What’s My Travel Spending Strategy?

After I shared with you last week the details of my trip to Turkey, Greece, and the Middle East, reader Andrew left the following comment:

Sounds like a really interesting trip. I would be interested to know how much foreign currency you would budget on trips like these. Also what you would use as an alternative to withdraw currency if needed. From my past experiences, I have started to carry less and less currency as it is becoming a norm for many countries to accept credit and the foreign transaction fee is not really a deterrent for not using my credit card. I’m sure you would only use it in emergency cases anyway.

This is something that many other readers have asked me as well in the past: what payment methods and financial products do I use to ensure I’m spending money effectively (i.e., minimizing my costs and maximizing my returns wherever possible) when I’m travelling abroad? In this post, I thought it’d be worthwhile to talk about my travel spending strategy and give you a picture of how I approach the “money situation” along my trips.

In This Post

- Credit Cards vs. Cash

- No FX Fee Credit Cards

- The Stack Prepaid MasterCard

- A Handful of USD Cash

- Conclusion

Credit Cards vs. Cash

As with my regular purchases at home, I prefer to use my credit card rather than cash whenever possible when I travel, because I find that it just makes my life so much easier.

Instead of juggling a handful of foreign banknotes (not to mention the coins that you accumulate from small transactions, which tend to slip out of my wallet at the most inopportune times), I can simply swipe my credit card and go on my merry way, knowing that I can review the charge later if needed.

I know some people are concerned about the potential for fraudulent transactions on using their credit cards abroad, but I’ve flat-out never encountered such a situation over many years of travelling abroad.

(I’ve had numerous instances of credit card fraud that took place in Canada in which someone must have spoofed my credit card number. In those situations, the issuer was always very good about reversing the charges and issuing me a new card, and I know they’d do the same if I were a victim of a fraudulent transaction while travelling as well.)

Using a credit card also allows me to easily track my spending after-the-fact by logging into my online account and seeing where the money went – if I used cash, I’d have to either note down the expenses more meticulously in real-time, or risk losing track of my spending entirely. On an extended trip, I’ll typically log in to my credit card portal around once a week to review my spending patterns and ensure that no unexpected charges have appeared.

No FX Fee Credit Cards

There are, however, a few significant challenges associated with using credit cards along your travels. The first is the 2.5% foreign transaction fee that’s levied by most major Canadian credit card issuers.

Unlike Andrew, who felt that “the foreign transaction fee is not really a deterrent” for credit card usage, I personally feel very annoyed by the fact that the 2.5% FX fee seems to be a long-standing industry standard here in Canada, and I always go out of my way to avoid paying it whenever I can.

Fortunately, that industry standard seems to be softening these days, with the Scotia Passport and HSBC World Elite both offering 0% foreign transaction fees as a selling point. And starting August 1, the Scotia Gold Amex will begin offering this perk as well.

However, these premium credit cards do have annual fees that you must consider when deciding whether the card is worth getting (or in the case of a first-year annual fee waiver, whether or not to keep the card beyond the first year). If you’d prefer a no-fee credit card to use purely for foreign spending, then the Rogers World Elite MasterCard can be a solid bet, whose 4% cash back on foreign spending more than offsets the usual 2.5% FX fee.

In my case, I actually prefer to use my US credit cards – chiefly the Chase Sapphire Preferred – whenever I’m travelling abroad.

(Note that this makes sense for my situation as someone who has regular access to US dollars, so I can easily pay off my credit card bill without incurring any FX impact. If most of your holdings are in Canadian dollars, then this might not be as worthwhile a strategy to pursue.)

After I first began dabbling with US credit cards, over time I found that it just makes sense to use them while travelling. I like earning Chase Ultimate Rewards points more than Scotia Rewards or HSBC Rewards, since I can redeem Chase UR through their transfer partners at a higher value than the fixed-value Canadian points programs (even accounting for the difference in nominal value thanks to the CAD/USD spread).

Moreover, I generally find Chase to be so easy to deal with over the phone, which is something I’d value if I needed to call in about something while travelling, whereas Scotiabank and HSBC’s customer service hasn’t filled me with the same confidence (and as a client on the telco side, I don’t have much faith in Rogers doing so either). And lastly, I’m also hoping that having some regular spend activity on my US credit cards will foster a healthier relationship with the US credit issuers as well.

The Stack Prepaid MasterCard

Despite having a solid strategy in place for my foreign credit card spending, the other challenge with credit cards is of course that not all places around the world have an infrastructure in which credit card usage makes sense.

There are a huge amount of places where credit cards simply aren’t widely accepted. For example, when I visited Ghana and Micronesia on my recent round-the-world trip, I had no hope of swiping my credit card unless I was patronizing the fanciest establishments in town that catered almost exclusively to Westerners.

