Interchange Class Action: Small Businesses Can Claim Up to $600

Recently, the Canadian Federation of Independent Business (CFIB) took Visa and Mastercard to court.

It appears their legal team had Phoenix Wright: Ace Attorney onboard, because they managed to wring a substantial settlement from the credit card giants.

Today, let’s review what happened and how you can make a claim if, if applicable.

The Lawsuit

The case that was brought by the CFIB specifically called into question the legality of Visa and Mastercard forbidding merchants from charging customers additional fees for credit cards, especially premium credit cards that incurred high transaction fees.

These transaction fees, known more commonly as “interchange fees” or colloquially as “swipe fees”, were hitherto mandatory for merchants to accept.

Moreover, merchants could not opt to decline premium credit cards, such as the high-fee Visa Infinite Privilege or Mastercard World Elite lines of products, lest they draw the ire of the major payment networks.

This has now been ruled to have caused damages by the court system. Therefore, businesses who incurred interchange fees will now be entitled to compensation.

Moreover, come October 6, 2022, many of the policies previously enforced by Visa and Mastercard will be retired, and policies such as surcharging customers for credit card use will be permitted.

While I personally have opinions about this, it’s important to remember that the law has spoken and we as Canadian consumers will now be bound to the changes detailed within the settlement. What this also means is that anybody reading this who’s run a business in the past which accepted credit cards can be eligible to receive some of the compensation finalized in the CFIB’s lawsuit.

How to Make a Claim

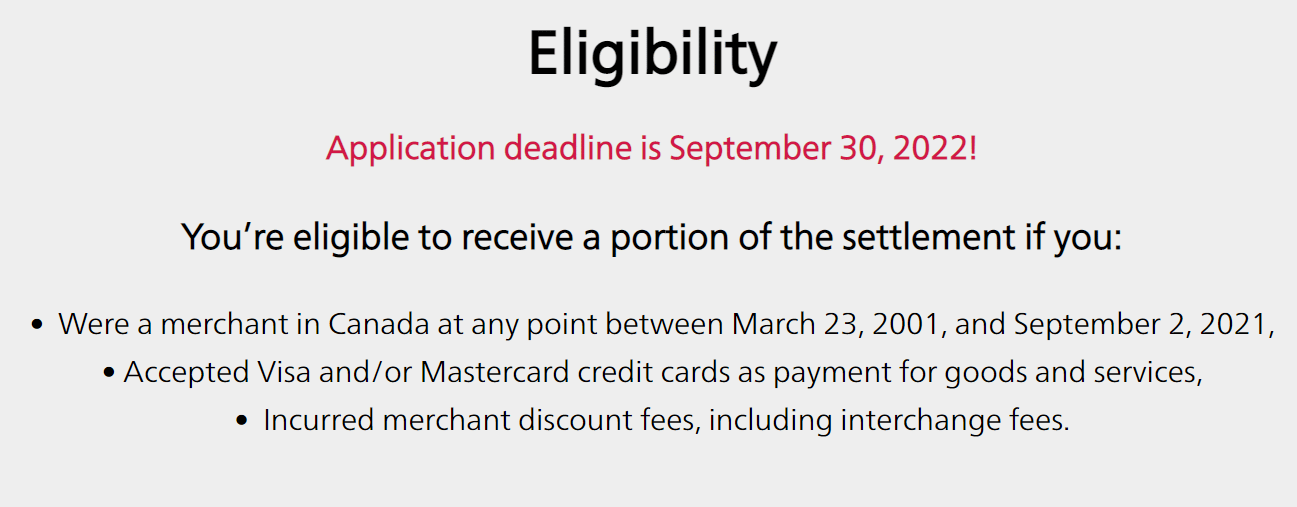

Before making a claim for any quantity of the money set aside by the settlement, consider your eligibility. You’re going to have to file all your paperwork by September 30, 2022. The rest of the information is given directly by the CFIB:

In order to determine what type of business you were running, consider that you must have been operating between March 23, 2001 and September 2, 2021 in order to qualify for compensation. If you ran your business entirely outside this timeline, you’re out of luck.

