When signing up for a new credit card, you’ll typically need to meet a minimum spending requirement within a specific time period to unlock some or all of the card’s welcome bonus. In some cases, the required spending is quite minimal; however, for larger welcome bonuses, the threshold often exceeds $10,000, and can even rise to $50,000 or more.

Credit card welcome bonuses are one of the fastest ways to accumulate points. Therefore, you’ll want to be sure that there aren’t any barriers to meeting the minimum spending requirement, as you’d otherwise lose out on a great opportunity.

Fortunately, there are some creative ways to meet minimum spending requirements, which can either buy you more time to complete the spending, or push you over the threshold before the spending window closes.

In This Post

- What Are Minimum Spending Requirements?

- Use Bill Payment Services

- Major Life Events

- Prepay Future Expenses

- Other Ways to Meet Minimum Spending Requirements

- Conclusion

What Are Minimum Spending Requirements?

Many credit cards with welcome bonuses come with some sort of minimum spending requirement. Usually, you’re required to charge a certain amount in purchases onto your credit card within three months or so to be eligible to receive the signup bonus; however, the spending window can also be drawn out over six months or longer.

The window to meet the minimum spending requirement begins on the date of your application’s approval. Therefore, in practice, you actually have less than the full allotment to fulfill the spending requirement, given that it takes time for your new card to arrive in the mail.

The amount of spending required to unlock the card’s welcome bonus varies widely between cards, and can also change as new offers are rolled out on individual cards.

For entry-level cards with low annual fees, the welcome bonus is usually quite modest, and might have a minimum spending requirement of up to $1,000 in the first few months. Sometimes, you’ll earn the bonus simply upon being approved or making your first purchase.

Mid-tier cards, which have an annual fee in the range of $120–200, have a higher minimum spending requirement that’s typically paired with a larger welcome bonus. You can usually expect a minimum spending requirement in the range of $1,000–3,000, although it sometimes goes higher for larger welcome bonuses.

Top-tier cards, which come with an annual fee of $400 or more, generally have the highest welcome bonuses, and the biggest minimum spending requirements to match. Expect to spend $5,000–10,000+ during the spending window to unlock a handsome amount of points for your efforts.

It’s also becoming more popular for credit card issuers to impose monthly minimum spending requirements over a longer period. For example, you might get a smaller welcome bonus for each month in which you spend $500 over the course of the first year as a cardholder, which amounts to a sizeable welcome bonus when it’s all tallied up.

Furthermore, we’re also seeing multiple tiers of spending requirements (and welcome bonuses), as well as some welcome bonuses tied to spending in the second year as a cardholder. If you have an offer like this, be sure to keep track of your spending to make sure you don’t miss out.

Once you’ve fulfilled a minimum spending requirement, the welcome bonus is typically deposited into your account once the charge that brought you over the threshold posts to your account. It’s always exciting to see your points balance increase, and it’s a satisfying feeling to not have to worry about how much spending is left.

For monthly welcome bonuses, the points are deposited into your account each month once you’ve met the monthly requirement. You’ll want to keep track of your monthly spending, since if you miss the threshold one month, you’ll lose out on the welcome bonus for that month.

Even if you’re fortunate enough such that these amounts are attainable with your normal spending patterns, there are many reasons why it’s useful to have some tricks up your sleeve to help meet higher minimum spending requirements.

Use Bill Payment Services

A fantastic method to help meet minimum spending requirements is to use bill payment services to pay for anything for which you can’t usually use a credit card. These services come with an additional processing fee, so you’ll want to make sure that the benefits outweigh the cost of acquisition.

Throughout the year, many individuals encounter large bills that can’t be paid directly with a credit card. Some examples include rent, taxes, tuition, large utility bills, property taxes, and more.

Since these expenditures tend to be quite large, paying with a credit card through a third-party service can go a long way towards fulfilling a minimum spending requirement.