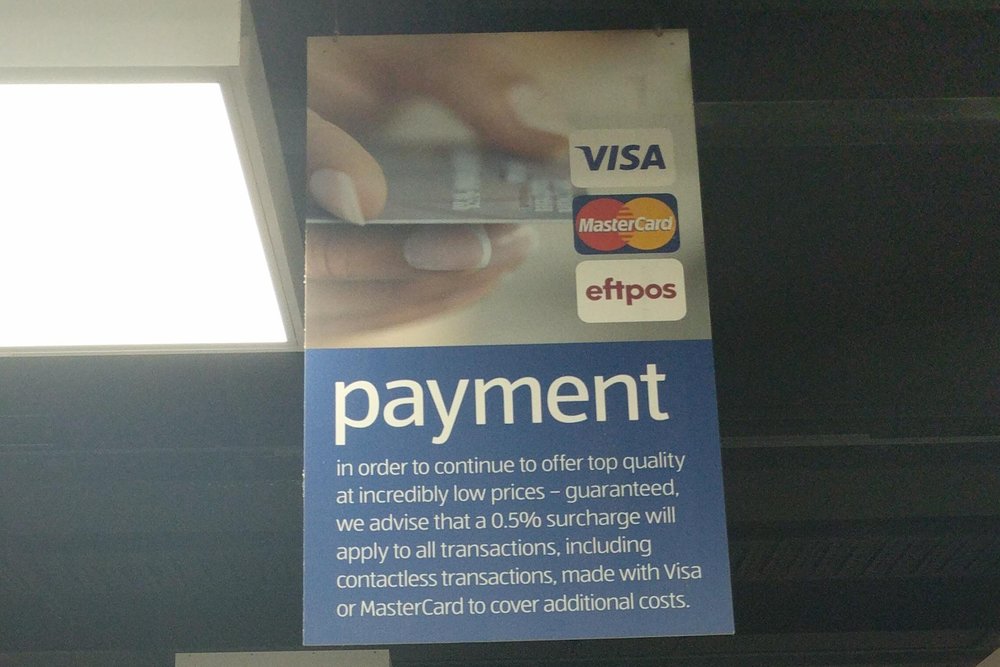

Then there are places like Australia and New Zealand, where, despite being highly developed countries, the credit card “culture” doesn’t seem like it has caught on like in Canada and the US. Whether you’re eating at a restaurant, picking up groceries, or paying for your hotel bill, credit card transactions are often subject to a nasty 0.5–2% surcharge.

This practice seems to be accepted by most Aussies and Kiwis as simply the way things are, which is pretty mind-boggling, and does in fact make me feel quite averse to using my credit cards.

So while I’d say that my credit cards help me navigate about 50% of my spending while on the road, the remaining 50% of transactions are settled with cold, hard cash. And in that regard, the Stack Prepaid MasterCard has been a godsend that has completely changed the way I handle foreign cash.

Before Stack, I’d have to find a way to estimate how much cash I’d need along the trip and withdraw that amount in USD beforehand, because otherwise I’d have to pay all sorts of ATM fees (charged by both the ATM and my bank), foreign exchange fees, and/or cash advance fees when withdrawing money abroad.

Yes, the amounts of those fees themselves wouldn’t have necessarily mattered so much, but similar to the 2.5% FX fees on major credit cards, they were something I was looking to avoid on principle.

The Stack Prepaid MasterCard is the first prepaid product that also offers a 0% foreign transaction fee and $0 ATM withdrawal fees. That means I’m able to withdraw however much cash I need as I go, and rarely need to waste unnecessary time hunting down a currency exchange when I arrive at a new place. The only fees I’ll pay are the ATM fees levied by the machine itself, which usually amount to no more than $2, if it’s being charged at all.

It’s amazingly easy to track my Stack balance using the app on my phone, and if the balance runs low, I can easily top-up using Visa Debit straight from my Canadian bank account. If, for some reason, the credit card I’m carrying doesn’t work, then the Stack card gives me a backup option to use for any point-of-sale transactions as well.

You can pick up a Stack Prepaid MasterCard through my referral link (works on mobile only) to earn a free $20 credit upon opening an account. The product has greatly improved my travel experience, and I couldn’t be happier with how effectively it addresses the foreign cash conundrum I previously faced.

Despite that, though, I still make sure never to depart on a trip without…

A Handful of USD Cash

I still think it’s prudent to keep some US dollars on me while I’m out and about, even if I do have regular access to cash via ATMs at a fair exchange rate.

As diligent and organized as you might be in keeping an eye on your money, you’ll inevitably run into situations in which you need some cash at a moment’s notice, but find yourself short. At that point, it can be impractical to embark on a hunt for ATMs, and you know how these things are… ATMs are everywhere when you’re just going about your day regularly, but when you truly need one, they’re nowhere to be found.

In these cases, having some US dollars on hand can make all the difference, since many places around the world are accustomed to accepting US dollars from travellers in addition to the local currency.

Examples of these situations might include paying for a tour just before it begins, visiting an attraction that accepts credit cards for one part of the ticket but not for another, or even coming face-to-face with an immigration official who insists you must pay a sneaky “departure tax” upon leaving the country.

Before the Stack Prepaid MasterCard came along, I used to carry much larger volumes of US dollars around so that I could change them for local currencies at the exchange, and I’ll admit that occasionally brought some anxiety knowing how much cash I was carrying on my person.

Fortunately, now that I’ve got Stack, I only bring along a small amount – about US$200 for my current month-long trip, for example – solely for emergency use. And as a Toronto resident holding a US dollar account with CIBC, picking up my greenbacks for a trip is as simple as hitting the CIBC ATMs immediately before embarking on my trip at Pearson Airport.

Conclusion

No matter here I go in the world, I feel very comfortable that I’m not paying any more than I need to for the privilege of transacting in foreign currencies as long as I’ve got three things in my wallet: a credit card with no foreign transaction fees (whether Canadian- or US-issued), my Stack Prepaid MasterCard for cash withdrawals, and a small amount of USD cash just in case.

Next week, I’ll write a follow-up post about the other major question when it comes to dealing with money on the road: how I manage my spending habits, budget for my out-of-pocket expenses, and ensure I’m spending within my means while still having an awesome trip.

First-year value

$336

Monthly fee: $15.99

• Earn 1,250 points per month upon spending $750 per month for 12 months

Earning rates

Key perks

- Transfer to airline and hotel partners

Monthly fee: $15.99

• Earn 1,250 points per month upon spending $750 per month for 12 months

Earning rates

Key perks

- Transfer to airline and hotel partners