How to Remove Credit Inquiries

Credit reports. I have one. You have one. They are one of the greatest innovations of modern commerce, allowing lenders to easily assess our creditworthiness when we need to buy homes, apply for credit cards with sweet travel perks, or to borrow some money when we’re facing a rainy day.

Sadly, they can also be a major pain in the derrière. Getting a black spot on your report, such as an unpaid collection or even just an unwanted hard inquiry, can be worse than getting the pirates’ black spot of death from Long John Silver.

I have good news for you: the tools and mechanisms to remove negative marks from your credit history have become easier than ever. What was once a tedious process done entirely by mail can be done online within minutes – though don’t rule out snail mail just yet.

Today, I want to assist you in getting those unwanted credit requests off your report pronto.

Pop Quiz: Credit Bureaus and Inquiries

Attention class! Anyone remember what credit bureaus we have in Canada?

If you guessed that we have Equifax and TransUnion in Canada, you’d be right. These are the two main credit bureaus every lender consults before deciding to extend you an auto loan or shiny new prepaid “disruptive” fintech card.

The bureaus collect personal information that identify you individually by metrics such as address and date of birth, as well as use complex algorithms to determine your credit score – more on that here.

Because each bureau has different criteria of calculation, it’s common that your score will vary drastically between the two. In my personal experience, Equifax appears to be the more conservative sibling, and my score there is usually lower than my TransUnion.

I’ve also found this to be true when applying for credit cards: Equifax-only banks such as TD have been stodgier at extending me new credit than TransUnion’s heavy-hitters such as American Express and RBC.

Most credit inquiries you’ll make will be “hard” pulls – that is to say, they’ll show up on your report. Some banks, such as Amex, will only do a “soft” pull to verify your personal information, which means the inquiry won’t dent your credit score or be visible on your report.

You have the option to pay for weekly/monthly copies of the “official” version of your credit reports from Equifax and TransUnion, but I recommend you follow in my curmudgeonly footsteps and just use Borrowell for Equifax and CreditKarma for TransUnion.

The scores won’t exactly equal those found at their respective bureaus, but I’ve always found them to be a good ballpark.

How Do Entries On My Credit Report Add Up?

We don’t always get the opportunity at Prince of Travel to address folks whose credit situation might need a bit of tender loving care. This is because our optimal strategies usually require having a good-to-great credit profile as a prerequisite.

Right now, though, I’d like to help demystify credit reporting for those of us with an unblemished history and those needing some repair work alike.

First off: the number of inquiries usually doesn’t make a big impact. We’ve covered this before, but inquiries for new credit cards will often only ding you a few points, and assuming your payment history is decent, won’t disable you from getting new credit lines.

Second, for those of you on the home or auto lending market and pulling your credit multiple times at different lenders – don’t fret. Your large amount of hard inquiries across a short chronology are usually classified as one or sometimes two transactions. Once again, your ability to get new cards won’t be hurt.

Third, for those of you with a less than stellar history of payment, maybe even with late payments: as our chief found out, often your late-paid account won’t be reported to TransUnion and Equifax.

Instead, you’ll be hit with a late fee, but your score will remain unaffected so long as you pay it off before the lender reports you to the bureaus, which is typically only when it’s 30 days past due.

Finally, if you do have derogatory remarks like collections or recorded late payments on your account, these will do the real damage.

Don’t focus on your actual score too much. If you have relatively low utilization (i.e., <30% across all of your open trade lines) and good payment history, you’re good to keep on applying for cards as part of the travel game. If you’ve been late or gone to collections, take a breather.

Stay tuned in the future for a piece on how to play the Miles & Points game while rebuilding good habits (hint: American Express loves a comeback kid).

Why Would I Want to Remove an Inquiry?

There are several reasons you’d want to dispute a credit inquiry and get it off your report.

The first reason would be that you never made the inquiry. Remember all those scam calls you get from synthesized voices claiming to be the CRA? Well, big surprise: they aren’t the CRA. I hope you didn’t give out your SIN. I also hope you don’t have a sketchy neighbour who likes rifling through your mail and opening any envelopes with government markings.