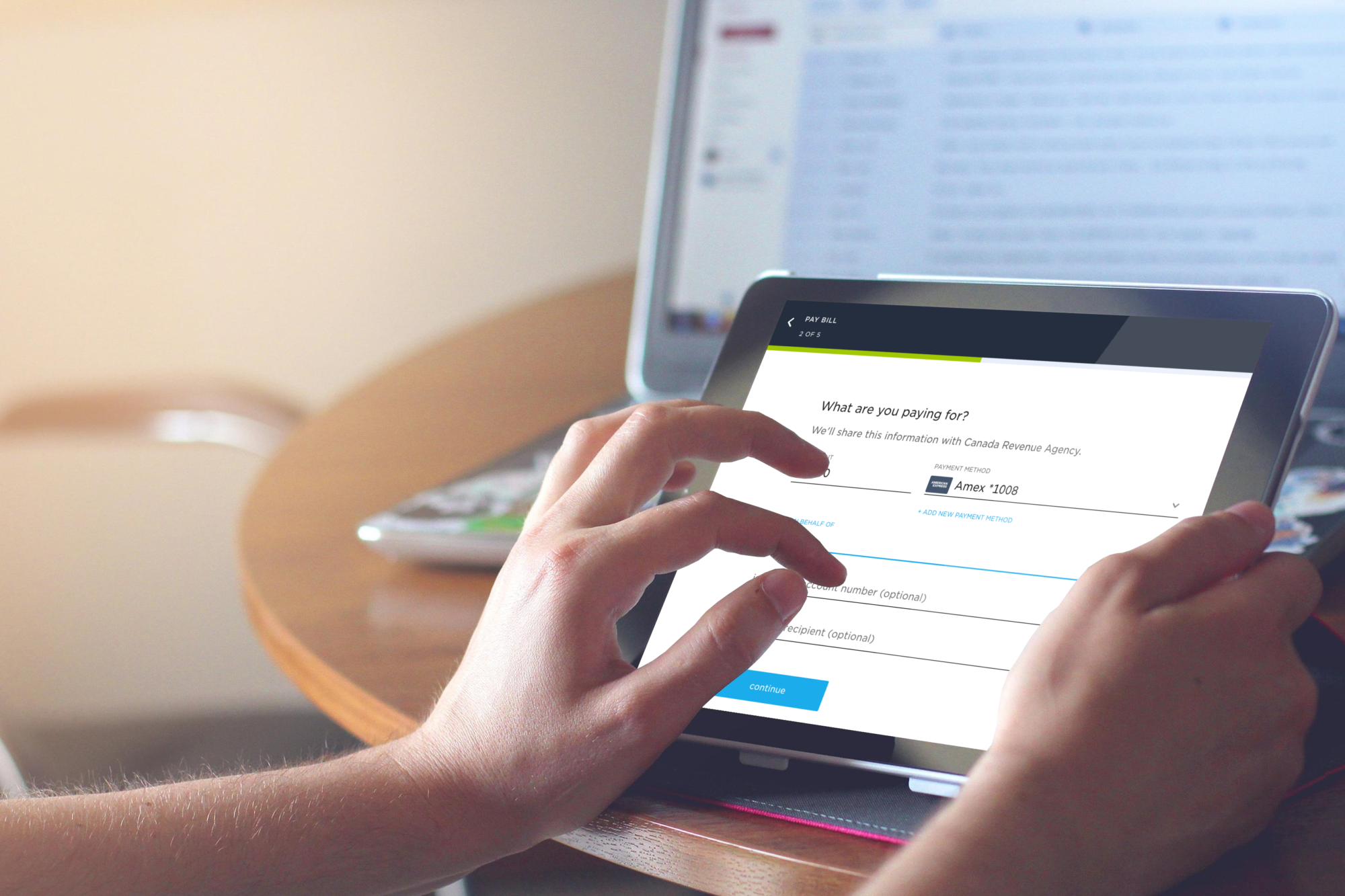

In Canada, our preferred platform is Chexy, which provides a way for you to pay rent, bills, and personal taxes with a Visa or American Express card and earn rewards on your monthly payments.

Chexy charges a modest 1.75% service fee, so you’ll want to factor that into your monthly budget. However, you can reduce that fee to as low as 0.5% by referring friends and family to the platform, too.

For example, if your rent is $2,000 each month, then Chexy’s 1.75% service fee would add $35 to the total. Over the first three months, you’d have made $6,000 of progress towards a minimum spending requirement, for a total additional cost of $105.

It’s quite likely that the welcome bonus, and in many cases, the points or cash back earned every month when you’re not fulfilling a minimum spending requirement, are worth the extra cost.

Chexy is our favourite Canadian platform for earning credit card rewards on rent, bill payments, and personal taxes.

Aside from rent, you can make use of Chexy to pay for other large expenses, including income tax, property tax, tuition, car lease payments, utility bills, and more, with a credit card.

The advantage of this method is that it’s quick and easy, and many of the expenses available through bill payment services are significant. On the other hand, it comes with a cost, so you’ll always want to make sure that it’s worth it. Otherwise, you’d be incurring extra costs for no reason.