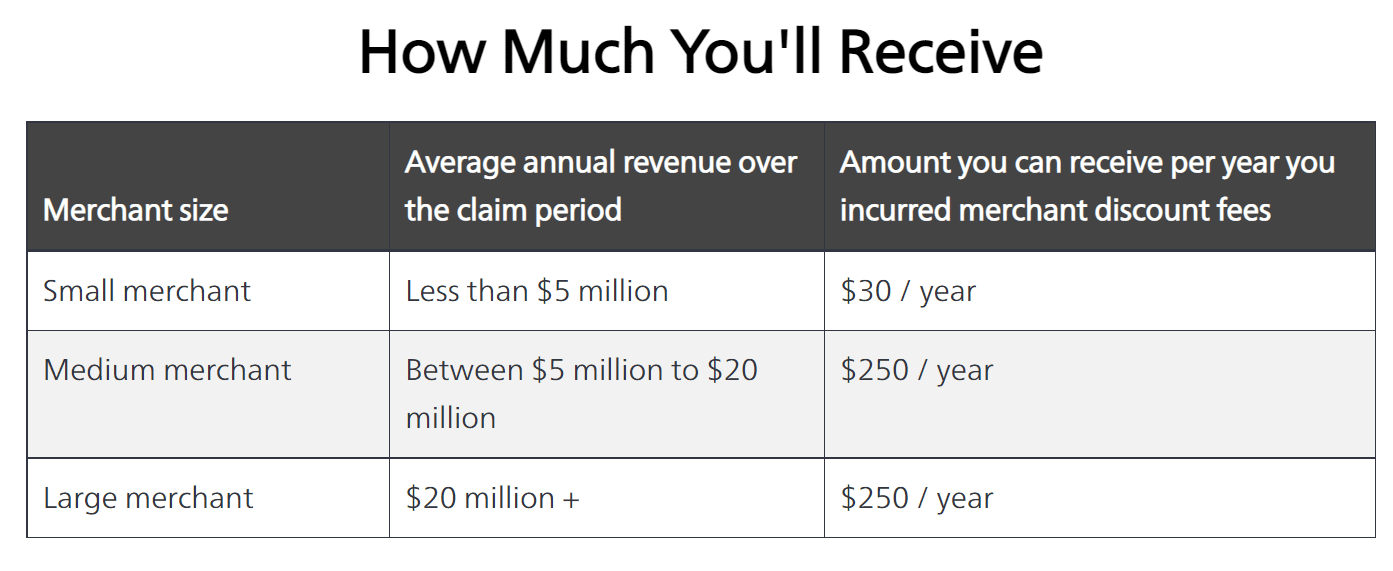

Next, consider the amount of revenue your business generated in order to determine what category you’ll fall under, and how much you could be entitled to receive.

If you’re running a business that operates on more than $5 million in revenue a year, then my heartfelt congratulations and also my condolences. Your application is going to be rather complicated, requiring a lot of documentation and supporting evidence.

On the other hand, if you were a small merchant at any point in the date range considered, your claim can be completely undocumented. Just apply at the following link, and your eligibility will be assessed by the lawsuit’s internal review team.

Do note that as an undocumented claimant, your application can be denied and there is no recourse or appeal process if this occurs. Therefore, honesty is the best policy when entering your information. Don’t expect an auditor to believe you were accepting Visa and Mastercard at your middle school lemonade stand!

Then simply make your claim, and wait for the review process to approve you. When it at last hopefully does, just hand over your direct deposit information or request a cheque (this latter option requires a $2 fee, deducted from your final settlement payout) and wait for the money to come. Just remember, you can only claim up to a maximum of $600, or 20 years in operations as a small business.

Whatever your personal situation, if you ran a business during any year of the period in question and accepted Visa/Mastercard, you should definitely apply and recoup some of the costs before the opportunity passes forever.