Sometimes, the fault lies with a specific credit issuer. For example, on some occasions, CIBC has been known to leave two hard hits on a credit card applicant’s Equifax file rather than one.

Needless to say, it would suck to have your credit report have hard inquiries you never made on it. It would be distressing if these inquiries (which you didn’t make) were to, say, put you above the “5/6 rule” for MBNA.

In that case, you’d need to take action immediately and remove those items from your report so that you can get your MBNA Alaska Airlines World Elite Mastercard.

There’s also the case that you might have been a fool years ago, and you have a derogatory mark on your report such as a paid collection weighing your score down and causing conservative lenders like the Big 5 to deny you credit.

That would also be a deficiency in need of swift rectification, as waiting the standard seven years for the derogatory remark to drop off the file would take far too long for your liking.

Do I Need to Contact the Lender?

Before we begin: I want to recommend to you that it is not usually in your best interest to contact the lender instead of the credit bureau.

This is because the lenders tend to have a much slower response time, and even if you do jump through their Kafkaesque hoops, they’ll just be sending a message to TransUnion or Equifax to remove the inquiry, anyways.

If you’ve been a little bit of a spicy Miles & Points collector, then you may not want to have eyes on your account activities from lenders you’ve used creative strategies with – but as always, the judgement call is yours to make.

How to Remove TransUnion Inquiries

In my experience, TransUnion is the far more lenient of the two bureaus. Those I know who have had to make a dispute against an inquiry that wasn’t their own haven’t had to provide a crazy amount of supporting evidence, and have seen their inquiries removed in a short amount of time.

