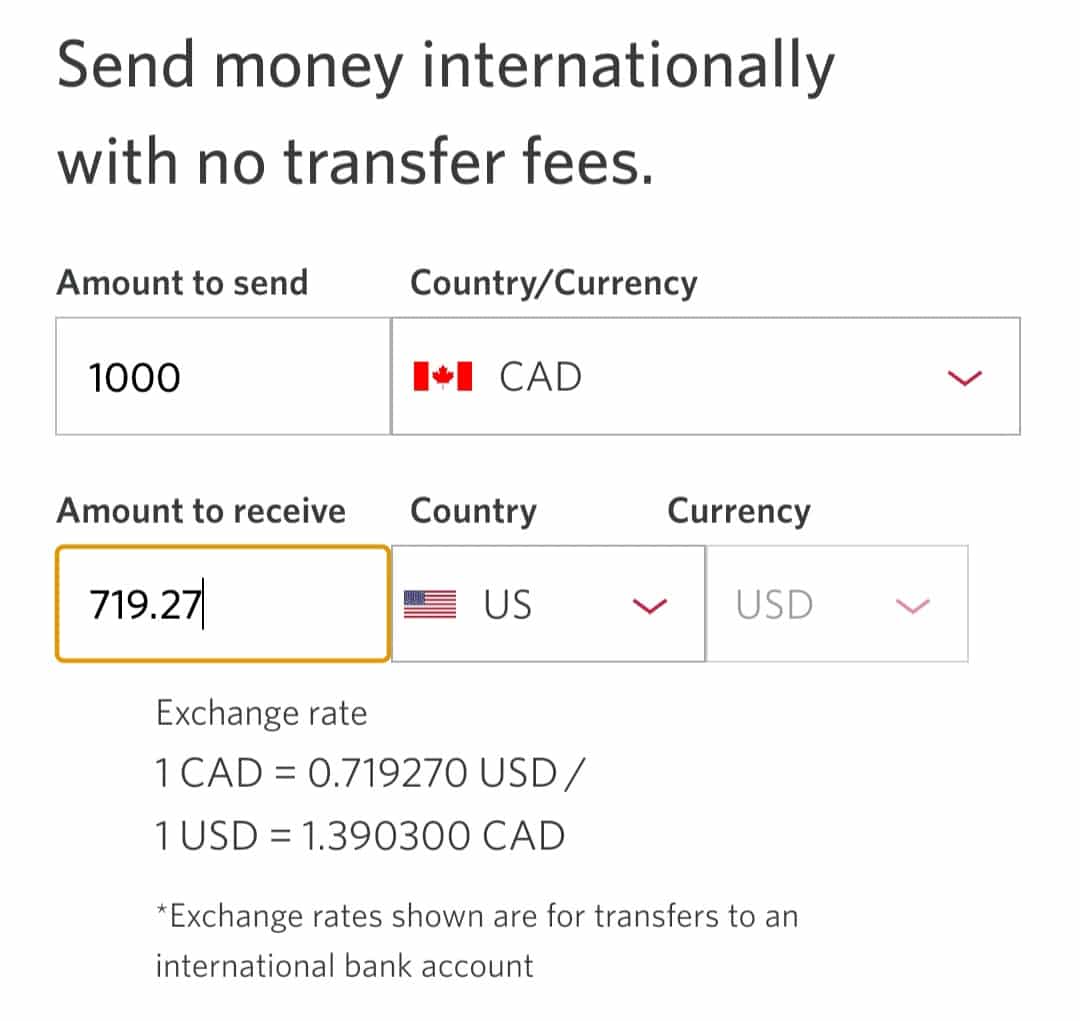

Let’s take a look at Simplii Financial’s Global Money Transfer program (which is identical in rates and speed to those of Simplii’s parent company, CIBC).

You’re getting $719 (USD) for $1,000 (CAD). Ouch. That’s $25 (USD) less than KnightsbridgeFX and $19 (USD) under Wise’s quote.

The good news is that the USD will be credited fast – my money transfers have shown up in my US bank account within 1–2 business days. In the past, I’ve also transferred from my Canadian BMO account to my US BMO Harris chequing account, and the transactions would post within hours!

While not the best option, this is often the fastest and involves the lowest amount of interaction. If you bank with CIBC or Simplii Financial, you can also take advantage of the fact that they occasionally run promos for $50-75 (USD) cash back for making a global money transfer over $100 (USD). Not too shabby.

Withdraw from an ATM

Within the Miles & Points community, it can often be verboten to even mention the dread name of that forbidden green substance…

I’m referring to cash, which is no fun when combusted. Sometimes, a traveller will need it. In such situations, it can be tempting to go and exchange currency or attempt to find some other way to get American dollars.

However, one of the best methods available to you if you have a Canadian debit card on you is to simply withdraw money from an ATM.

While you may be dinged a foreign ATM fee by your bank, and possibly another by the machine itself, you’ll get a spot exchange rate that isn’t designed to fleece you (assuming, of course, that you’re using a device from a reputable financial institution, and not a 7-Eleven in the bad part of town).

While this isn’t an ideal situation, it’s a much better idea than purchasing USD on a credit card or exchanging your CAD at a booth when you’re abroad.

In fact, there are some banks that positively encourage it. As members of the Global ATM Alliance, Scotiabank and its free junior partner Tangerine have a reciprocal no-fee agreement with Bank of America, the largest consumer bank in the United States.

How about the exchange rates?

Below, you can see the current spot rate for transferring CAD to USD within Tangerine’s USD Savings Account. This rate works out to $732 (USD) for $1,000 (CAD).

You can also withdraw directly with your CAD-denominated Scotiabank or Tangerine account and receive the spot rate minus a 2.5% standard foreign exchange fee automatically deducted.

For example, the day’s spot rate (that you can look up on Google) is $745 (USD) for $1,000 (CAD). With the 2.5% foreign exchange fee automatically deducted, you’re looking at getting around $726 (USD) for $1,000 (CAD).

But if you’d rather not open an account with Scotiabank, Tangerine, or one of the major banks, you always can get yourself a no-fee card with one of the non-mainstream players. Among those offering them are EQ Bank and Wealthsimple.

Their respective cards don’t charge any fees from their end — not even the pesky 2.5% foreign exchange fee. However, you’d still be dinged by the ATM you’re withdrawing from, and in the US, fees are around $2-4 (USD) per withdrawal.

Using the $745 (USD) for $1,000 (CAD) spot rate above, you can get $742 (USD) for $1,000 (CAD), assuming that the ATM charges you a $3 (USD) fee for the withdrawal.

But be sure to decline any conversion the may ATM offer. This racket is called dynamic currency conversion (DCC), and you’d surely be getting a bad marked-up rate.

If stuck in Philadelphia attempting to buy a cheesesteak at a cash-only joint, I know which card I’d reach for at the bank.

Conclusion

In a marketplace with this many options for converting your Canadian dollars to their southern counterparts, it can be a bit confusing to know where to begin.

I hope that today I’ve shed some light on the various methods available to us, whether it’s for paying off our US credit cards or simply gathering some spending money for our trips across the border.

Personally, I tend to use Norbert’s Gambit for large transactions, Wise for daily banking needs, and my banks’ exchange options for fast turnaround. I’m looking forward to using KnightsbridgeFX more in the future, as my account there is new.

Until next time, may your exchange rates be excellent.

Kirin explores the world through the lens of miles and points, sharing insights on premium travel experiences.

First-year value

$336

Monthly fee: $15.99

• Earn 1,250 points per month upon spending $750 per month for 12 months

Member Discussion