Guide to COVID-19 Travel Insurance for Canadians

COVID-19 travel insurance has become a necessary evil when you consider travelling outside of your home country. For a variety of reasons, purchasing a policy that covers all of the possible risks when travelling is more important during a pandemic than ever before.

Today, let’s explore your options for COVID-19 travel insurance as a Canadian traveller.

What Is COVID-19 Travel Insurance?

If you’re an adult, you are probably familiar with purchasing insurance. Whether it be for your car or home, when you become an adult, it becomes an added expense that is just part of life.

While COVID-19 travel insurance is optional, it’s probably a good idea to have based on all of the stories we’ve heard recently of people being forced to quarantine in a foreign country due to a positive COVID-19 test.

Unfortunately, when that happens, you are personally liable to cover all of your additional accommodation and food expenses – and that’s where travel insurance helps.

While there is insurance to cover illness and emergency medical emergencies while on vacation abroad (typically called emergency travel medical insurance), COVID-19 travel insurance only covers issues directly related to COVID-19.

So, if you fall and break your leg while on vacation and you only have a policy that covers COVID-19 related expenses, you wouldn’t have a valid claim with the insurance company.

At the time of writing, most of the COVID-19 insurance policies also include emergency travel medical insurance, but you should never assume it does and always read over your policy carefully.

What Does COVID-19 Travel Insurance Cover?

What you are purchasing is trip interruption insurance directly related to COVID-19. Some of the items covered with this type of insurance typically include the following:

- Return travel home: In the event that you are forced to stay in a country for longer than expected due to quarantine requirements, you will need to change your flight plans. While we have heard of airlines being somewhat flexible in rebooking your flight, this insurance provides some added coverage to pay for a return flight home.

- Accommodation and meal costs: You may be required to quarantine up to 14 days depending on the country you are visiting. This rider in the COVID-19 policy covers your expenses related to accommodation and food costs while quarantining.

There may be additional coverage included, especially if your policy also includes emergency travel medical coverage. Effectively, what you are purchasing is peace of mind in the event that you contract COVID-19 while abroad and need some help paying for your trip home or the quarantine hotel you are forced to pay for.

What Doesn’t COVID-19 Travel Insurance Cover?

Each policy is going to differ, but there are some common exclusions related to any type of insurance and some specific ones that are directly related to COVID-19.

It’s important to read your policy carefully and not to make any assumptions, but here are some common exclusions that I have seen across multiple policies:

- Pre-existing conditions: A common exclusion is a pre-existing health condition. This includes, but is not limited to, heart and lung conditions that require medication or equipment to keep under control. This is typically an exception directly related to emergency travel medical insurance and not the COVID-19 policy.

- Quarantine at home: If you are forced to quarantine while in Canada, those expenses are not typically covered.

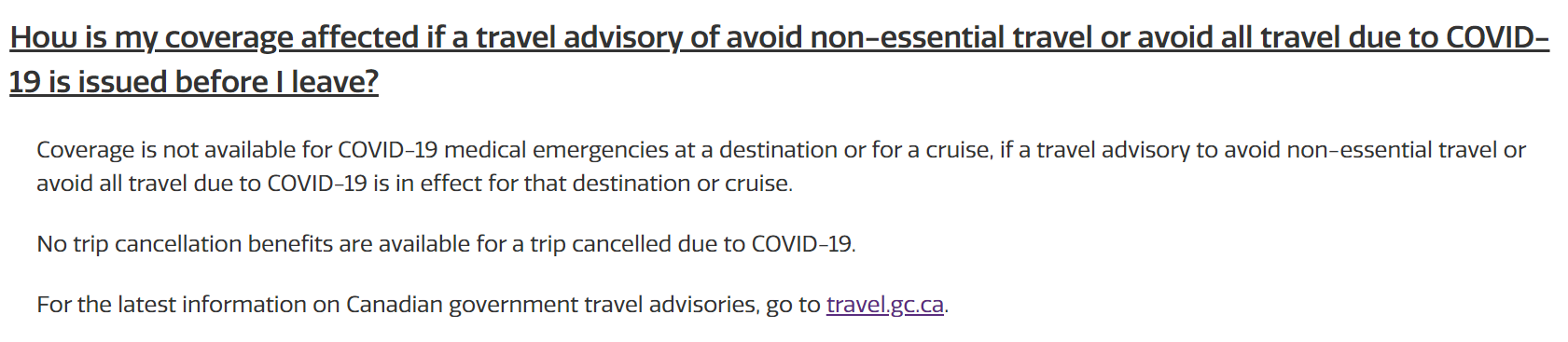

- Travel under “Avoid all travel”: The Government of Canada issues four levels of travel advisories. Currently, all countries are listed as Level 3 – Avoid non-essential travel, but this will be downgraded to a Level 2 – Practise special precautions as of February 28, 2022. If the Government of Canada issues a Level 4 – Avoid all travel notice, your policy will not be valid if you choose to travel. For most policies, insurance is valid for Level 3 and Level 2 notices, but be sure to read your policy to ensure that this is the case.