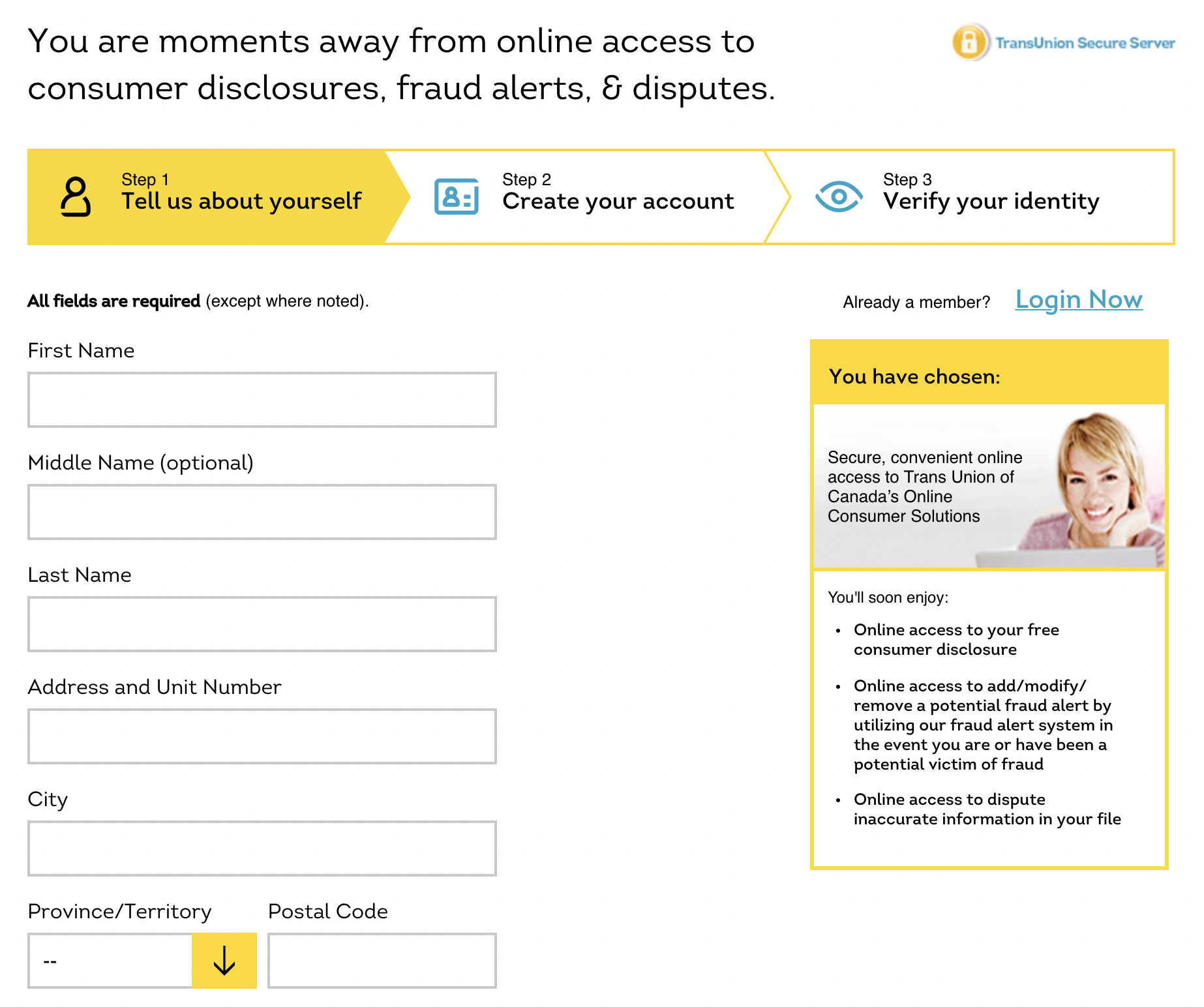

In order to remove your TransUnion inquiries, the most convenient method is online. Fill in your personal information and answer the personal verification questions.

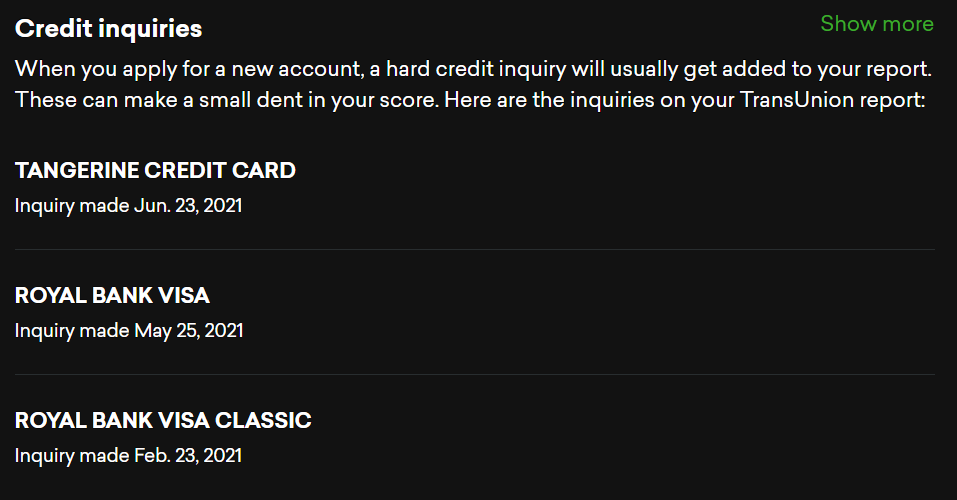

Note: The dispute page is unique and does not contain your credit score (which costs a gobsmacking $19.95 a month!) Instead, this page contains your Consumer Report, which is merely a log of all your inquiries at TransUnion.

Click on the button to file a dispute and select that you are looking for a “general” investigation. Click through all the disclaimers and you’ll be taken to a page below.

![]()

Select the inquiry you don’t recognize, request an investigation, and mark your reason for doing so as not recognizing the transaction. Attach anything that you think supports your case, even if it’s only a short explanation of what occurred. Now it’s in TransUnion’s hands.

They’ll contact the lender who pulled your credit and, if they don’t hear anything back or are not satisfied with the response they receive, then they will remove the inquiry from your report. Their fact-collection methods are not open to public perusal.