Major Life Events

Many of life’s biggest events often come with a large amount of spending. If you’re planning a family vacation, a wedding, a honeymoon, a move, or a renovation on your home, these are all great opportunities to work towards a large minimum spending requirement.

To use the example of planning a wedding, you’ll have a number of significant expenses to cover, including a venue, food, beverages, attire, rings, accommodation, travel, and more.

Depending on the size of the wedding, these expenses can easily exceed $20,000, which is a great opportunity to earn points that you could, say, put towards a dream honeymoon.

As you go through the planning process, you’ll want to find out which payment methods are available. If you’re able to pay directly with a credit card, great! If not, consider looking at alternative options, such as bill payment services, to see if there’s still a way for you to put the spending towards a welcome bonus.

Since a wedding, renovation, or move can incur a significant amount of spending, you may also want to strategize with a significant other to work towards multiple welcome bonuses. This way, you’re utilizing the opportunity to unlock more points, while working in tandem with your partner to elevate your Miles & Points expertise.

Prepay Future Expenses

There are many ways to meet a minimum spending threshold within three months by effectively bringing forward your future spending, which would otherwise take place after the three-month window.

For example, if you normally spend $250 each month on gas, and you’re aiming to meet a $1,500 spend within three months, you could buy up six months’ worth of gas station gift cards at your preferred retailer.

This way, you’d be able to easily meet the spending requirement, and for the next six months, you’d use gift cards to pay for gas instead of your credit card.

Another option is to prepay any bill that can be paid with a credit card, including a cell phone, cable, utilities, or internet, for a few months in advance. When you go to pay your bill, you can slightly overpay using your credit card, which helps you meet the minimum spending requirement, and then you’ll just use up the credit in your account over the next few months.

Of course, one disadvantage of this method lies in the time value of money.

By prepaying future expenses, whether by buying gift cards or prepaying bills, you’re giving up the return you could’ve earned on that money in the intervening period. However, this return that you’re giving up is almost always outweighed by the welcome bonus you’d earn as a result of meeting the minimum spending requirement.

Other Ways to Meet Minimum Spending Requirements

If any of the above tips don’t apply to your particular situation, you can still apply other common methods to help meet minimum spending requirements.

Some credit cards offer bonus points for spending in specific categories. For example, the American Express Cobalt Card offers 5 American Express Membership Rewards points per dollar spent on groceries, restaurants, and bars.

While it’s usually best to earn as many points as you can with each dollar spent, you may want to temporarily shift some or all of your regular spending to a card on which you’re working towards a minimum spending requirement.

You’ll lose out on a few points this way, but the welcome bonus is sure to add up to more than what you’d have otherwise earned through category multipliers.

If you tend to go out for dinner or drinks with groups of people, you could also offer to pick up the tab for your group, thereby making more progress towards a minimum spending requirement. Of course, you’ll want to make sure everyone pays you their fair share.

Many employers offer benefits to employees to cover services such as dentists, massage therapy, prescription medication, and more. Instead of having the costs billed directly to your benefits company, you can consider paying for them directly with your credit card, and then filing a claim to be reimbursed separately.

For example, a simple trip to the dentist often comes with a cost of $200 or more. Rather than having your benefits cover the cost directly, consider charging the $200 (or more) to your credit card, and then send in a claim after the fact to help work towards a minimum spending requirement.

As part of your job, you may have to spend money on a company credit card for daily expenses. Some employers might allow you to make charges on your personal credit card instead, and then reimburse you for work-related expenses.

Especially if these expenses are significant, this can be a great way to spend someone else’s money and earn rewards.

Lastly, consider prepaying charitable donations as another way to work towards minimum spending requirements, rather than waiting until the end of the year or rolling them out on a monthly basis.

Conclusion

Credit card welcome bonuses are the fastest way to accumulate large amounts of points.

Welcome bonuses are often paired with a minimum spending requirement in a specified time period. As the size of the welcome bonus increases, so too does the minimum spending requirement, which can reach in excess of $10,000 and sometimes even more.

Fortunately, even large minimum spending requirements can be fulfilled by using some outside-the-box methods. If you’ve got your eyes on a juicy welcome bonus, be sure to use all methods at your disposal to make sure you don’t lose out on a nice boost of points.

I’ve paid my car and home insurance on my credit card. They don’t charge an additional fee, and together it comes pretty close to a mid-tier spend requirement.

Fantastic article. Thanks for sharing!

Making charitable donations is another quick way to top up your spend if you fall short at the end of the month.