- Cruises: Most policies have a special exclusion for cruises, so any COVID-19-related expenses that you incur while on or after a cruise are not covered.

There can be more exclusions depending on your policy, so be sure to go over your policy with care and seek the advice of the insurance company before making any decisions.

Things to Look for in a Policy

The largest expense you will incur on a trip that is affected by COVID-19 is your quarantine hotel and associated food costs. With costs running in the thousands of dollars, this is an expense that many people simply cannot afford, so it makes a lot of sense to purchase a policy that provides you with the most coverage possible.

Most policies seem to have become standardized with an offering of $200/day to cover accommodation and food expenses for a maximum of 14 days.

If you are travelling as a family, that stretches to $400/day, assuming that all of your family members are on your policy. This means that the maximum coverage provided to you is $5,600 if you are a family that has been affected by COVID-19 and needs to quarantine abroad.

In many cases, this amount should be sufficient, but if you are planning on quarantining at the Ritz-Carlton, this probably won’t cover your 14-day stay.

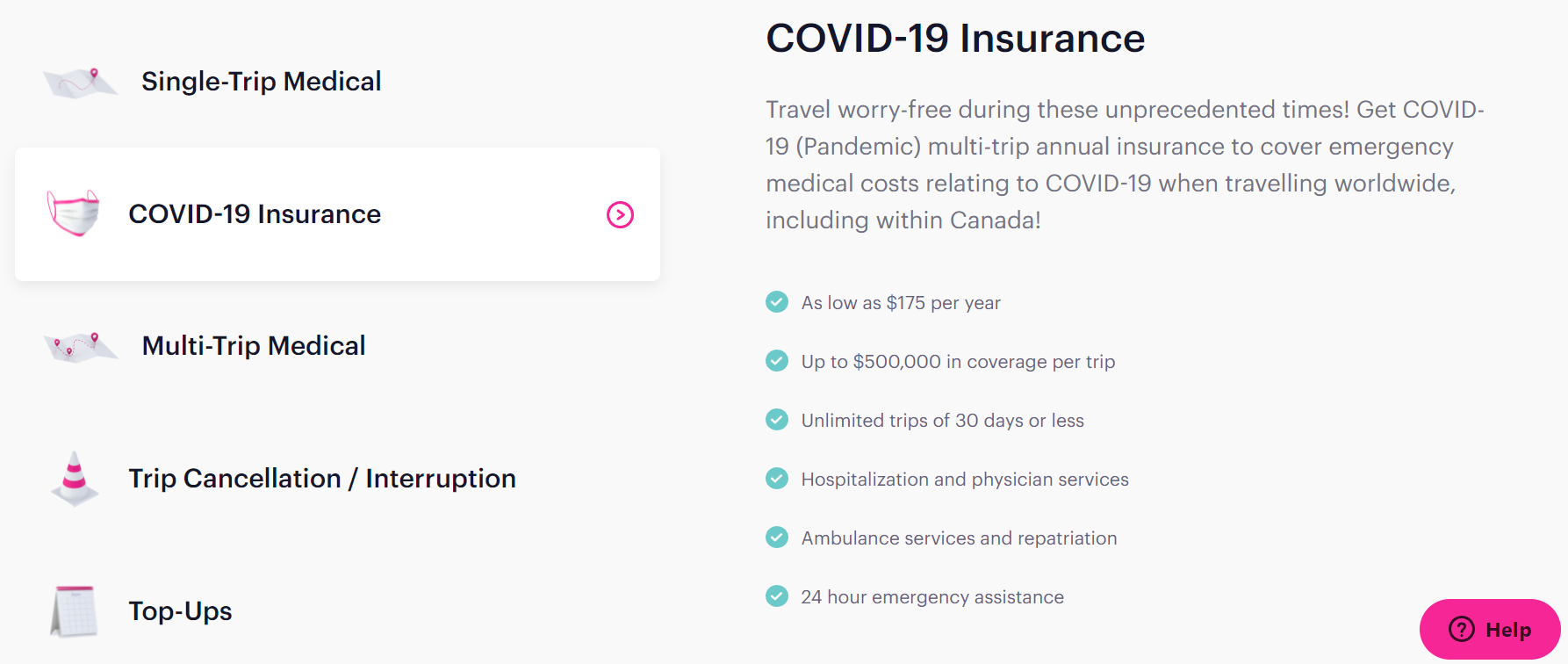

COVID-19 Insurance Providers in Canada

Canadians have relatively few choices for COVID-19 travel insurance. I was able to find three companies offering this type insurance, and their unique coverages are as follows:

- Manulife Cover Me provides emergency medical and COVID-19 insurance in one policy, but only on a per-trip basis. This means that you need to purchase coverage for each trip that you take. You can receive a quote online.