If you fail your online identity verification, don’t fret. You can attempt to call in, or you can choose to file your dispute by mail. Print out the forms on this page and fill them out, then mail everything to the mailbox listed on that web page.

Personally, I’ve seen a greater ratio of successful inquiry removal requests via traditional mail than online, but it is much more time-consuming and costs postage. Choose whichever method you’re more comfortable with.

Online filing is listed as taking up to 25 business days, but it is often much shorter. Mail applications’ biggest bottleneck will be waiting on Canada Post.

When your dispute is successful, the credit inquiry or derogatory remark will disappear from your report, as if it had never been!

Equifax: Expect Exasperation

A disclaimer: I haven’t heard of many successful disputes with Equifax – and that’s including for people whom I’ve personally known who had to deal with real and troubling cases of issues such as identity theft.

It always seems like Equifax wants enormous quantities of evidence pertaining to your case, and won’t respond to it in a timely fashion.

I hope that this has changed since I spoke with those who went through what they described as a nightmare process, but I’d suggest you prepare for a hard slog when dealing with this credit bureau.

Keeping this in mind, I’d collect as much evidence as you can before you even login to their online portal. This should include any approval emails (or lack thereof – e.g., a clean log of emails on the date of the inquiry), personal written statements, and anything else that may lead an observer to believe these transactions were not conducted by you.

Now you can login and fill out their online dispute form.

Be prepared to follow-up when Equifax emails you for further information. Provide them with all that evidence you gathered and hope for the best.

If you wish to apply by mail, they have an online-fillable form which you then print and ship. Before mailing your complaint form, make sure to make physical copies of your evidence or representations and include them in the envelope to Equifax.

When dealing with Equifax, I’d actually recommend using the mail-in method. I’ve heard a lot of horror stories about trying to make disputes work online, and I suspect you might be safer via the mail route.

With your form mailed, wait for the bureau to get to you. Their processing standard is 5–20 business days to conduct an investigation both online and via the mail. Once again, don’t forget to accommodate for Canada Post if you used analogue shipping.

If your evidence collection worthy of John Grisham has passed muster, then the disputed inquiries will disappear from all Equifax reports – sweet!

What If My Dispute Is Declined?

There’s nothing worse in the Miles & Points game than the sinking feeling that comes from being declined for a new travel credit card. I’d rate losing a credit bureau dispute as a close second, though.

This is because it can often be difficult – not to mention intensely more frustrating – to try and appeal the decision of a credit bureau. As enormous corporations, TransUnion and Equifax will probably not give you a detailed reason as to why your dispute was rejected so as to cover themselves on the liability front.

Worse, even if you do wish to appeal your case, any defined timeline in which the company will have to respond to you will be treated as more of a guideline.

Worse yet, the bureau could simply reiterate its decision.

This does not mean you’re out of options. Some declined disputes will offer you the chance to follow up with the credit bureau. Even if this isn’t offered, I’d try and call in to follow-up on the dispute.

As always, remain polite with the customer service representative. It is likely they won’t know the specifics of your case, but gently attempt to get a file number assigned to your escalation and keep it for future reference or calls.

In this situation, I would also recommend reaching out via snail mail. As anachronistic as it may sound, many companies are better at responding to mail than they are to overflowing email boxes. Use the addresses listed on TransUnion’s and Equifax’s websites, explain your situation, and enclose any additional supporting documentation you can.

When they do mail you back, make sure to keep the mail correspondence going until you get a definitive answer to your appeal.

Conclusion

It’s a real pain to deal with, but sometimes it’s just worth getting credit inquiries removed from your report.

If you’re getting declined for new cards because of too many recent inquiries, and know that some of those applications must have been performed by your goateed evil twin, then I hope these lessons helped.

I also hope this article has brought a ray of sunshine to those languishing in credit jail due to the foolishness of their younger years.

Good sailing – remove all those black spots, mateys.

Kirin explores the world through the lens of miles and points, sharing insights on premium travel experiences.

First-year value

$336

Monthly fee: $15.99

• Earn 1,250 points per month upon spending $750 per month for 12 months

Member Discussion