There Are Two Sides to Every Card

As I mentioned earlier, I have personal opinions on this case, but do advise folks going forward to continue to be courteous to the members of the Canadian business community. After all, no Miles & Points enthusiast would get to enjoy the benefits of credit cards if we didn’t have vibrant commerce in this country.

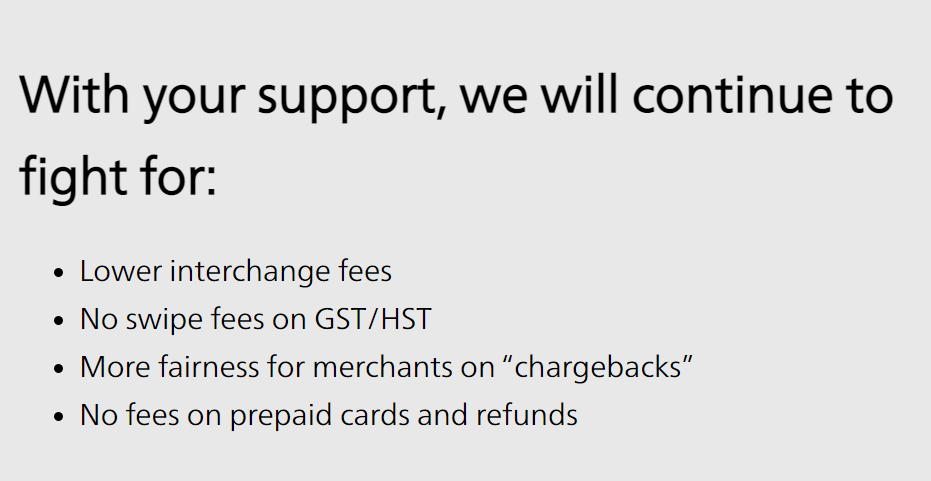

That being said, some of the stated aims by the CFIB, while they undoubtedly benefits merchants, could potentially be damaging to consumers. Let’s take a look:

Let’s break this down, because these could have significant implications for customers, especially those in the Miles & Points space.

A lowering of interchange fees, for example, could potentially result in the same situation faced by British and Australian credit card rewards enthusiasts: much lower rates of return and earning on daily spend. The same goes for an abolition of fees on GST/HST, because that portion of transactions would then become ineligible for points earning – possibly even for making the minimum spend on a credit card’s welcome bonus.

When it comes to chargebacks, I am in agreement that businesses shouldn’t be duped by unscrupulous individuals. But neither should paying customers have their legitimate chargebacks – often the last line of defence in a commercial dispute – rejected out of hand.

Think about how bad it would have been if the chargebacks made in the wake of the COVID-19 pandemic so that customers could recoup money they’d spent on flights in cash instead of travel bank credits had been denied. Tighter rejection of chargebacks could have seriously hurt customers who needed that money in a crisis situation!

As for abolishing fees on prepaid cards, I think this would unfairly hamstring very interesting and customer-friendly prepaid projects such as the Wise Card, which have done an admirable job of offering consumers greater payment convenience and lower exchange rates.

No matter what happens, the credit card space will certainly look different after October 6, 2022, when surcharges on credit card use will be permitted. Here’s hoping merchants don’t realize an overall loss in sales even if they do recoup some interchange fees. Thankfully, surcharges won’t be mandatory, so let’s hope they don’t become universal.

Conclusion

The CFIB’s lawsuit against Visa and Mastercard may have major implications for the entire Canadian credit card space.

If you’ve run a business in the past, there’s no point in dallying. Go onto the CFIB’s site now and apply for your compensation while you still can.

For the rest of us consumers, it remains to be seen whether these changes will benefit the market as a whole or only certain merchants. It doesn’t seem like the best business practice to charge customers more because they want the protections of a credit card, but ultimately time will tell.

Kirin explores the world through the lens of miles and points, sharing insights on premium travel experiences.

First-year value

$336

Monthly fee: $15.99

• Earn 1,250 points per month upon spending $750 per month for 12 months

Member Discussion