- Goose Insurance is an app-based insurance policy that provides both emergency medical and COVID-19 insurance, but only on an annual basis. This means that if you are taking multiple trips in a year, you can make one purchase to ensure coverage for the entire year. Quotes are available through the app.

- Allianz provides emergency medical and COVID-19 insurance in one policy, but only on a per-trip basis, meaning that you need to purchase separate coverage for each trip that you take. You must call in to receive a quote.

Fair warning, though – if you’re okay with getting your quote online and parsing the terms and conditions, you are all set; however, if you have any questions and need clarification, I wish you luck in reaching the insurance companies.

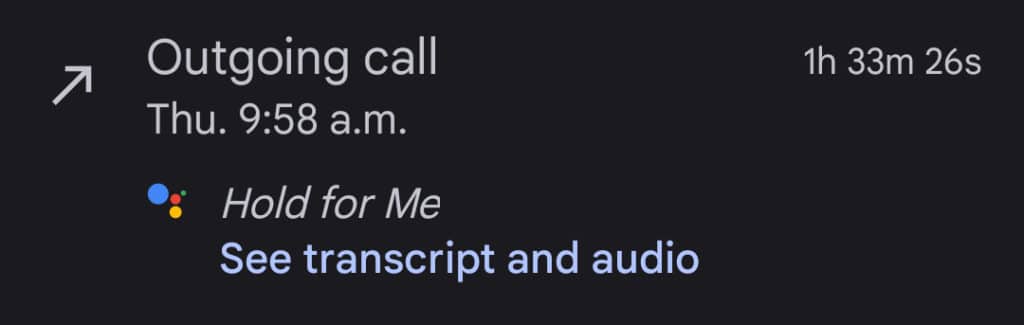

With Manulife, I made the mistake of believing that I could book an annual COVID-19 insurance policy as a Costco Executive Member. After going through the booking flow and making my purchase, I received my policy by email, only to discover that this only covered emergency medical and included no COVID-19 provisions.

It took me 1 hour and 33 minutes to reach an agent and for them to process the cancellation, which can only be done over the phone. I have yet to receive my cancelation notice, so I will watch my credit card statement to ensure that I did indeed receive a refund.

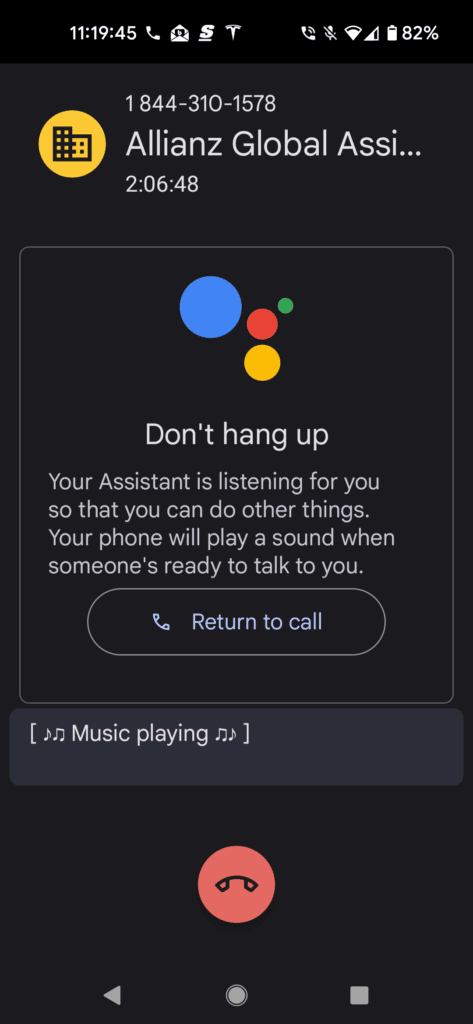

With Allianz, there is no way to receive a quote online, so you are forced to call and wait on hold. I’ve tried on multiple occasions to reach a representative and have been on hold for over two hours as I write this article.

Luckily, I have a Google Pixel 5 that waits on hold for me, otherwise I think I would have lost it.

How Much Does COVID-19 Travel Insurance Cost?

The cost for a policy is largely dependent on age, health conditions, length of travel, and travel destination.

In my case, a 17-day international trip for my family (two adults and one child) priced out at $144.16 through Manulife and $425.00 through Goose Insurance. Keep in mind that Goose Insurance provides a year’s worth of coverage.

(I wish I could tell you what Allianz charges, but I continue to wait on hold.)

Does My Credit Card Insurance Cover COVID-19?

While I continue to urge you to read your policy for a definitive answer, the usual response is “no”.

If you take a look at the insurance coverage on a premium card, such as the American Express Platinum Card, there is specific wording that states the policy is void if there is a government advisory to avoid non-essential travel.

Even after Canada’s Travel Advisory is downgraded to Level 2 as of February 28, 2022, the major credit cards will begin to cover emergency medical travel insurance and other types of protection like trip cancellation and trip interruption, but not quarantine costs due to COVID-19.

Credit Card Insurance: What You Need to Know

Read moreOther Things to Consider

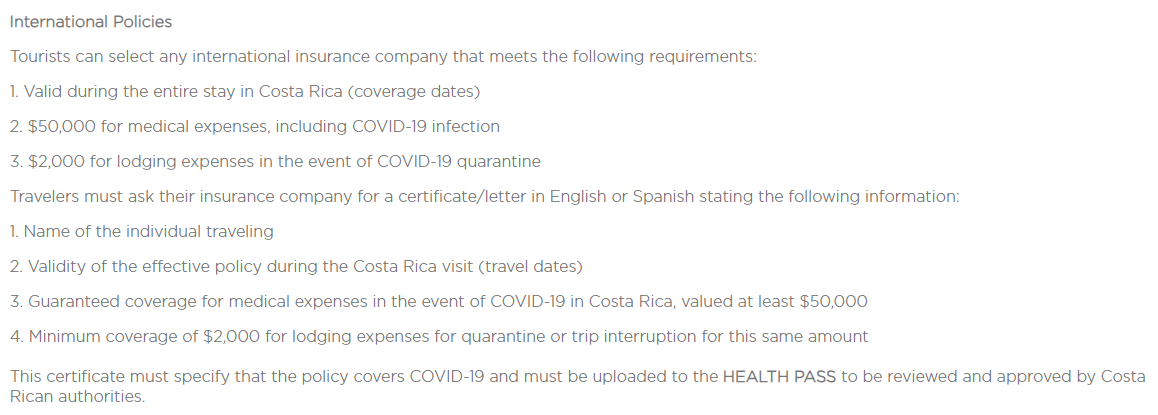

The country that you’r travelling to may require you to have specific COVID-19 insurance to avoid passing on the potential cost of your care to their own taxpayers.

As an example, Costa Rica has a specific requirement for insurance coverage and requires you to upload proof prior to entry.

Keep in mind that this is a fast-changing environment and entry requirements change at the drop of a hat.

A week ago, I was strongly considering purchasing an annual policy through Goose Insurance, but considering that Canada is about to drop its requirements for pre-arrival molecular tests, the likelihood that other countries may follow suit has increased.

This calls into question whether I might face a requirement to quarantine in Costa Rica at all, as I won’t need to take a test prior to my return journey to Canada. I’ll continue to observe how things play out and mull over my upcoming year’s travel plans before deciding on a policy to buy.

Conclusion

COVID-19 travel insurance, like all insurances, is designed to protect against worst-case scenarios. For a small amount of money, at least in comparison to the potential cost if you contract COVID-19 while abroad, you are given peace of mind that you won’t undergo financial hardship.

It’s up to each individual to decide whether or not this type coverage is right for you. For our family, we will continue to monitor Costa Rica’s entry requirements and make a last-minute decision on whether or not we need the coverage and which provider to go with.

First-year value

$336

Monthly fee: $15.99

• Earn 1,250 points per month upon spending $750 per month for 12 months

Member Discussion